Net neutrality is a term like pro-choice or right to work that sounds uncontroversial but is used by its proponents to refer to a specific and highly contentious policy. This chapter defines net neutrality as the policy adopted by the Federal Communications Commission (FCC) majority in its 2015 rule titled “Protecting and Promoting the Open Internet” (hereinafter referred to as the 2015 Open Internet order) to describe the regulatory policy followed by the FCC in the Open Internet Order before it was repealed in 2017.1Protecting and Promoting the Open Internet, 80 Fed. Reg. 19737 (April 13, 2015). For the brief time the FCC’s net neutrality regulation was in effect, it was applied unevenly, it prohibited conduct that could be beneficial to internet users, and it suppressed capital investment needed to support growth in a dynamic industry. Since the repeal of net neutrality regulation in 2017, we have seen increases in internet speeds, capital investment, and access to wireless cell sites.

Banning conduct and increasing regulatory oversight of conduct in the telecommunications sector is the wrong approach. The better regulatory response to the concerns that net neutrality was supposed to address is to promote faster and easier access to the internet through clear rules that embrace vigorous competition on the internet. If Congress will take the lead and clarify how internet access is to be regulated, or not regulated, then infrastructure investments can be planned knowing the layout of the playing field, and competition among providers can continue to drive new technological advances and growth of the U.S. economy.

A Brief History of Internet Regulation

The FCC is an independent federal agency that regulates interstate and international communications by radio, television, wire, satellite, and cable delivery. The FCC is led by five commissioners who are appointed by the president and approved by the Senate. Typically (and at all times that are relevant for this chapter), three of the commissioners are from the president’s party and two are chosen by the leader of the other party in the Senate.

The FCC was created by the Communications Act of 1934, which Congress enacted to impose regulatory control over perceived monopolies in communications services. The original regulatory structure is still largely intact, even though competition concerns raised by today’s broadband, digital, and wireless technologies are far different from the regulatory issues of nearly a century ago. The Communications Act of 1934 draws a distinction between Title I “information services” and Title II “telecommunications services.” Title I information services are regulated lightly, if at all, while Title II telecommunications services may be subject to the same public utility–style regulation that the FCC used to regulate landline telephone service for much of the past century.

The internet was first launched in 1969, but until the 1990s traffic was fairly limited and relatively few people were using it. When regulators started to pay attention to the internet, internet service providers were classified as Title I information services, which allowed the internet to develop and thrive with relatively little regulatory oversight. That did not mean, however, that the internet was the unregulated Wild West. Instead, until 2015 the Federal Trade Commission, state attorneys general, and other state and federal consumer protection agencies had the same authority over internet service providers that they have over most other businesses.

During President Obama’s administration, the FCC commissioners appointed as Democrats began to question whether more regulatory oversight was needed, while the commissioners appointed as Republicans generally resisted increased regulation of the internet. In 2010, the FCC, by a 3–2 party-line vote, promulgated the first version of the net neutrality regulation.2Preserving the Open Internet, 76 Fed. Reg. 59192 (September 23, 2011). Internet service providers challenged this regulation, which was struck down by the DC Circuit Court of Appeals in its 2014 Verizon v. FCC decision.3Verizon v. Federal Communications Commission, 740 F.3d 623 (D.C. Cir. 2014).

In Verizon v. FCC, the court held that the FCC did not have the authority to impose its 2010 version of net neutrality regulation under Title I, but would have that authority if the FCC reclassified internet service providers as Title II telecommunications services. The FCC majority at the time got the message, and by a 3–2 party-line vote promulgated a revised rule—the 2015 Open Internet order—to reclassify internet service providers as telecommunications services under Title II and impose its concept of “net neutrality.”4For a brief history of internet regulation and the net neutrality debate, see the introduction in Randolph J. May and Seth L. Cooper, A Reader on Net Neutrality and Restoring Internet Freedom (Potomac, MD: Free State Foundation, 2018).

In 2017, soon after taking office, President Trump appointed a Republican replacement for an outgoing Democratic FCC commissioner. In December 2017, the FCC, with four holdover commissioners and the one new commissioner, voted again along party lines to promulgate the “Restoring Internet Freedom” order,5Restoring Internet Freedom, 83 Fed. Reg. 21927 (May 11, 2018). which largely undid the net neutrality regulations of the Open Internet order and restored internet service providers to their previous status as Tile I information services. The majority in favor of deregulation may only last, however, until the first commissioner vacancy following the 2020 election. Net neutrality regulation was imposed by a 3–2 vote in 2015, and it could be imposed again in 2021 with the change of a single commissioner.

Net Neutrality Regulation under the FCC’s 2015 Open Internet Order

The term net neutrality is not well defined, and the lack of clarity about what is meant by net neutrality causes a great deal of confusion in policy debates. For the purposes of this chapter, net neutrality will be defined as the regulatory policy toward internet service providers found in the 2015 Open Internet order.

The 2015 Open Internet order divides the internet marketplace into internet service providers (ISPs), to be regulated under Title II, and “edge providers,” which remain under Title I. The terminology used by the FCC majority indicates these commissioners’ view that ISPs are looking to extort punitive rents from edge providers that can’t fight back without the protection of the FCC. But edge providers are hardly fringe players on the internet—they are anyone that provides content on the internet, including Google and Amazon, the two largest companies in the world by market capitalization.6These categorizations are somewhat inconsistently applied. For example, Google operates its own infrastructure that is not considered an “ISP” network. Tom Foremski, “Google Is Building a Private Internet That’s Far Better, and Greener, than the Internet,” ZDNet, March 18, 2010, Tom Evslin, “Internet Fast Lanes: You May Be Surprised by Who Actually Has Them,” Morning Consult, August 4, 2017. ISPs include wireless carriers such as AT&T and Verizon and cable companies such as Comcast, Cox, and Spectrum. These ISPs are substantial companies, but nowhere near the size of some of the edge providers.

The Open Internet order’s analysis of why its net neutrality regulation was needed was based on what the FCC called the “virtuous cycle” theory. The FCC majority did not offer very much explanation in the Open Internet order for its conclusion that the virtuous cycle theory would lead to ISPs choking off demand for the very service they offer:

The key insight of the virtuous cycle is that broadband providers have both the incentive and the ability to act as gatekeepers standing between edge providers and consumers. As gatekeepers, they can block access altogether; they can target competitors, including competitors to their own video services; and they can extract unfair tolls. Such conduct would, as the [Federal Communications] Commission concluded in 2010, “reduce the rate of innovation at the edge and, in turn, the likely rate of improvements to network infrastructure.” In other words, when a broadband provider acts as a gatekeeper, it actually chokes consumer demand for the very broadband product it can supply.7Protecting and Promoting the Open Internet, 80 Fed. Reg. 19737, 19740 (April 13, 2015), citing Preserving the Open Internet, 76 Fed. Reg. 59191, 59194 (September 23, 2011).

The FCC majority then justified banning certain conduct by internet service providers using a “bright-line” approach:

The record in this proceeding reveals that three practices in particular demonstrably harm the open Internet: blocking, throttling, and paid prioritization. . . . [W]e find each of these practices is inherently unjust and unreasonable, in violation of section 201(b) of the [Communications] Act [of 1934], and that these practices threaten the virtuous cycle of innovation and investment that the Commission intends to protect under its obligation and authority to take steps to promote broadband deployment under section 706 of the 1996 [Telecommunications] Act. We accordingly adopt bright-line rules banning blocking, throttling, and paid prioritization by providers of both fixed and mobile broadband Internet access service.8Protecting and Promoting the Open Internet, 80 Fed. Reg. at 19752.

The Open Internet order further described its three specific regulatory prohibitions:

No Blocking. Consumers who subscribe to a retail broadband Internet access service must get what they have paid for—access to all (lawful) destinations on the Internet. This essential and well-accepted principle has long been a tenet of Commission policy, stretching back to its landmark decision in Carterfone, which protected a customer’s right to connect a telephone to the monopoly telephone network. . . .

No Throttling. The 2010 open Internet rule against blocking contained an ancillary prohibition against the degradation of lawful content, applications, services, and devices, on the ground that such degradation would be tantamount to blocking. . . . A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not impair or degrade lawful Internet traffic on the basis of Internet content, application, or service, or use of a non-harmful device, subject to reasonable network management. . . .

No Paid Prioritization. Paid prioritization occurs when a broadband provider accepts payment (monetary or otherwise) to manage its network in a way that benefits particular content, applications, services, or devices. To protect against “fast lanes,” this Order adopts a rule that establishes that: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not engage in paid prioritization.9Protecting and Promoting the Open Internet, 80 Fed. Reg. at 19740.

The Open Internet order had several other effects that are also important, but will not be analyzed in detail here. First, by classifying broadband providers as Title II telecommunications services, the Open Internet order effectively stripped the Federal Trade Commission of jurisdiction over broadband ISP practices that are potentially harmful to consumers, including practices affecting online privacy.10Theodore R. Bolema, “The FTC Has the Authority, Expertise, and Capability to Protect Broadband Consumers,” Perspectives from FSF Scholars (Free State Foundation) 12, no. 35 (October 19, 2017). Second, the Open Internet order created an uneven playing field between ISPs and edge providers by treating their relationship as predominantly that of suppliers and users of internet access, when in fact regulated ISPs and unregulated edge providers are direct competitors in many markets.11Evslin, “Internet Fast Lanes.” Third, the Open Internet order contained a “general conduct standard,” which was a catch-all provision that allowed the FCC to sanction almost any conduct that three commissioners deem undesirable.12Introduction in May and Cooper, Reader on Net Neutrality.

Problems with the Economic Analysis in the 2015 Open Internet Order

The 2015 FCC majority, applying its virtuous cycle theory, conjectured three ways in which ISPs might benefit from throttling, blocking, and paid prioritization: (1) ISPs could avoid the cost of making new investments, (2) they could charge more for access with capacity restricted by the lack of new investments, and (3) they could further enhance their revenues by making “slow lane” traffic less attractive, forcing content providers to move their content to “fast lanes” where the ISPs would charge extra for better service. The FCC majority argued that the 2015 Open Internet order’s three bright-line prohibitions, when combined with the general conduct standard in the order, would take away broadband providers’ incentives to game the system and encourage them to invest more in broadband infrastructure.

One obvious concern with the Open Internet order’s analysis is that there is very little evidence that any of the allegedly harmful conduct by ISPs was actually occurring under Title I regulatory oversight. Then Commissioner Ajit Pai (he is now FCC chairman) pointed this out in his dissent to the Open Internet order:

The Order ominously claims that “threats to Internet openness remain today,” that broadband providers “hold all the tools necessary to deceive consumers, degrade content or disfavor the content that they don’t like,” and that the FCC continues “to hear concerns about other broadband provider practices involving blocking or degrading third-party applications.” The evidence of these continuing threats? There is none; it’s all anecdote, hypothesis, and hysteria. A small ISP in North Carolina allegedly blocked VoIP calls a decade ago. Comcast capped BitTorrent traffic to ease upload congestion eight years ago. Apple introduced FaceTime over Wi-Fi first, cellular networks later. Examples this picayune and stale aren’t enough to tell a coherent story about net neutrality. The bogeyman never had it so easy. . . . One would think that a broken Internet marketplace would be rife with anticompetitive examples. But the agency doesn’t list them. And it’s not for a lack of effort.13Protecting and Promoting the Open Internet, GN Docket N0. 14-28(dissenting statement of Ajit Pai, Commissioner, FCC) at 14.

Apart from the lack of evidence of actual harm from any existing internet practices, the FCC’s theory is not based on any conventional analysis of market power. Instead, the FCC based the Open Internet order’s rules on the specious “gatekeeper” concept, which in essence is an assertion by the FCC majority that customers have a unique relationship with ISPs that gives ISPs monopoly power over them. Thus, the FCC extended Title II to ISPs with only a few subscribers and zero market power:

This Order need not conclude that any specific market power exists in the hands of one or more broadband providers in order to create and enforce these rules. Thus, these rules do not address, and are not designed to deal with, the acquisition or maintenance of market power or its abuse, real or potential.14Protecting and Promoting the Open Internet, 80 Fed. Reg. at 19739.

The 2015 FCC majority was arguing that all ISPs are “terminating access monopolists” because they are the gatekeepers to the internet and because the cost of switching providers is so high for users. Even if those claims were true, a better response than imposing a sweeping regulatory structure that would discourage future competition, would rather be to address the specific anticompetitive harm the FCC claimed to have identified.15At the time of the 2015 Open Internet order, the ISP market was more competitive and dynamic than monopolistic: 99 percent of US consumers had a choice of providers. Chart III.A.2 in Federal Communications Commission, “Annual Report and Analysis of Competitive Market Conditions with Respect to Mobile Wireless, Including Commercial Mobile Services” (WT Docket No. 16-137, September 23, 2016), 31. Instead, the FCC created the very problem that it was supposed to fix—except that it effectively made the FCC the internet access gatekeeper, injecting itself into ISPs’ decisions to innovate, interconnect, and invest.16Introduction in May and Cooper, Reader on Net Neutrality.

Profits based on taking advantage of leverage from high market shares in a dynamic market are not sustainable because they attract new entry and investment by competitors. Such increases in competition should be encouraged, because competition defeats the incentive to restrict capacity described by the virtuous cycle theory, and also brings new firms into the market that can be the source of new innovation. But that is not what the Open Internet order did, as Commissioner Ajit Pai pointed out in his dissent:

And yet, literally nothing in this Order will promote competition among Internet service providers. To the contrary, reclassifying broadband, applying the bulk of Title II rules, and half-heartedly forbearing from the rest “for now” will drive smaller competitors out of business and leave the rest in regulatory vassalage. Monopoly rules designed for the monopoly era will inevitably move us in the direction of a monopoly.17Protecting and Promoting the Open Internet, GN Docket N0. 14-28(dissenting statement of Ajit Pai, Commissioner, FCC) at 10.

One of the bright-line bans imposed by the Open Internet order is particularly problematic. The two relatively uncontroversial bright-line bans concern the blocking of traffic based on content and the “throttling,” or slowing, of traffic based on content. While it might be argued that these bans were mostly harmless and contain qualifying language that should prevent the worst misapplications by regulators, they are unnecessary if the ISP market is reasonably competitive. But the rubber meets the road with the ban on paid prioritization arrangements, by which the FCC tried to prevent ISPs from charging for priority access.

Consumers Benefit from Paid Prioritization in Many Markets

Paid prioritization is used in many markets, regulated and unregulated. It is striking how common the practice is, and how widely accepted different forms of paid prioritization have become in diverse markets. Directly contradicting what the FCC’s virtuous cycle theory predicts, existing paid prioritization arrangements do not lead to firms trying to choke off demand for their products. Instead, they consistently lead to more investment and more choices that benefit customers.

Another federal agency, the US Postal Service, makes extensive use of its own fast lanes and slow lanes for customers. Customers can pay for various forms of expedited delivery for packages and mail, or they can pay regular postage or bulk rates for mail that will be delivered on a slower schedule. FedEx and other private delivery services offer similar expedited “fast lane” schedules, but—contrary to the virtuous cycle theory—that has not given them the incentive to slow down deliveries of packages for customers who do not pay extra for higher-priority deliveries.18Kenneth Button and David Christiansen, “Unleashing Innovation: The Deregulation of Air Cargo Transportation” (Mercatus on Policy, Mercatus Center at George Mason University, Arlington, VA, November 2014).

Many states now offer actual “fast lanes” on highways, for a toll, as a way of attracting investment for highway projects. For example, Virginia has used the optional toll system to attract private investment for highway construction, and is currently relying on new private investment to expand the toll network to a stretch of highway on Interstate 395 going into the District of Columbia. Terry McAuliffe, Virginia’s former Democratic governor, touted this expansion as “the latest step in our ongoing effort to move more people and provide more travel choices in one of the most congested corridors in the country.”19Terry McAuliffe, “Governor McAuliffe Announces Acceptance of Private Sector Proposal to Deliver I-395 Express Lanes Extension,” news release, February 25, 2017, http://www.vdot.virginia.gov/newsroom/statewide/2017/governor_mcauliffe_announces_acceptance111748.asp. Commuters willing to pay for a faster trip now have the option to do so. Even drivers who do not pay the toll stand to benefit from the private investment in and expansion of the highway, which reduces congestion in the nontoll lanes while giving them the option to use the faster toll lanes when they wish to use them.20Robert Krol, “Tolling the Freeway: Congestion Pricing and the Economics of Managing Traffic” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, May 2016).

One paid prioritization practice that has been extensively analyzed over many years by the US antitrust agencies is the usage of slotting allowances at grocery stores, bookstores, and other retailers.21Federal Trade Commission, “Slotting Allowances in the Retail Grocery Industry, Selected Case Studies in Five Product Categories” (Federal Trade Commission Staff Study, November 2003). A supplier seeking to sell its merchandise at a retailer may agree to pay a slotting allowance in order to have its products placed on the most favorable shelf space, while other suppliers may be willing to accept less favorable shelf space. The practice of paying for favorable slotting may be an effective strategy for introducing new products that would otherwise require more spending on advertising and other forms of marketing. Former Commissioner Joshua D. Wright of the Federal Trade Commission, in his review of the economic effects of slotting allowances, finds that the practice generally benefits consumers:

My results show that slotting contracts are primarily associated with brand-shifting of sales within a product category, but not increases in category level prices or a reduction in category output or variety. To the extent that slotting contract revenue is passed on to consumers in competitive retail markets, an assumption generally warranted in the grocery retail industry, the results here imply that slotting contract competition is likely to benefit consumers. In sum, my findings are inconsistent with anticompetitive theories and, in practice, demonstrate that such agreements are likely procompetitive and consistent with the promotional services theory.22Joshua D. Wright, “Slotting Contracts and Consumers Welfare,” Antitrust Law Journal 74, no. 2 (2007): 440.

In a wide range of markets, customers have shown they are willing to voluntarily enter into paid prioritization arrangements, and usually are better off for it. For example, airlines charge passengers extra for a variety of enhanced services, including first-class seats, priority boarding, seats with extra leg room, and seats near the front of the airplane. The airlines’ goal is not to exclude passengers who do not pay for these services or force them to pay higher fares. In fact, the opposite effect is much more likely. Regular air travelers can see that airlines try to fill as many seats as they can, and even offer “economy” fares that may not include any choice of seat, for example.

The customers who do not pay extra for better airline service are unlikely to be made worse off by the presence of other passengers on the plane who choose to pay extra for better service. Instead, it is more likely that passengers who pay less are better off if the airline chooses to offer more flights over more routes to attract customers willing to pay extra, and then offers lower fares to fill the remaining seats on those flights. Put another way, even though many customers today may feel as if they are being nickeled-and-dimed by airlines because of the fees associated with nearly every aspect of flying, forcing airlines to charge the same fares to everyone will almost certainly lead to fewer flights and routes, as well as to less investment for increasing capacity, which will raise fares and reduce choices for the most cost-conscious customers, leaving those customers worse off as a result.

Similarly, sports stadiums provide luxury boxes and favorable seating for higher prices, but that does not mean that the stadium operators want to exclude other customers who are unwilling to pay for premium seating or amenities, nor that they want to build smaller stadiums to restrict the supply of seats in order to drive up prices. Having some customers pay extra for better seats generates revenue that may be used to upgrade the stadium, to offer extra amenities to all customers, or to attract free agent professional players to make the home team more competitive—all of which may make games more enjoyable for all fans, even the ones paying the least.

These and other variations on paid prioritization have developed over time as suppliers, distributors, and customers have experimented in the market to find the arrangements that provide the greatest benefits. So long as markets are reasonably competitive, paid prioritization arrangements that try to take advantage of other parties will not survive for long, because the parties at a disadvantage can find alternative arrangements.

When Paid Prioritization May Be Necessary for Attracting Investment

Some specialized services for dedicated users require a high level of internet speed and reliability. The benefits of video phone calls and video streams from Netflix, for example, are reduced when they are delayed by slow buffering. Other internet uses do not necessarily require a prioritized internet connection. Email traffic, most file downloading, and many other uses lose little of their value if their transmission is delayed somewhat in a slow lane, although too long of a delay could diminish their value.

Paid prioritization offers benefits both to services that are sensitive to delays and to services that are not. Those that pay more are better off because they receive better quality service, in the same way that some people shipping packages are willing to pay extra for priority mail services that arrive faster, while others will not see enough benefit from avoiding delays to justify paying more.

Many future web applications are unlikely to develop if their developers cannot be assured that they will have access to fast and stable internet connections. One real-world example is Aira, a company that is providing smart glasses for people with vision impairments. Aira helps the visually impaired “see” by employing the capabilities of emerging 5G networks. Its customers receive instant wireless access to visual information through smart glasses, augmented reality, machine learning, geolocation, sensors, and trained human agents. Aira’s customers can use their glasses to navigate city streets and airports, review printed material, catch public transportation, and get real-time assistance for job applications, shopping, and travel. But Aira glasses won’t work without a robust network with dependable connectivity.23Roslyn Layton, “Prioritization: Moving Past Prejudice to Make Internet Policy Based on Fact,” AEIdeas, April 17, 2018.

Autonomous vehicles, interactive e-learning, and telemedicine are other examples of applications in the early stages of development. Investors may be unwilling to take the risk of investing in these applications if they cannot be assured of reliable prioritized broadband connections. For example, telemedicine is an emerging private application that may require prioritization in order to become widely available and accepted. Telesurgery is already allowing specialized surgeons in one location to operate on patients in completely different locations. The emerging market for telesurgery can give patients in small hospitals or remote areas access to highly skilled specialists who otherwise would not serve those areas. According to a medical journal article,

The ultimate goal of telerobotic surgery is to replicate the Ted Bolema normal process of surgery from a distance. The success of telesurgery (or any aspect of telemedicine for that matter) depends largely on how faithfully and without incident remote activities duplicate their on-site equivalents. Because of its direct impact on surgeon performance, a frequent metric in real-time telesurgery research is that of system delay.24Eric J. Hanly and Timothy J. Broderick, “Telerobotic Surgery,” Operative Techniques in General Surgery 11, no. 2 (2005): 173, citations omitted.

The FCC’s prohibition of paid prioritization may well prevent these services from developing, as well as other new applications that no one is yet anticipating. Their loss is difficult to measure because we cannot easily anticipate what will never happen.

Banning Paid Prioritization Doesn’t Advance the FCC’s Stated Objectives

Even if it were established that ISPs try to use paid prioritization in ways that do not benefit users, a sweeping regulatory ban on paid prioritization creates two problems that are likely to be worse than the problem the regulation is intended to address. First, such a ban prevents the paid prioritization arrangements that benefit final customers, who may want to pay extra for the reliability needed for their applications. Second, the ban on paid prioritization limits the return on investment by ISPs, so that they will invest less in situations where they do not have market power and protection from new entry.

The claim by the 2015 FCC majority that ISPs’ status as “terminating access monopolists” requires the FCC to ban paid prioritization arrangements is inconsistent with the usual economic analysis of how firms with monopoly power behave. Basic economic analysis tells us that if ISPs are seeking to abuse whatever monopoly power they might have, they would be better off raising prices for internet access for all their customers until they reach the monopoly price rather than creating a new pricing arrangement that would only collect extra revenues from the minority of customers that need the priority access.

While the 2015 Open Internet order’s ban on paid prioritization was framed as protecting consumers, it is worth asking whether consumers really want this protection. As the examples in the previous section show, a ban on paying for faster internet service is aimed at preventing internet users from paying for higher-quality or faster service. People choose to pay for better service all the time in many different markets, and rarely is that considered controversial or exploitative of the customers who want better service.

To the extent that there are any remaining concerns about broadband providers having market power and abusing it, these concerns should be addressed in a more closely tailored way to resolve the specific harm that arises from clearly anticompetitive instances of paid priority. Tailored responses used to address anticompetitive harms and inefficiencies in other industries, including antitrust laws, consumer protection laws, and minimum quality standards, may be sufficient to prevent the harms that could plausibly result from paid prioritization by broadband providers. More targeted approaches are less likely to destroy the real benefits and efficiencies that can be achieved using voluntary contracting arrangements, and less likely to discourage investment for the applications and new entrants that may require fast and reliable broadband connections.

Importance of Telecommunications Investment to the US Economy

The broadcast and telecommunications sector of the US economy is an important part of the US economy in and of itself, accounting for 2.1 percent of the US GDP in 2018.25Bureau of Economic Analysis, US Department of Commerce, “Industry Economic Accounts Underlying Detail,” news release, October 29, 2019. The impact of telecommunications investment spreads far beyond the telecommunications sector, affecting many other sectors of the economy. Telecommunications are used by firms in other sectors as a crucial part of their production process, for marketing their products, for placing orders, and for credit validation to facilitate business transactions. Innovative new telecommunications products are emerging, building on the facilities created from past investment. As Chairman Pai points out, “Broadband has also made many sectors of the economy more productive, from shipping to energy. And it has given birth to entirely new industries, like the mobile apps economy, telemedicine, online education, and the nascent Internet of Things.”26Ajit Pai, “Infrastructure Month at the FCC,” news release, Federal Communications Commission, March 30, 2017, https://www.fcc.gov/news-events/blog/2017/03/30/infrastructure-month-fcc.

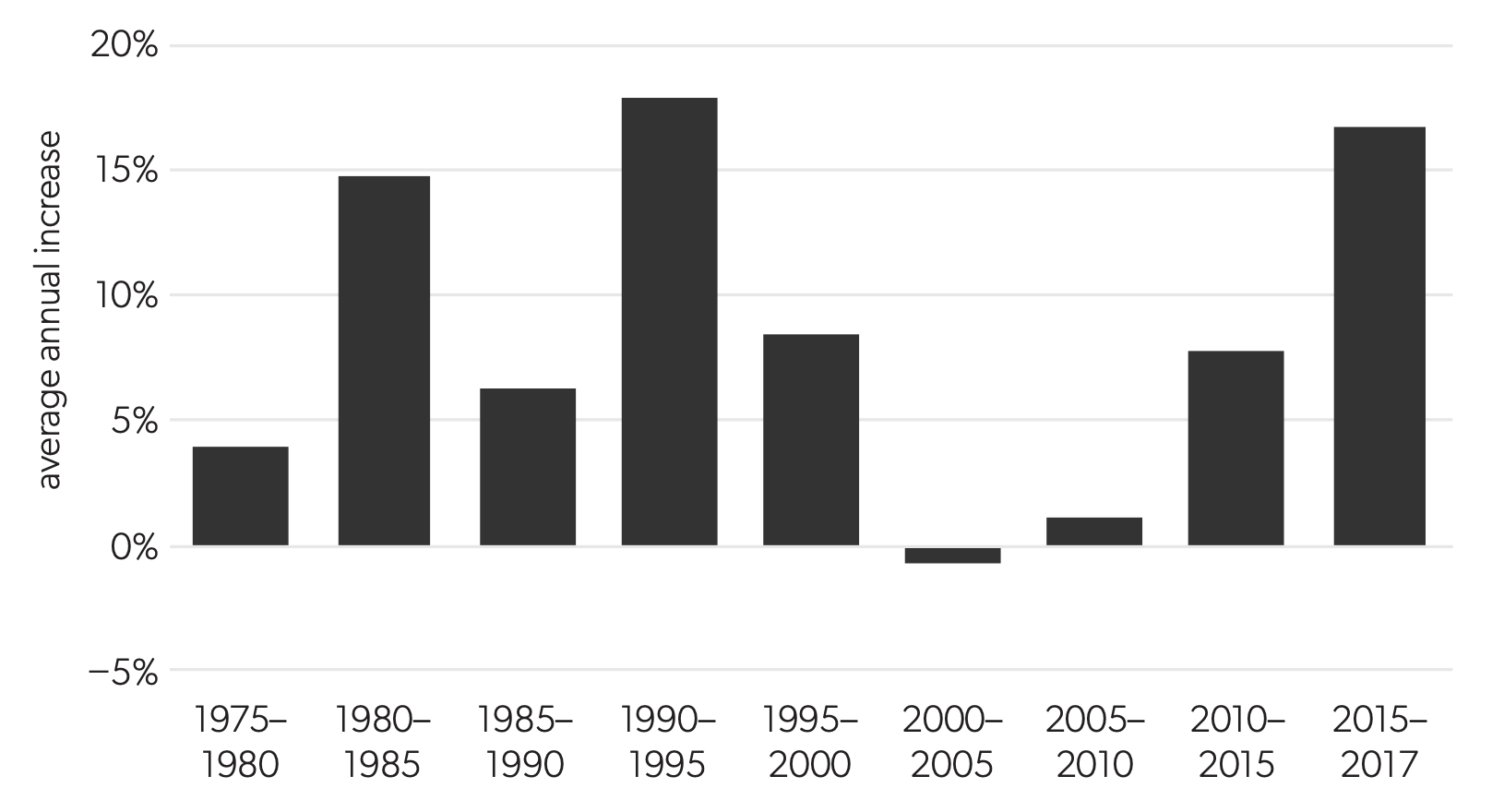

Figure 1. Increase in Telecommunications Regulatory Restrictions

Source: RegData for three-digit North American Industry Classification System code 517: Telecommunications. Patrick A. McLaughlin and Oliver Sherouse, RegData US 3.0 Daily (data set), QuantGov, Mercatus Center at George Mason University, 2017.

The US telecommunications sector has experienced ongoing and consistent increases in regulation over time, except for about a decade where the regulatory accumulation leveled off from approximately 2000 to 2010. Figure 1 shows the accumulation of federal telecommunications regulations, using the RegData database at the three-digit level of the North American Industry Classification System (NAICS).27RegData measures regulatory restrictions at the industry level according to the two-, three-, and four-digit levels of the NAICS. It is particularly useful because it is an industry-specific quantification of federal regulation that counts the number of actual regulatory restrictions using text analysis of the Code of Federal Regulations rather than relying on proxies such as the number of pages in the Code of Federal Regulations or in the Federal Register. Patrick A. McLaughlin and Oliver Sherouse, RegData US 3.2 Annual (data set), QuantGov, Mercatus Center at George Mason University, 2020; Omar Al-Ubaydli and Patrick A. McLaughlin, “RegData: A Numerical Database on Industry-Specific Regulations for all United States Industries and Federal Regulations, 1997–2012,” Regulation & Governance 11 (2015): 109–23. NAICS category 517 is for the telecommunications industry, and it includes wired and wireless telephone and internet carriers, including voice over internet protocols, cable and satellite distribution services, and telecommunications reselling services.

Federal regulatory restrictions have increased steadily in the US telecommunications sector, other than a decrease in 2000-2005, with an acceleration of new regulation additions after 2010. These increases represent net changes in the number of federal restrictions in place in the different time periods—that is, they consider both regulations that are added and regulations that are removed. Only changes in federal regulation are noted, however; regulatory burdens created at the state or local level are not included. As regulations are added, the amount of interaction between regulations increases, so the negative effect of regulatory accumulation results in a compounding effect as new regulations continue to accumulate.28Michael Mandel and Diana G. Carew, “Regulatory Improvement Commission: A Politically-Viable Approach to U.S. Regulatory Reform” (Policy Memo, Progressive Policy Institute, Washington, DC, May 2013).

Regulatory controls that have outlived their intended purposes may be misapplied in ways that deprive the US economy of the benefits of new competition, greater innovation, and new investment that would otherwise lead to greater benefits for American customers. Even regulations that were promoted as ways to encourage investment by new firms can have the opposite effect. Michał Grajek and Lars-Hendrik Röller, economics professors at the European School of Management and Technology in Berlin, find that the European Union’s open-access approach discourages entrants’ individual investment even as new entry increases. They conclude, “Because facilities-based entry is likely to require substantial firm-level investment, our results are consistent with the view that the regulatory framework in Europe fails to deliver effective incentives to move toward facilities-based competition.”29Michał Grajek and Lars-Hendrik Röller, “Regulation and Investment in Network Industries: Evidence from European Telecoms,” Journal of Law and Economics 55, no. 1 (2012): 211.

Weak growth in the telecommunications sector is a problem not only for telecommunications firms, but also for firms and entrepreneurs throughout the economy that depend on telecommunications in their businesses and for their own innovation. As Chairman Pai explained,

Today, with a powerful plan and a broadband connection, you can raise capital, start a business, immediately reach customers worldwide, and disrupt entire industries. Never before in history has there been such opportunity for entrepreneurs with drive and determination to transcend their individual circumstances and transform their world.

And achieving this success does not require you to move to Silicon Valley or Stockholm or Seoul any other tech hub around the world. There are opportunities in every city in every corner of the world, if—and this is a big if—you have high-speed access to the Internet.30Ajit Pai, “Remarks of the Federal Communications Commission Chairman Ajit Pai at the Mobile World Congress,” Barcelona, Spain, February 28, 2017, speech.

Chairman Pai further explained how his concern about the 2015 Open Internet order’s impact on investment was an important consideration when he sought to have the order repealed:

The FCC decided to apply last-century, utility-style regulation to today’s broadband networks. Rules developed to tame a 1930s monopoly were imported into the 21st century to regulate the Internet. This reversal wasn’t necessary to solve any problem; we were not living in a digital dystopia. The policies of the Clinton Administration, the Bush Administration, and the first term of the Obama Administration had produced both a free and open Internet and strong incentives for private investment in broadband infrastructure.

Two years later, it has become evident that the FCC made a mistake. Our new approach injected tremendous uncertainty into the broadband market. And uncertainty is the enemy of growth. After the FCC embraced utility-style regulation, the United States experienced the first-ever decline in broadband investment outside of a recession. In fact, broadband investment remains lower today [in early 2017] than it was when the FCC changed course in 2015.31Ajit Pai, “Remarks of the Federal Communications Commission Chairman Ajit Pai at the Mobile World Congress” (speech at the Mobile World Congress, Barcelona, Spain, February 28, 2017).

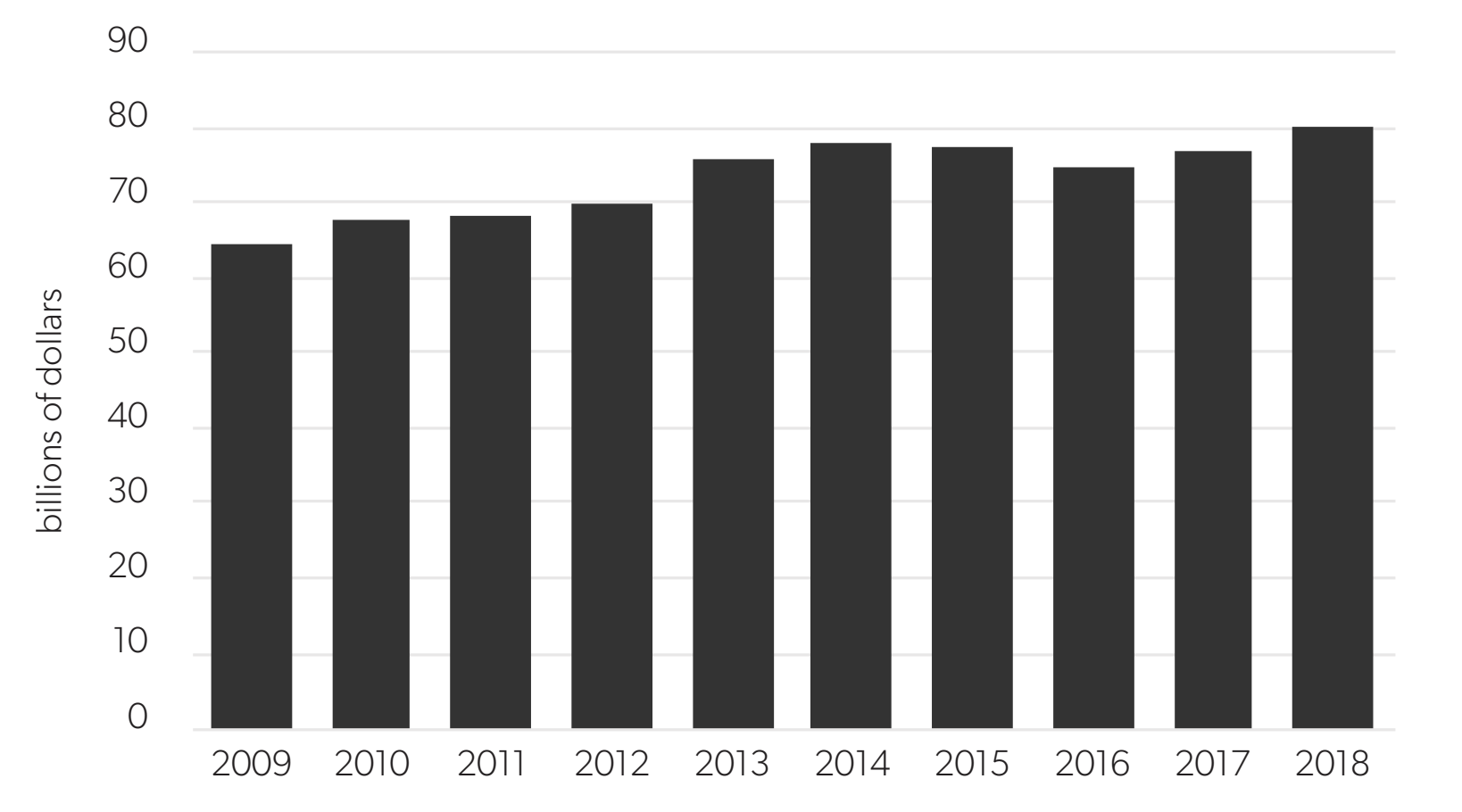

Pai was referring to the estimate by Hal Singer, a senior fellow at the Progressive Policy Institute, of a decline in domestic broadband capital expenditures of $3.6 billion in 2016, or 5.6 percent, relative to 2014 levels.32Hal Singer, “2016 Broadband Capex Survey: Tracking Investment in the Title II Era,” Hal Singer (blog), March 1, 2017. As shown in figure 2, the only two years in which US broadband investment has declined were 2015 and 2016, which were while the Open Internet order was in effect. When it became clear in 2017 that the FCC intended to undo the net neutrality regulations of the Open Internet order, capital investment in broadband internet capacity began to recover, and reached a record level in 2018 compared to recent years.

These trends are continuing, as Chairman Pai pointed out in October of 2020 when he described the increase in internet speeds, investment, and access to wireless cell sites since 2017:

And what’s been the result [following the Restoring Internet Freedom order]? The Internet has remained free and open. And it’s stronger than ever. Millions more Americans have access to the Internet today than in 2017. In 2018 and then again in 2019, the United States set records for annual fiber deployment, and we’ve seem network investment hit levels that our nation hadn’t seen in over a decade. In fact, since we adopted the Restoring Internet Freedom Order, average download speeds for fixed broadband in the United States have doubled, increasing by over 99% (so much for getting the Internet one word as a time). And in 2018 and 2019, we added over 72,000 wireless cell sites in the United States, after adding fewer than 20,000 in the prior four years.

The potential for net neutrality regulation being readopted and then retracted has a cost, however, and one that is difficult to measure. Uncertainty about what the future regulatory environment will be like creates business uncertainty. Singer explained the effects of this uncertainty in 2013, as the FCC was beginning to consider how to replace the 2010 version of net neutrality regulation that was about to be struck down in court:

ISPs will likely hedge against this new regulatory risk by conserving cash or paying out dividends rather than investing in continued network improvements. This reduction is not academic: In the few months since the [draft] Open Internet order was released, several small ISPs announced their intention to abandon investment plans due to heightened uncertainty injected by the reclassification.33Hal Singer, “Three Ways the FCC’s Open Internet Order Will Harm Innovation” (Policy Memo, Progressive Policy Institute, Washington, DC, May 2015).

The emergence of cross-platform competition for data, video, and voice services presents a particular problem for accumulated telecommunications regulations. The old regulatory structures did not anticipate this competitive development enabled by technological advances and the digital revolution. The result is an uneven application of regulation, which discourages investment by the platforms most restricted by regulation. This situation also potentially weakens the incentive for the less-regulated platforms to invest, because they may be insulated from cross-platform competition.

Figure 2. US Broadband Investment by Year

Source: USTelecom, “USTelecom Industry Metrics and Trends 2020,” February 2020, https://www.ustelecom.org/wp-content/uploads/2020/02/USTelecom-State-of-Industry-2020.pdf.

Even when regulatory compliance compels more investment spending, complying will alter the mix of regulations, which introduces distortions that may not produce new or improved goods and services that consumers value more than those they had to give up.34Richard Williams, “The Impact of Regulation on Investment and the US. Economy” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, January 2011). These types of investments crowd out beneficial investment activity in favor of investments offering fewer benefits.35John W. Mayo, “Regulation and Investment: Sk(r)ewing the Future for 21st Century Telecommunications?” (Economic Policy Vignette, Georgetown Center for Business and Public Policy, June 2016).

Professor Richard A. Epstein of the New York University School of Law summarizes the importance of investment in telecommunications:

The adjudication with respect to our telecommunications systems in the next generation will determine, for better or for worse, whether or not this nation, or other nations, will maintain its energetic drive. Every time tough regulations apply to networks, content providers will benefit to some extent in the short run but at the cost of retarding additional investment in the network itself. Voluntary arrangements are still the best way to determine the optimal way to structure interactions between content providers and carriers outside the control of the regulatory state. In the short term, the battle over the Internet may well look like some form of second-best monopolistic competition. Nonetheless, in the long run, allowing technology to be free from regulation will make the system both more competitive and more efficient. The weight of the evidence supports light-handed regulation.36Richard A. Epstein, “Can Technological Innovation Survive Government Regulation?,” Harvard Journal of Law and Public Policy 36 (2013): 97.

The Repeal of Net Neutrality and How It Might Return

The FCC in December 2017 repealed the net neutrality regulations of the 2015 Open Internet order when it issued its Restoring Internet Freedom order.37Restoring Internet Freedom, 83 Fed. Reg. 21927 (May 11, 2018). This reversal was made possible by the change of one FCC commissioner, giving the FCC a 3–2 majority for the party-line vote to repeal.

The Restoring Internet Freedom order, like nearly every other major order by the FCC, was followed by legal challenges. In 2019, the DC Circuit’s decision in Mozilla v. FCC held that the FCC had acted within its legal authority to reclassify ISP services from Title II telecommunications services to Title I information services.38Mozilla v. Federal Communications Commission, 940 F.3d 1 (D.C. Cir. 2019). But the Mozilla decision was not a complete win for the FCC. The DC Circuit pushed back on several specific provisions in the Restoring Internet Freedom order that were not specific to a repeal of the Open Internet order. In particular, the DC Circuit forced the FCC to make changes that related to internet access for public safety purposes, pole attachments for broadband deployment, and benefit eligibility for low-income households.

Most significantly, the Mozilla majority, over the dissent of one judge, struck down a provision in the Restoring Internet Freedom order that would have imposed a blanket preemption on states, preventing them from passing their own net neutrality laws that contravene the FCC’s deregulatory policy. The court’s majority did acknowledge that the FCC has the power to review state laws individually and preempt those that are inconsistent with clearly articulated FCC policies. Even so, the Mozilla decision is likely to lead to years of litigation, and regulatory uncertainty, as states such as California try to impose their own versions of net neutrality.39Professor Daniel Lyons of Boston College Law School provides an excellent analysis of the implications of the Mozilla decision striking down the provision in the Restoring Internet Freedom order that would have preempted states from passing their own net neutrality laws. Daniel A. Lyons, “Conflict Preemption of State Net Neutrality Efforts after Mozilla,” Perspectives from FSF Scholars (Free State Foundation) 14, no. 29 (October 14, 2019).

The repeal of the Open Internet order has also been used as a justification for cities to build and operate their own broadband networks in hopes of achieving certain “net neutrality” outcomes at the local level that supposedly will comply with net neutrality regulations. For example, Mark Howell, the chief information officer for Concord, Massachusetts, claimed in a Washington Post op-ed that the Concord municipal broadband utility is providing a road map for “saving net neutrality.”40Mark Howell, “Saving Net Neutrality, One House at a Time,” Washington Post, April 22, 2018. A report by the American Civil Liberties Union (ACLU) claims that “states, cities, towns, and counties should take matters into their own hands by creating publicly owned services that do honor those [net neutrality] values and can help ensure an open internet.”41American Civil Liberties Union, The Public Internet Option: How Local Governments Can Provide Network Neutrality, Privacy, and Access for All, March 2018, 5.

The ACLU report claims that government-run broadband networks will give more people access to the internet and will promote the “net neutrality” policies the ACLU favors. But then the ACLU goes even further, suggesting that First Amendment rights may be violated unless municipal governments operate their own communications networks.42American Civil Liberties Union, Public Internet Option, 12.

Thus, the ACLU, despite its long and distinguished history of protecting First Amendment free speech rights against government infringement, is now advocating for government ownership and operation of communications networks as a means of protecting free speech, under the beguiling guise of net neutrality. The ACLU report implicitly assumes that local governments can be trusted with this new power to be arbiters of what speech is permissible on the internet. But even leaving aside the issue of giving governments more control over communications networks, government-run broadband providers in the United States have a troubling history of blocking or otherwise restricting online content and failing to respect their users’ privacy concerns.43Enrique Armijo, “Municipal Broadband Networks Present Serious First Amendment Problems,” Perspectives from FSF Scholars (Free State Foundation) 10, no. 11 (February 23, 2015); Enrique Armijo, “A Case of Hypocrisy: Government Network Censors Support Net Neutrality for Private ISPs,” Perspectives from FSF Scholars (Free State Foundation) 13, no. 1 (January 3, 2018).

Policy Reform for Preserving and Promoting a Fast and Open Internet

Ultimately, the uncertainty about the status of internet freedom versus regulation in the name of net neutrality reflects a failure on Congress’s part to give clear guidance to the regulatory agency. Congress should end the FCC’s back-and-forth policy regarding net neutrality with legislation clarifying the issues the FCC has been addressing.

First, rather than leaving the FCC to decide whether to fit ISPs into the Title I or Title II regulatory boxes, Congress should declare what the regulatory policy toward ISPs should be. Ideally, Congress should declare that ISPs should be regulated as they have been—as Title I information services. Then Representative (now Senator) Marsha Blackburn of Tennessee introduced such a bill in 2017. As a compromise, Congress might consider a bill that would retain the ban on the blocking and throttling of internet traffic from the Open Internet order. These bans, while unnecessary in a reasonably competitive market where internet users can switch providers, might allow for a bipartisan agreement by acknowledging some of the concerns raised by net neutrality proponents but also permitting new technologies and applications that can only develop if paid prioritization is tolerated.

Second, Congress should declare under the Commerce Clause of the US Constitution a single national regulatory policy toward ISPs and preclude states from passing their own patchwork of different regulatory regimes. The internet allows people anywhere in the country to interact, with little regard for state borders. Requiring ISPs, edge providers, or anyone else doing business on the internet to keep track of different and potentially conflicting state regulatory requirements can only hold back the growth of exciting new markets and technologies that rely on internet access.44Lyons, “Conflict Preemption.”

Alternatively, if Congress does not act either to clarify its intended regulatory policy toward ISPs or to preempt state regulation in the name of net neutrality, the FCC might seek a bipartisan consensus among FCC commissioners to issue a net neutrality–type regulation that bans throttling and blocking but not paid prioritization. Such a regulation might do little harm and could help ward off the patchwork of state and local regulations that could replace federal regulations.

Third, Congress, as well as the FCC acting according to its power delegated from Congress, should resist the temptation to impose new regulation on the internet and in closely related telecommunications markets. While some eras (as shown in figure 1) are characterized by great regulatory accumulation and others by little or no accumulation, the overall direction has been toward a greater regulatory burden. Some of these regulations are now outdated owing to changes in markets and technologies. Other regulations, like the net neutrality regulations of the 2015 Open Internet order, are overly broad and prescriptive, or are not designed to address anticompetitive harms. It is no coincidence that the era with the least accumulation of new regulation—from 1995 to 2010—was also the era in which the internet and e-commerce emerged and new commerce thrived in the new markets created by rapid growth in internet access in the United States.

Conclusion

Internet service is better than ever since the repeal of the FCC’s net neutrality policy at the end of 2017. Investment in internet infrastructure, which had slowed while net neutrality was in effect, grew in the first year of the order’s repeal. In any event, the outcomes the FCC claimed to be pursuing with the Open Internet order can be better achieved by promoting competition among internet service providers than by regulation that discourages competition and deprives internet users of choices among providers and of applications that can only work with reliable access.

The partisan politics surrounding net neutrality regulations are hard to escape. The FCC’s position on net neutrality will likely continue to seesaw each time the balance of power changes at the agency—which happens each time the presidency switches parties. But solutions are available if Congress acts to adopt a national policy toward internet regulation, one that will embrace vigorous competition among providers and guide both the FCC and state regulatory policies.

References

Al-Ubaydli, Omar and Patrick A. McLaughlin. “RegData: A Numerical Database on Industry-Specific Regulations for all United States Industries and Federal Regulations, 1997–2012.” Regulation & Governance 11 (2015): 109–23.

American Civil Liberties Union. The Public Internet Option: How Local Governments Can Provide Network Neutrality, Privacy, and Access for All. March 2018. 5.

Armijo, Enrique. “A Case of Hypocrisy: Government Network Censors Support Net Neutrality for Private ISPs.” Perspectives from FSF Scholars (Free State Foundation) 13. No. 1 (January 3, 2018).

Armijo, Enrique. “Municipal Broadband Networks Present Serious First Amendment Problems.” Perspectives from FSF Scholars (Free State Foundation) 10. No. 11 (February 23, 2015).

Bolema, Theodore R. “The FTC Has the Authority, Expertise, and Capability to Protect Broadband Consumers.” Perspectives from FSF Scholars (Free State Foundation) 12. No. 35 (October 19, 2017).

Bureau of Economic Analysis. US Department of Commerce. “Industry Economic Accounts Underlying Detail.” News release. October 29, 2019.

Button, Kenneth and David Christiansen. “Unleashing Innovation: The Deregulation of Air Cargo Transportation” (Mercatus on Policy. Mercatus Center at George Mason University. Arlington, VA. November 2014).

Epstein, Richard A. “Can Technological Innovation Survive Government Regulation?” Harvard Journal of Law and Public Policy 36 (2013): 97.

Evslin, Tom. “Internet Fast Lanes: You May Be Surprised by Who Actually Has Them.” Morning Consult. August 4, 2017.

Federal Communications Commission. “Annual Report and Analysis of Competitive Market Conditions with Respect to Mobile Wireless, Including Commercial Mobile Services” (WT Docket No. 16-137. September 23, 2016). 31.

Federal Trade Commission. “Slotting Allowances in the Retail Grocery Industry, Selected Case Studies in Five Product Categories” (Federal Trade Commission Staff Study. November 2003).

Foremski, Tom. “Google Is Building a Private Internet That’s Far Better, and Greener, than the Internet.” ZDNet. March 18, 2010.

Grajek, Michal and Lars-Hendrik Röller. “Regulation and Investment in Network Industries: Evidence from European Telecoms.” Journal of Law and Economics 55. No. 1 (2012): 211.

Hanly, Eric J. and Timothy J. Broderick. “Telerobotic Surgery.” Operative Techniques in General Surgery 11. No. 2 (2005): 173.

Howell, Mark. “Saving Net Neutrality, One House at a Time.” Washington Post. April 22, 2018.

Krol, Robert. “Tolling the Freeway: Congestion Pricing and the Economics of Managing Traffic” (Mercatus Working Paper. Mercatus Center at George Mason University. Arlington, VA. May 2016).

Layton, Roslyn. “Prioritization: Moving Past Prejudice to Make Internet Policy Based on Fact.” AEIdeas. April 17, 2018.

Lyons, Daniel A. “Conflict Preemption of State Net Neutrality Efforts after Mozilla.” Perspectives from FSF Scholars (Free State Foundation) 14. No. 29 (October 14, 2019).

Mandel, Michael and Diana G. Carew. “Regulatory Improvement Commission: A Politically-Viable Approach to U.S. Regulatory Reform” (Policy Memo. Progressive Policy Institute. Washington, DC. May 2013).

May, Randolph J. and Seth L. Cooper. A Reader on Net Neutrality and Restoring Internet Freedom (Potomac, MD: Free State Foundation. 2018).

Mayo, John W. “Regulation and Investment: Sk(r)ewing the Future for 21st Century Telecommunications?” (Economic Policy Vignette. Georgetown Center for Business and Public Policy. June 2016).

McAuliffe, Terry. “Governor McAuliffe Announces Acceptance of Private Sector Proposal to Deliver I-395 Express Lanes Extension.” News release. February 25, 2017. http://www.vdot.virginia.gov/newsroom/statewide/2017/governor_mcauliffe_announces_acceptance111748.asp.

McLaughlin, Patrick A. and Oliver Sherouse. RegData US 3.2 Annual (data set). QuantGov. Mercatus Center at George Mason University. 2020.

Mozilla v. Federal Communications Commission. 940 F.3d 1 (D.C. Cir. 2019).

Pai, Ajit. “Infrastructure Month at the FCC.” News release. Federal Communications Commission. March 30, 2017. https://www.fcc.gov/news-events/blog/2017/03/30/infrastructure-month-fcc.

Pai, Ajit. “Remarks of the Federal Communications Commission Chairman Ajit Pai at the Mobile World Congress” (Speech at the Mobile World Congress. Barcelona, Spain. February 28, 2017).

Preserving the Open Internet. 76 Fed. Reg. 59191, 59194 (September 23, 2011).

Preserving the Open Internet. 76 Fed. Reg. 59192 (September 23, 2011).

Protecting and Promoting the Open Internet. 80 Fed. Reg. 19737 (April 13, 2015).

Protecting and Promoting the Open Internet. 80 Fed. Reg. 19737, 19740 (April 13, 2015).

Protecting and Promoting the Open Internet. 80 Fed. Reg. at 19739.

Protecting and Promoting the Open Internet. 80 Fed. Reg. at 19740.

Protecting and Promoting the Open Internet. 80 Fed. Reg. at 19752.

Protecting and Promoting the Open Internet. GN Docket N0. 14-28(dissenting statement of Ajit Pai. Commissioner. FCC) at 14.

Protecting and Promoting the Open Internet. GN Docket N0. 14-28(dissenting statement of Ajit Pai. Commissioner. FCC) at 10.

Restoring Internet Freedom. 83 Fed. Reg. 21927 (May 11, 2018).

Singer, Hal. “2016 Broadband Capex Survey: Tracking Investment in the Title II Era.” Hal Singer (blog). March 1, 2017.

Singer, Hal. “Three Ways the FCC’s Open Internet Order Will Harm Innovation” (Policy Memo. Progressive Policy Institute. Washington, DC. May 2015).

Verizon v. Federal Communications Commission. 740 F.3d 623 (D.C. Cir. 2014).

Williams, Richard. “The Impact of Regulation on Investment and the US. Economy” (Mercatus Research. Mercatus Center at George Mason University. Arlington, VA. January 2011).

Wright, Joshua D. “Slotting Contracts and Consumers Welfare.” Antitrust Law Journal 74. No. 2 (2007): 440.

Table of Contents

- Regulation and Entrepreneurship: Theory, Impacts, and Implications

- Regulation and the Perpetuation of Poverty in the US and Senegal

- Social Trust and Regulation: A Time-Series Analysis of the United States

- Regulation and the Shadow Economy

- An Introduction to the Effect of Regulation on Employment and Wages

- Occupational Licensing: A Barrier to Opportunity and Prosperity

- Gender, Race, and Earnings: The Divergent Effect of Occupational Licensing on the Distribution of Earnings and on Access to the Economy

- How Can Certificate-of-Need Laws Be Reformed to Improve Access to Healthcare?

- Land Use Regulation and Housing Affordability

- Building Energy Codes: A Case Study in Regulation and Cost-Benefit Analysis

- The Tradeoffs between Energy Efficiency, Consumer Preferences, and Economic Growth

- Cooperation or Conflict: Two Approaches to Conservation

- Retail Electric Competition and Natural Monopoly: The Shocking Truth

- Governance for Networks: Regulation by Networks in Electric Power Markets in Texas

- Net Neutrality: Internet Regulation and the Plans to Bring It Back

- Unintended Consequences of Regulating Private School Choice Programs: A Review of the Evidence

- “Blue Laws” and Other Cases of Bootlegger/Baptist Influence in Beer Regulation

- Smoke or Vapor? Regulation of Tobacco and Vaping

- Moving Forward: A Guide for Regulatory Policy