Introduction

An energy technology transition is under way as digital technologies and low-carbon energy technologies fall in costs and proliferate in the electricity system. Solar and wind power, once unaffordable and uncommon, now make up over 8% of electricity generation and are poised to rise further.1 United States Energy Information Association. “What is U.S. electricity generation by energy source?” Available at https://www.eia.gov/tools/faqs/faq.php?id=427&t=3. Many states have net metering regulations, allowing rooftop solar owners to participate in the electric grid as distributed and decentralized energy producers. Despite stalling at the federal level, policies at the state level are requiring utilities to transition from fossil fuels to clean energy. As of 2018, 29 states had some form of “renewable portfolio standard,” while others have energy efficiency mandates or green power options. Even transportation has been affected—electric and hybrid vehicle sales composed almost 5% of 2017 vehicle sales in California.2 Bellan, Rebecca. “The Grim State of Electric Vehicle Adoption in the U.S.” CityLab, October 15, 2018. Available at https://www.citylab.com/ transportation/2018/10/where-americas-charge-towards-electric-vehicles-stands-today/572857/

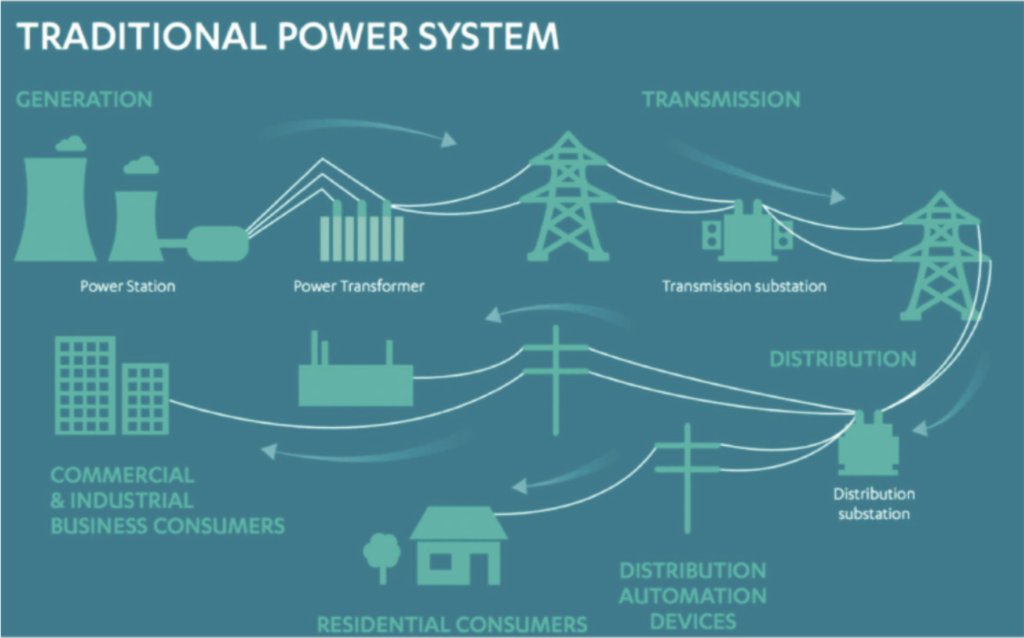

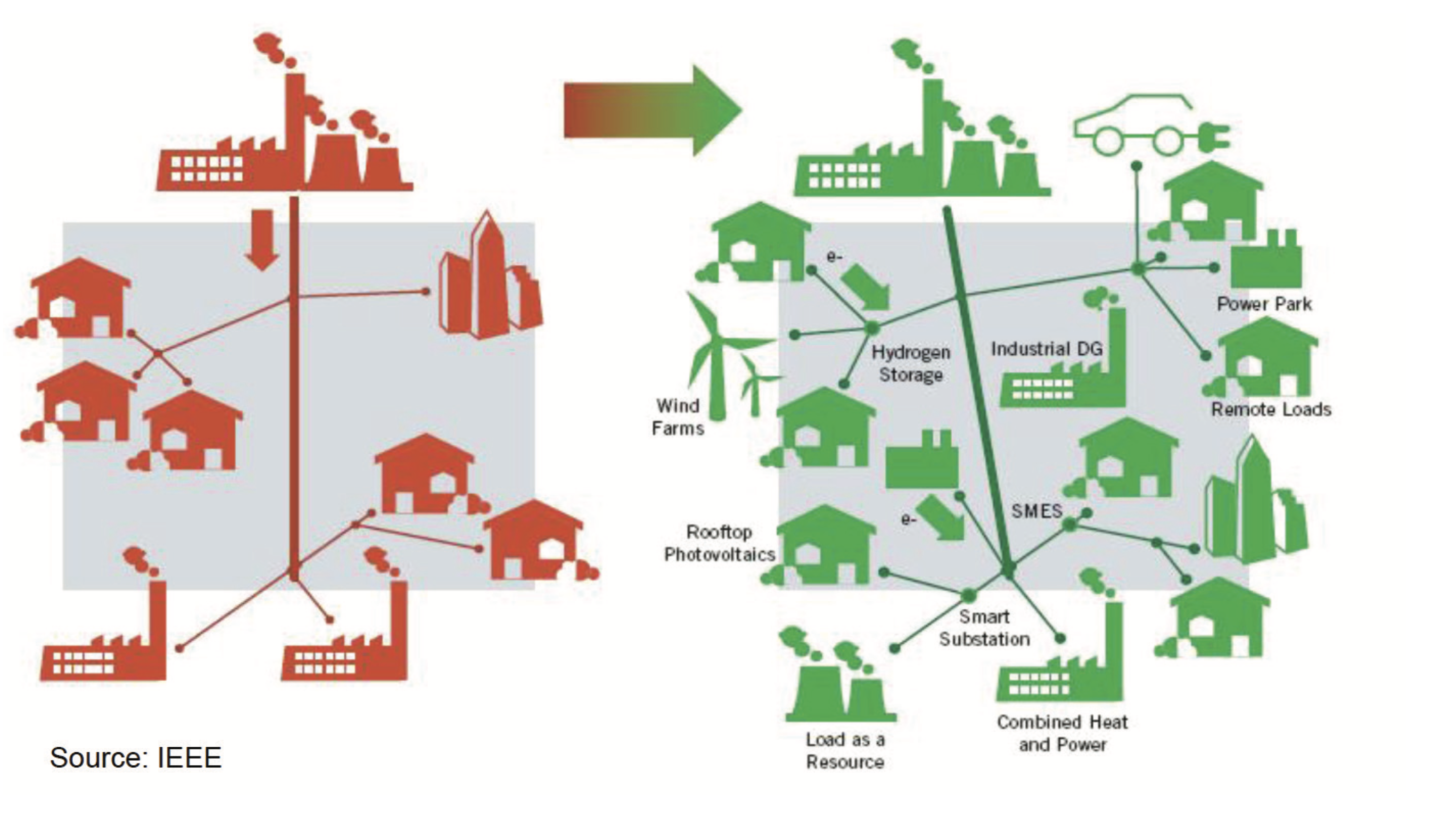

These changes are affecting an industry that has been a vertically integrated regulated monopoly for over a century, and this transition will have substantial implications for the value propositions available to consumers, the utility business model, and the regulatory framework. The 20th-century regulated utility sent energy in a one-way flow from generators to consumers (as seen in Figure 1), controlling delivery and reliability of a basic electric service from a centralized control room. The utility was the only provider of the grid services, such as voltage regulation, required for delivery and grid balance. Its profit relied on volume-based pricing determined administratively through regulatory proceedings rather than markets. In this design, demand was assumed to be “dumb” and inelastic. Today’s innovations will affect all of those features of the status quo.

Figure 1. One-Way Flow in the Traditional Power System

Source: Kristov, Lorenzo. Power System Evolution from the Bottom Up. October 25, 2018.

Parallel to technological changes in distributed energy resources (DERs) are changes in digital technologies and automation. In 2002, 62% of American adults owned a cell phone. In 2018, 96% own at least one, with 81% owning a smartphone.3Pew Research Center Mobile Fact Sheet. Available at https://www.pewinternet.org/fact-sheet/mobile/. Along with the proliferation of cell phones, many new devices attempt to connect other aspects of consumers’ lives through technology. Smart speakers, released only five years ago, are now owned by one in six Americans.4Perez, Sarah. “39 million Americans now own a smart speaker, report claims.” TechCrunch, January 12, 2018 Available at https://techcrunch.com/2018/01/12/39-million-americans-now-own-a-smart-speaker-report-claims/. Smart home systems and devices attempt to bring technology even further into day-to-day activities, with options to automate and remotely control lighting, heating, and home security. Adoption of these new technologies is increasingly driven by affordability. These technology trends suggest that the energy future will be lower carbon, more digital, more automated, and more decentralized. It is also likely to involve more market processes to enable and implement coordination in an increasingly decentralized system, as digitization drives down transaction costs.

Consider, for example, a homeowner (let’s call her Anna) with rooftop solar and an electric vehicle (EV), two DERs. Anna’s solar panels primarily supply her own consumption, including charging her EV. Anna is a “prosumer.” At times, though, the solar panels generate more energy than Anna needs. Current net energy metering regulations pay her for the energy she puts on the grid, but from a system perspective that flow is not timed well, so when all of the net metering customers put their excess energy on the grid it strains grid operations. The distribution grid was not designed for such uncoordinated two-way flow. In this situation, Anna’s clean distributed energy disrupts the grid, when it could instead be a valuable resource supporting grid operations and balance. Decentralized local energy markets and markets for grid services would enable Anna to earn revenue from selling her excess capacity while also coordinating with others and with grid conditions, turning her solar excess capacity into a true resource.

Now think about Anna’s electric vehicle. Owning an EV is actually a more profound change to the distribution system because it is an intertemporal resource—it uses energy to charge the battery and stores energy to discharge later. An EV is also capable of being a bi-directional resource, with EV owners setting bid prices to charge the battery and offer prices to discharge, using automation in local energy markets. The combination of distributed solar and storage makes Anna’s resources flexible, one of the most important capabilities in a decentralized distribution grid that requires real-time physical balance. From a distribution system perspective the EV acts like a sponge that can provide flexibility and resilience by charging and discharging when it is beneficial to both Anna and others around the distribution grid, as well as those who operate the grid itself.

How would she know when her DERs are a valuable resource to others and for grid balance? A robust framework for communicating that message to her and others is a price system—decentralized markets that connect DER owners and enable them to provide both energy and grid services at times when they are more valuable, rather than just when the sun is shining. (The role of storage for flexibility here is crucial.) As needs and available resources change over minutes, hours, and days, those changes show up in the prices that emerge from the markets for energy and for a range of grid services. Anna’s home energy management system would use algorithms to automate submitting her bids and offers to the market, and the market algorithm would establish the market-clearing price and send a message to her system telling it what actions to take. Note how different this scenario and these opportunities are from the current regulated monopoly context.

The analysis presented here explains how digitization of the electric system makes this scenario possible and mutually beneficial. DER owners can realize their assets’ full potential, through their own consumption and by participating in local energy markets, and can also create value for others in the distribution system, by selling the use of their DERs for energy and for grid services. Enabling this potential has implications for the architecture of the distribution grid, utility business models, and regulatory frameworks, in both the near future and the long term.

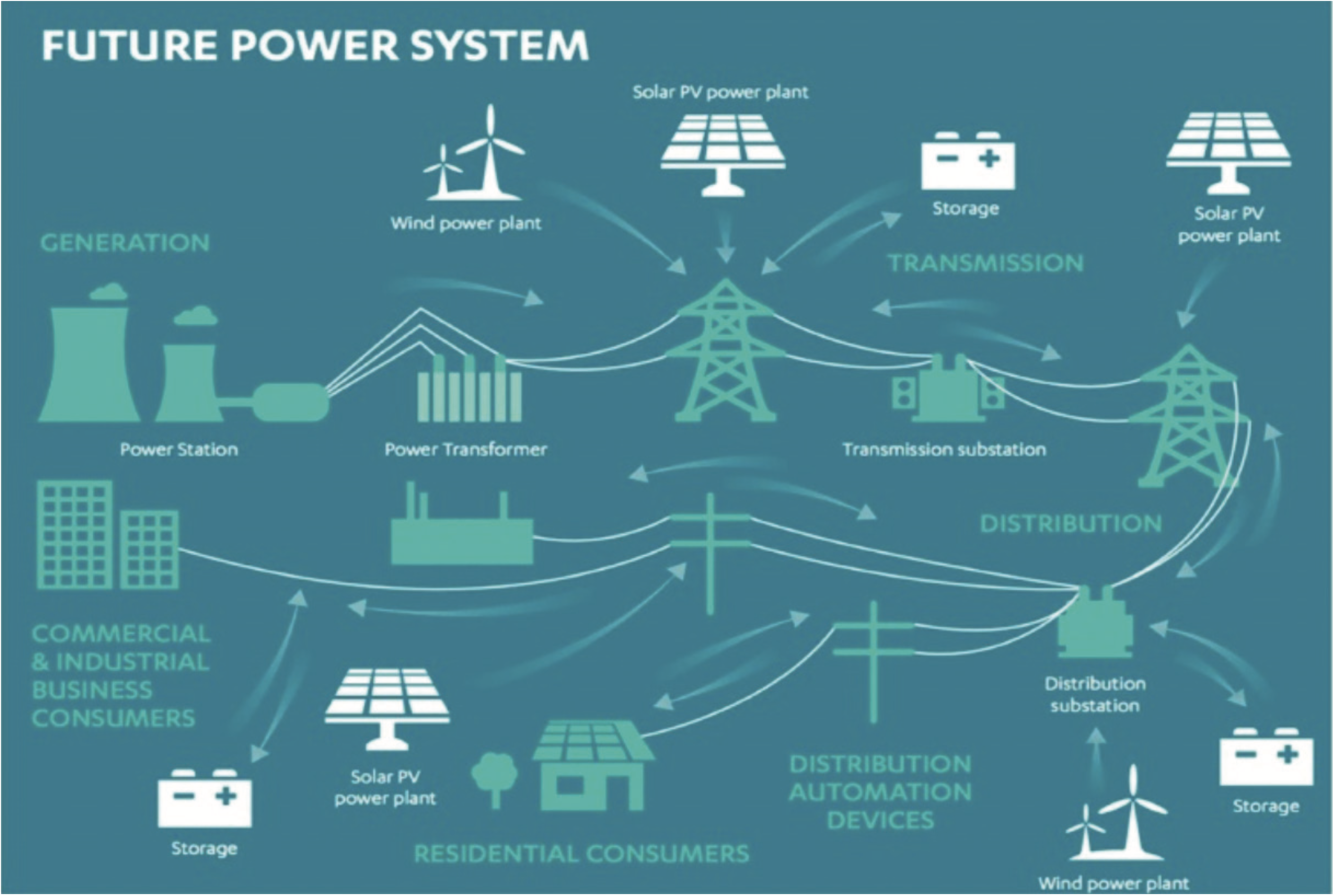

The falling costs of DERs and the digital technologies that can interconnect them to the distribution grid and automate their actions are leading to this energy transition, resulting in a more diverse power system, as shown in Figure 2.

Figure 2. Two-Way Physical Flow in the Future Power System Source: Kristov, Lorenzo. Power System Evolution from the Bottom Up. October 25, 2018.

Source: Kristov, Lorenzo. Power System Evolution from the Bottom Up. October 25, 2018.

Digital and DER technologies make possible a transition to a more decentralized distribution grid that can take advantage of small-scale low-carbon resources. The widespread implications of these possibilities also include the electrification of transport, automation in building systems in commercial and residential buildings, and even the ability to use a homeowner’s water heater tank as a flexible energy storage resource. These examples illustrate how digital and DER innovations will change the possible opportunities for value creation in and around the distribution grid. “I flip the switch and the light goes on” is no longer the only value proposition that electricity distribution and retail offer for residential customers.

This analysis provides a primer on DER innovation and digitization to lay a foundation for thinking about the institutional implications of technological change. The dynamic nature of these changes makes detailed recommendations difficult, so instead I offer an analytical framework for understanding implications for the utility business model and for regulation.

Digitization and the energy technology transition imply that the utility business model should evolve to enable communities to take advantage of these new value opportunities and these reductions in transaction costs. This analysis explores a platform business model for the utility as a distribution system operator (DSO) and coordinator of the grid services required for grid operations.

Regulatory institutions should also evolve in several ways to take advantage of the increasing diversity of technologies and value opportunities, and of the reductions in transaction costs arising from digitization. Potential changes to regulation fall into two categories: changes to what is regulated and changes to the form regulation takes. In particular, targeting the regulatory footprint to the part of the electricity supply chain that still has natural monopoly characteristics would reduce barriers to innovation and experimentation in clean energy systems. Many states still have vertically integrated regulated monopolies despite the fact that the wires network is the only part of the supply chain that still has natural monopoly characteristics.5Joskow, Paul. “Regulation of Natural Monopoly.” Handbook of Law and Economics 2 (2007). 1227–1348 Changing the regulatory footprint implies regulatory restructuring in those states.

Changes to the form of regulation have several dimensions, most relating to how regulated rates are determined. Continuing the ongoing move toward time-varying and dynamic rates for both energy and network costs would provide more accurate information to consumers, increasing coordination and operational efficiency and enabling DERs to be system resources. Some state regulatory commissions are already moving away from volumetric cost-based rates toward more performance-based rates for regulated functions.6Lazar, Jim, and Wilson Gonzalez. Smart Rate Design for a Smart Future. Regulatory Assistance Project. July 2015. 71. Using outcome-focused performance-based regulation rather than cost-based rate setting for functions within the regulatory footprint would enable the DSO-grid service coordinating platform to earn revenue commensurate with its performance of these activities. Finally, evolving away from existing net metering regulations toward decentralized local markets would reward DER owners for providing grid services and would better enable coordination across time and place. These changes require rethinking the enterprise of regulation for a dynamic digital economy and modifying existing rules and procedures to adapt to these changes.

This combination of technological and institutional change is a way to harness new ideas for economic and environmental benefits, to create a clean and prosperous energy future.

Technology and Innovation in Electricity: Digital and Distributed Resources

The profound technological changes of the past two decades are changing the operations, the economics, and the architecture of the electric power network in a process of grid modernization. Growing consumer-facing digital technologies to automate and manage energy use, as well as the increasing penetration of electric vehicles and other DERs, are bringing the digital economy into electricity in many different ways. These changes are creating an impetus for grid modernization and for rethinking the utility business model and traditional regulatory frameworks.

Grid modernization involves increasing the communications capabilities of the distribution grid. An intelligent grid “uses digital communications technology, information systems, and automation to detect and react to local changes in usage, improve system operating efficiency, and, in turn, reduce operating costs while maintaining high system reliability.”7United States Department of Energy. Quadrennial Energy Review: Transforming the Nation’s Electricity System. 2017. 1–15. As a result of grid modernization over the past decade, the DERs that are increasingly being interconnected in the electric power system are coupled electronically to the grid. Digital interconnection facilitates DER investment and uses automation to make DERs into flexible grid resources.

The Growth of Distributed Energy Resources

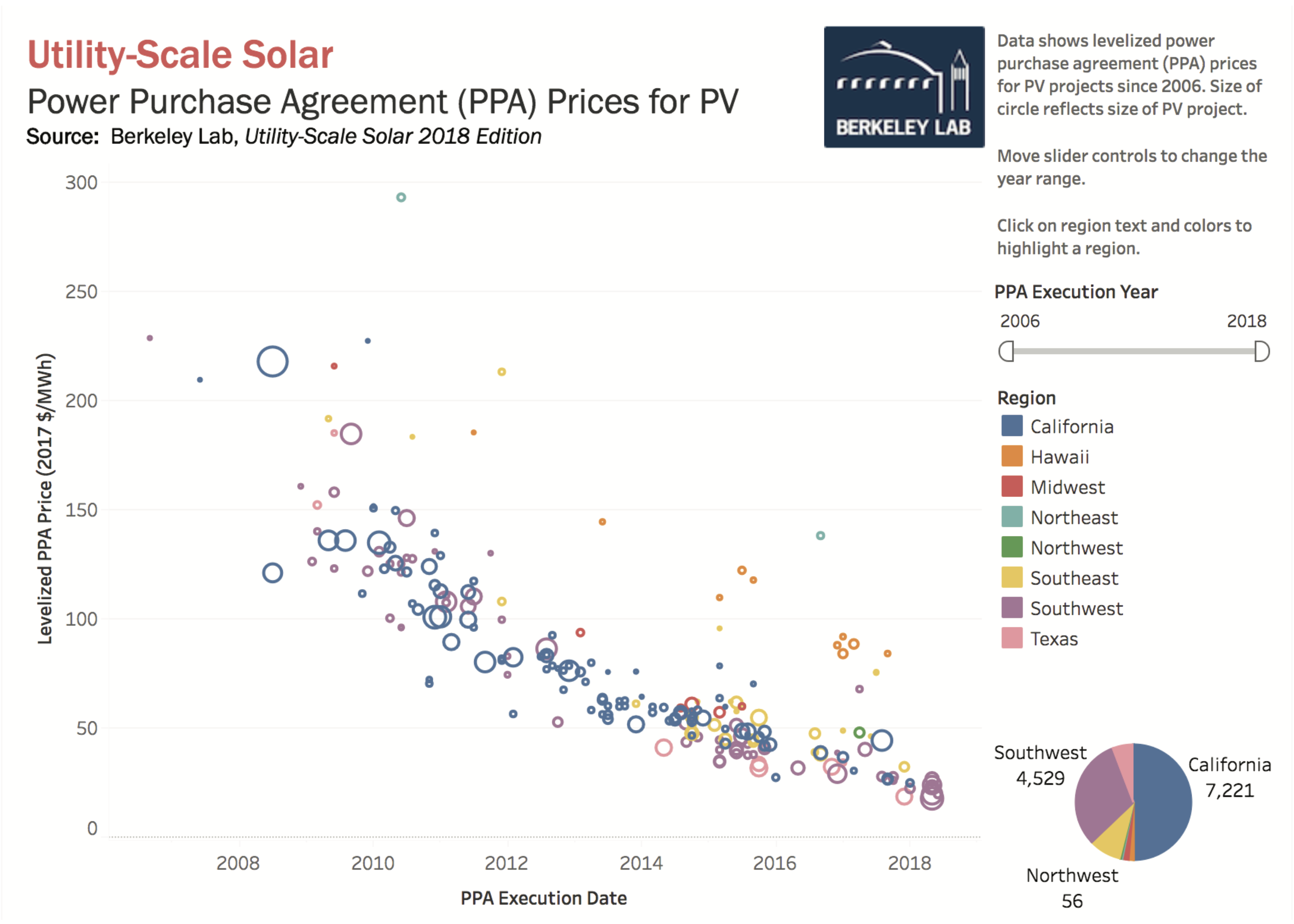

This analysis focuses on distributed or “behind-the-meter” resources such as residential solar, storage, and electric vehicles. Solar photovoltaic costs have fallen over the past decade as solar technologies have improved in performance. In 2017 combined utility-scale and distributed solar accounted for 31% of new generation capacity, driven by the combination of falling installation and equipment costs, requirements for utilities to meet state renewable portfolio standards, and increasing customer preferences (particularly the preferences of large commercial customers) to purchase low-carbon electricity.8Berkeley Lab. Utility-Scale Solar 2018. Available at http://utilityscalesolar.lbl.gov. As of 2018 cumulative operating solar photovoltaic (PV) capacity in the US is 62.4 gigawatts, 75 times the installed capacity in 2008.9Wood Mackenzie/SEIA U.S. Solar Market Insight. March 2019.

Figure 3. Utility-Scale Solar Power Purchase Agreement Prices 2008–2018 Source: Berkeley Lab, Utility-Scale Solar 2018.

Source: Berkeley Lab, Utility-Scale Solar 2018.

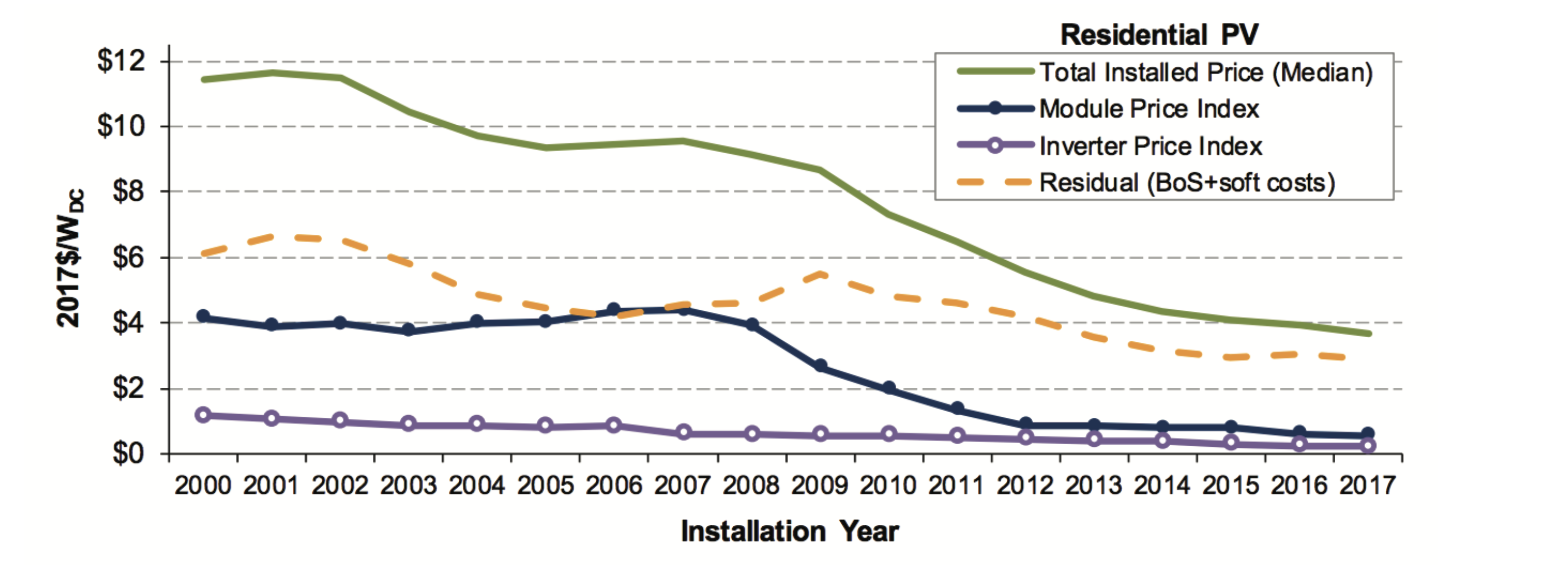

Figures 3 and 4 indicate the cost reductions in utility-scale solar and distributed residential solar, respectively. Distributed solar is more expensive to build and install, but those costs have fallen since 2008 due to reductions both in hardware costs and installation “soft costs.”10Berkeley Lab. Tracking the Sun 2018. 21.

Figure 4. Prices and Costs for Residential PV Systems, 2000–2018 Source: Berkeley Lab, Tracking the Sun 2018.

Source: Berkeley Lab, Tracking the Sun 2018.

Hagerman et al. estimated that in 2015 residential solar had achieved subsidy-free “socket parity“ (price equivalence with grid-supplied power) only in Hawaii.11Hagerman, Shelly, Paulina Jaramillo, and M. Granger Morgan. “Is Rooftop Solar PV at Socket Parity Without Subsidies?” Energy Policy 89 (February 2016). 84–94. Other sources suggest that renewables more generally have reached grid power price parity in global comparisons; see, for example, Motyka, Marlene, Andrew Slaughter, and Carolyn Amon. “Global Renewable Energy Trends.” Deloitte Insights. September 2018. Available at https://www2.deloitte.com/insights/us/en/industry/power-and-utilities/global-renewable-energy-trends. html?id=us:2sm:3li:4di4624:5awa:6di:MMDDYY::author&pkid=1005414. And in 2017 seven states had achieved socket parity—all had either abundant sunshine or net energy metering regulations that compensated solar owners the full retail rate for their net excess generation.12Vaishnav, Parth, Nathaniel Horner, and Ines L. Azevedo. “Was It Worthwhile? Where Have the Benefits of Rooftop Solar Photovoltaic Generation Exceeded the Cost?” Environmental Research Letters 12 (2017).

Despite its current higher costs, residential solar can yield different benefits from utility-scale solar, at an individual, community, and system level. Homeowners with strong environmental and/or local community engagement preferences may perceive rooftop solar as yielding different and larger benefits than other alternatives, because they are taking deliberate actions and engaging in mutually beneficial exchange with their neighbors. Small-scale community solar farms offer multi-unit dwelling residents a similar opportunity, even if they do not own a roof. Its smaller scale can make it a more flexible resource, especially if paired with storage. By increasing the distributed nature of the system, an interconnected network of small-scale solar can increase system resilience in response to unanticipated events or external threat.13National Association of Regulatory Utility Commissioners. The Value of Resilience for Distributed Energy Resources: An Overview of Current Analytical Practices. April 2019.

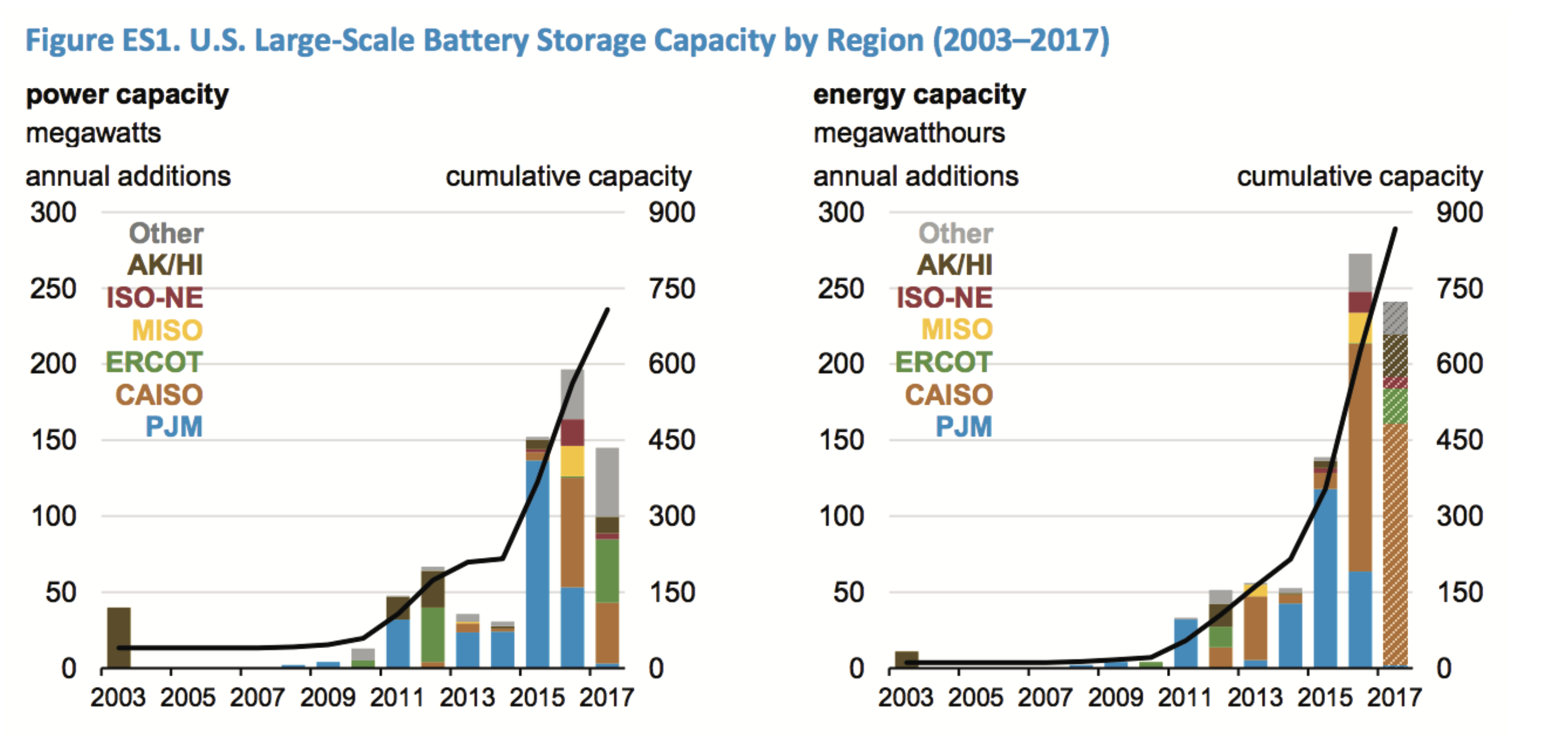

Energy storage of different types (electrical, thermal, mechanical, and electrochemical) and at different scales has started to increase as technologies improve and costs fall. The largest changes have been in electrochemical or battery storage. Bloomberg New Energy Finance estimates that the cost of electricity from batteries has fallen by 76% since 2012.14Mai, H.J. “Electricity Cost from Battery Storage Down 76% Since 2012: BNEF.” Utility Dive. March 26, 2019. Available at https://www. utilitydive.com/news/electricity-costs-from-battery-storage-down-76-since-2012-bnef/551337/. Grid-scale battery storage in the US has increased since 2015, particularly in the mid-Atlantic region (the PJM Regional Transmission Organization territory), as shown in Figure 5.

Figure 5. Grid-Scale Battery Storage Capacity Source: United States Department of Energy. Battery Storage Market Trends 2018.

Source: United States Department of Energy. Battery Storage Market Trends 2018.

Smaller distributed “behind-the-meter” storage systems are more expensive due both to equipment and installation costs at smaller scale, but their costs are also starting to fall.15Lazard. “Levelized Cost of Storage 2017.” Available at https://www.lazard.com/perspective/levelized-cost-of-storage-2017/. Performance improvement and falling costs for behind-the-meter battery storage arise in part from developments in a complementary DER: electric vehicles (EVs).

Battery innovations have increased the range between charges and have improved battery performance for EVs. A meta-analysis from Bjorn Nykvist and Mans Nilsson surveyed 80 peer-reviewed analyses and estimated that global lithium-ion battery production costs fell 14% per year between 2007 and 2014, and were falling faster than previous forecasts had estimated.16Nykvist, Bjorn, and Mans Nilsson. “Rapidly Falling Costs of Battery Packs for Electric Vehicles.” Nature Climate Change 5 (March 2015). 329–332. Combined with falling production costs from large-scale production and tax credits that have provided subsidies to purchasers, the number of EVs sold in the US has quadrupled from 2012 to 2017, although they currently comprise only 1% of the automobile market.17Wagner, I. “U.S. Electric Vehicle Industry—Statistics and Facts.” Statista. January 31, 2019. Available at https://www.statista.com/topics/4421/the-us-electric-vehicle-industry/.

The importance of EVs as a DER derives from their distinct and special nature compared to other resources. An electric vehicle is both automobile and storage, so it can play two roles in the distribution system in a way that is not true for other resources—it consumes electricity to charge, and can provide electricity to others with a battery discharge. An electric vehicle enables its owner to be both a buyer and a seller of electricity, and to take on those roles depending on that person’s preference at the time for using the vehicle and depending on the state of the system and the market (i.e., is the market price at least as high as the price the owner is willing to accept?). Its storage capability, combined with its ability to either use or provide energy, makes it a flexible resource if interconnected on the distribution grid and connected to other people in a decentralized market. Even in the absence of decentralized energy markets in the near term, EVs can serve as storage and provide grid services. Lazar (2019) argues that as a device, an electric vehicle already behaves like a water heater, and that with digital interconnection and better pricing, EVs can engage in “smart charging.”18Lazar, Jim. “Electric Cars Are a Lot Like Water Heaters.” Regulatory Assistance Project, August 28, 2019. Available at https://www.raponline.org/blog/electric-cars-are-a-lot-like-water-heaters/. Lazar frames his argument for time-varying rates and smart charging within avertically integrated, regulated structure, in which both energy prices and network charges are determined administratively through regulatory processes. His logic generalizes to the case in which, instead, decentralized energy markets and markets to provide grid services exist, but in that case, the only functions subject to regulatory rate determination would be those associated with energy delivery, provision of some grid services, and the coordination of grid services provided by DERs.

This intertemporal and bi-directional capability has profound implications for changing the architecture of the distribution grid and how it operates. The electro-mechanical technologies of the 20th century created a one-way flow from large-scale, centralized generators to end users. Now, with more DERs in general and with the flexible capabilities of EVs, a distribution grid that can take advantage of those capabilities must enable two-way flow of energy and be more aware of both the possible disturbances and resilience benefits that arise from these distributed resources throughout the system, as illustrated in the right-hand panel of Figure 6.

Figure 6. Existing Grid Architecture and Digital + DER Grid Architecture

The Distribution Grid’s Digital Technologies

Operating a safe and reliable electricity distribution grid is challenging at all times. Delivering the electricity service that end users desire and purchase requires more than simply connecting generators to consumers. Even in a one-way network without distributed resources and without digital technologies this process is complicated and intricate—it requires multiple different grid services to maintain that current flow and keep it in the range of voltage and frequency for which the distribution grid is designed. These grid services are essential to reliable service and resilient networks.

Energy analysts Jamie Mandel, Tanuj Deora, and Lisa Frantzis define grid services in five categories: energy, capacity, flexibility, operating reserves, and power quality.19Mandel, Jamie, Tanuj Deora, and Lisa Frantzis. “Distributed Energy Resources 101: Required Reading for a Modern Grid.” Smart Electric Power Alliance. January 26, 2018. Available at https://sepapower.org/knowledge/distributed-energy-resources-101-required-reading-moderngrid/. Some of those categories are more important at the bulk power/wholesale market system level, while others (particularly power quality) have traditionally been more important at the distribution level.20United States Department of Energy. National Renewable Energy Laboratory. An Introduction to Grid Services: Concepts, Technical Requirements, and Provision from Wind. By Paul Denholm, Yinong Sun, and Trieu Mai. 2019. More simply, David Patton argues that the only fundamental energy products are energy and reactive power (so the fundamental services are the provision of them), and that providing other services (e.g., reserves, capacity, power quality other than reactive power) is providing “options on energy in different timeframes.”21Patton, David. “Resilience and Emerging Issues in Wholesale Electricity Markets.” Presentation, Energy Conference, Energy Information Administration. June 2018. In the traditional vertically integrated regulated utility structure, the utility plans for, provides, and controls all grid services in the delivery of energy from generators to consumers.

In a decentralized distribution grid with DERs, though, parties other than the utility can provide grid services, and can do so in ways that make the grid more resilient.22National Association of Regulatory Utility Commissioners. The Value of Resilience for Distributed Energy Resources: An Overview of Current Analytical Practices. April 2019. Decentralization means that grid coordination and balance happen throughout the network, not through a centralized control room. DERs vary in size, in location, and in how quickly they can change their settings and behavior. Such scale, spatial, and temporal diversity means that different resource owners can profit from selling grid services to address local balancing issues.

Digital sensors, monitors, and circuit breakers embedded in the grid, in substations and transformers, create a digital-mechanical network that enables the flow of both electric current and data. This network forms the basis for distribution automation (DA):

… a family of technologies including sensors, processors, communication networks, and switches that can perform a number of distribution system functions depending on how they are implemented. Over the last 20 years, utilities have been applying DA to improve reliability, service quality and operational efficiency. More recently, DA is being applied to perform automatic switching, reactive power compensation coordination, or other feeder operations/control.23“Definition: Distribution Automation.” Open Energy Information. Accessed July 11, 2019. Available at https://openei.org/wiki/Definition:Distribution_Automation.

This communication network sends data autonomously to the utility control center, creating a more accurate and complete model of the network while providing information for the control center engineers to use to understand the physical state of the distribution grid at any time. Embedded digital technologies and grid modernization make the grid visible in ways and at a scale of precision that it has never been before. Control room operators can be more aware in real time of the grid’s operations, which gives them more precision in managing flows and improving the operating efficiency of the grid, even in a future in which much of the coordination occurs at a decentralized level.

Such an integrated operational and information network can also improve both reliability and resilience. One of the biggest impacts of grid modernization and distribution automation is on outage response. Distributed digital technologies enable autonomous identification of outages without customers having to alert the utility directly, targeting crews and trucks specifically to those locations. Fault detection and repair technologies can even perform some repairs and restore service remotely without the need for human intervention, reducing the time and cost associated with outages.

The ability to restore service quickly is a primary feature of both reliability and resilience, and resilience adds the capability of the system itself to bounce back after an unanticipated event. One characteristic of resilient systems is the ability to isolate damage and reduce or prevent its propagation, and digital technologies contribute to such resilience by making it feasible and cheaper to operate the grid in a more decentralized manner. For example, over the past decade Florida Power & Light has invested $2 billion in grid modernization. When Hurricane Matthew hit Florida in October 2016, most of their 1.2 million affected customers had service restored within three days; before these smart grid investments, restoration times for a storm like that would have been 10–15 days.24United States Department of Energy. Quadrennial Energy Review: Transforming the Nation’s Electricity System. 2017. 4–42.

An increased share of DERs in the distribution grid can also increase resilience because of the benefits of network decentralization, even though in the short run DERs are creating operational challenges and forcing changes in the centralized ways that utilities have traditionally operated their grids. DERs enable more decentralized energy generation that can make the system more resilient, and they can also provide some important grid services at a smaller, more decentralized level within the network, so they can contribute to resilience in multiple ways.25Denholm, Paul, Yinong Sun, and Triong Mai. An Introduction to Grid Services: Concepts, Technical Requirements, and Provision from Wind. National Renewable Energy Laboratory Technical Report NREL/TP-6A20–72578. January 2019. See also “Technical Appendix A: Detailed Overview of Services.” The Economics of Battery Storage. Rocky Mountain Institute. 2015.

The digital capabilities to monitor, coordinate, and control grid activity also allow increased capacity utilization without reducing reliability. A grid’s capacity is the aggregate amount of a particular activity (generation, delivery, consumption) that it can accommodate at the same time. In a non-digital grid where centralized operators control flows with limited information, a significant amount of capacity needs to be left unused, in reserve to provide a buffer against unexpected and changing conditions. In digital grids with increased system awareness, visibility, and automation, such excess capacity buffers are less necessary and less valuable, so a portion of that excess capacity can be used more valuably in other ways. For example, a traditional grid operator typically targets a reserve margin of about 15% running and ready to dispatch at all times means enough available energy to meet unexpected demand or unanticipated supply outages.26Denholm, Paul, Yinong Sun, and Triong Mai. An Introduction to Grid Services: Concepts, Technical Requirements, and Provision from Wind. National Renewable Energy Laboratory Technical Report NREL/TP-6A20–72578. January 2019. 4. This excess generation capacity also means additional production costs and additional pollution emissions. The capital that would have been invested in those reserve assets can be more valuably used elsewhere due to digital innovation, and emissions also fall as a consequence of more precise coordination of demand and supply. Digital monitoring and automation increases the flexibility of the distribution grid and increases the opportunity cost of high reserve margins. Higher capacity utilization means fewer wasted and idle resources, higher economic efficiency, and lower cost per unit of activity.

Increased DERs and a more heterogeneous distribution grid introduce coordination and control challenges to an already complex system, but a system benefit they create is increased system capacity. Interconnecting DERs using the monitoring, coordination, and control capabilities of digital technologies makes it possible for these DERs to live up to their name and serve as resources to provide energy, grid services, and a means of increasing capacity utilization and reducing investment in resources that will sit idle much of the time. Prices and market processes can facilitate harnessing DERs owned by different parties and enabling them to benefit from being “prosumers.”

One framework for designing technology-enabled retail electricity markets is transactive energy (TE). In a TE system, electricity end-use digital devices are programmed to set the prices they are willing to pay to operate at their current settings, to submit those prices as bids into a digital market, and to change their settings if the market-clearing price is higher than the device is programmed for. For example, a homeowner can program a two-way communicating thermostat with a price that represents how much the homeowner is willing to pay per kilowatt-hour to keep the temperature in the home at its current level. The thermostat bids that price into a digital retail market, and if the market-clearing price is lower than the set price, the thermostat is unchanged; if the market-clearing price is higher than the set price, then the thermostat is programmed to change its settings by, say, increasing its temperature by three degrees so the air conditioning does not operate as often. TE systems also enable a tiered or layered network architecture in which markets can exist and transactions can occur at different levels of aggregation.

Markets provide valuable, flexible, responsive coordination in a DER-rich distribution grid by enabling prices to emerge out of the interactions of participants and the physical state of the grid at a given time. Using market-enabled DERs for energy and for grid services can also reduce wasteful investment in costly excess generation capacity that is built to meet peak demand and sits idle for much of the year.

In the future the distribution grid is likely to evolve toward more decentralized markets, with more accurate locational marginal pricing of energy, grid services, and the wires company’s delivery services. TE systems harness the transaction cost reductions from digitization to provide a network and market design that can enable locational marginal pricing to the extent that is feasible at a given time. Below that organizational level in the grid, aggregators (such as retail suppliers or multi-unit building owners) can optimize their energy systems based on the price signals emerging from the market layers above them.

Consumer Devices Around the Distribution Edge

A related change in distribution digitization is consumer devices around the distribution grid edge. The gateway between the consumer and the grid is the electric meter that measures the amount of electricity consumed. Increasingly, consumers have digital meters and these meters generate more, and more accurate, data about their energy use. Almost half of all electric meters in use in the US in 2016 were advanced digital meters.27United States Federal Energy Regulatory Commission. Assessment of Demand Response & Advanced Metering. Washington, D.C.: Federal Energy Regulatory Commission, 2018. 3. On average 47.1% of residential customers have digital meters, with Texas having the highest residential penetration rate at 86.1%.28United States Federal Energy Regulatory Commission. Assessment of Demand Response & Advanced Metering. Washington, D.C.: Federal Energy Regulatory Commission, 2018. 5. Whether or not consumers have useful access to their consumption data depends on the utility’s rules, though.

Over time, these advanced digital meters and other widely available in-home technologies (like smart speakers), will allow consumers to exercise more control over their energy consumption and production decisions. They will also be able to use these technologies to benefit from providing essential flexibility in the distribution system, especially in a transactive energy system that enables informative local prices to emerge.

Another type of digitally enabled system around the distribution edge is a microgrid.29Microgrid Institute. http://www.microgridinstitute.org/about-microgrids.html. Microgrids are self-contained interconnected users of the electric system that can as a system disconnect (or “island”) from the distribution grid and still maintain service and operation for the microgrid participants. One example of a way to use a microgrid is a neighborhood that has, for example, a hospital with high reliability requirements and neighboring office and apartment buildings where there are distributed energy resources located within the neighborhood. The hospital may have its own attached small generator, and others in the neighborhood may have solar and electric vehicles. If this neighborhood has enough generation capacity to support its consumption in the event of a distribution grid outage, and it is structured as a microgrid, then it can detach (island) quickly from the grid to avoid the outage. The DER owners make providing grid services and energy possible from the microgrid. Digital technologies that connect all users together through a communication network and that provide a control interface with the distribution grid make a microgrid possible. Microgrid structure also can make the distribution system more resilient by making the network more decentralized and therefore harder to harm.

These various digital consumer devices and microgrids around the distribution edge can increase grid resilience and provide environmental benefits by increasing capacity utilization and by increasing the share of generation from renewable resources. Realizing these benefits, though, requires that distributed energy resource owners, consumers with smart homes, and microgrids are able to interconnect on the distribution grid. In other words, they have to be able to connect and disconnect using both economic and physical signals, using prices emerging from markets and algorithms used for automation to coordinate their decisions and actions, as described above in transactive energy systems.

Network Technologies: Blockchain for Energy

Digital network technologies like blockchain also decrease costs of interconnecting DERs into a decentralized, transactive network. At its core, blockchain is a distributed ledger technology that allows multiple parties to share a common database infrastructure. Traditionally, a database resides on a computer server, with parties exercising centralized editorial control over the single copy of the database. For example, a credit card company owns and operates a single stored database with customer information and has editorial control over the data contained there. The data on customer identity and transaction history are valuable, both to the transacting parties and to the trusted third party, and the third party’s ownership and control of the data is a big part of their value as an intermediary. A distributed ledger technology like blockchain reduces (or removes) the need for an intermediary in payment systems and transaction settlement.30Blockchain’s role in energy systems and markets is a current topic of debate, particularly with respect to the transaction settlement time, which may be too long to be suitable to some grid services with extremely small time scales.

Blockchain builds trust by providing a single shared ledger to support secure, transparent, and frictionless transactions among members. Blockchain enables systems to establish identity and interact based on that identity, forming reputations over time. Blockchain-enabled systems can create contracts to enable shared problem-solving, resource allocation, and machine-to-machine (M2M) contracts that embed a contract between two parties into an algorithm that automates contract fulfillment. Such transactions provide clear information to support local investment and local innovation, and the technology platform enables dissimilar systems from diverse manufacturers to interact with trust.

One example of a blockchain-based local energy market is a new pilot experiment at the Sacramento Municipal Utility District (SMUD). SMUD is partnering with Électricité de France (EDF) and Omega Grid to use a blockchain-based token system to coordinate EV charging with solar energy production.

The pilot project will offer blockchain-based “tokens” for charging vehicles when there’s a surplus of solar power on the local grid. The value will fluctuate based on the amount of solar being produced within a specific substation. Participants will have access to a web-based dashboard and receive notifications by email or text to alert them to upticks in solar generation, said Killian Tobin, CEO and co-founder of Omega Grid. Customers who plug in vehicles during these periods will be rewarded with blockchain tokens that can be spent at participating merchants. An option to convert tokens to cash is likely, as is the case in Burlington, Vermont, where the municipal utility uses Omega Grid software for a demand response program.31Thill, David. “Chicago Startup Will Help Test Hyperlocal Electric Vehicle Incentive in California.” Renewable Energy World. September 13, 2019. Available at https://www.renewableenergyworld.com/2019/09/13/chicago-startup-will-help-test-hyperlocal-electric-vehicle-incentive-incalifornia/.

When used as a platform for transactive energy, blockchain is a market platform enabler. It provides a technology platform into which a market design and governance structure can be programmed, and through which devices can trade autonomously based on the personal value-maximizing settings chosen by their owners. It can coordinate resources that are increasingly spatially and scale diverse, and token-based payment systems for small DER owners can log complex transactions in real time. Digital network technologies including blockchain can improve energy delivery and reduce costs even without central authorization, and blockchain could enable the trust, transparency, and automation that yields credible and valuable transactive systems.

Implications of Innovation for the Utility Business Model

Digital smart grid, distributed energy, and network technologies have significant implications for the utility business model. How these evolving implications will turn into new utility business models is unknown at the moment; here I offer a conceptual analysis to inform these ongoing discussions.

One important driver of those implications is the extent to which these innovations reduce transaction costs in the electricity supply chain. Transaction costs are the administrative and organizational costs of making a transaction happen: acquiring, assembling, monitoring, organizing, and re-purposing resources. For example, consider the costs to a consumer of buying a cup of coffee in addition to its money price— the time and money cost of travel to the coffee shop, looking at the menu, ordering, and waiting. Now consider the costs to the producer of that cup of coffee—searching for beans and negotiating a contract with the farmer, doing the same for the shop location, employees, and other inputs, and navigating the administrative and regulatory landscape associated with importing beans, opening a retail shop, hiring workers, and selling coffee. Transaction costs abound on both sides of the transaction.

Digital technology has reduced transaction costs to both the buyer and seller of that cup of coffee. Starbucks now has a smartphone app for advance ordering, and digital supply chain technologies have reduced several of the production transaction costs associated with contracting and monitoring. Falling transaction costs mean that Starbucks can rely on contracts with vendors to provide products and services that they otherwise used to do internally.

Falling transaction costs create different organizational structures that are more efficient or suited to these technologies. When the costs of parties entering into contracts and engaging in exchange fall, performing transactions through markets rather than within firms becomes more economical than before. This process is in progress in electricity due to digital and DER technologies.

From their origins in the late 19th century, electric utilities have been vertically integrated, from generation to high-voltage transmission to low-voltage distribution to retail. Vertical integration of these upstream and downstream transactions into the same firm was an economic response to mechanical technologies that had to work together as a system and were built together as a system, as well as a consequence of the cost subadditivity (economies of scale and scope over the relevant range of demand) that characterizes a natural monopoly cost structure.

Vertical integration is a natural response to an environment with higher transaction costs, because vertical integration takes advantage of the managerial hierarchy within a firm to coordinate transactions and decisions that are too expensive to be coordinated through markets and contracts. This argument is grounded in the pioneering research of Ronald Coase, who first argued that firms emerge as decision making responses to market transactions and contracts being costly or difficult to execute.32Coase, Ronald H. “The Nature of the Firm.” Economica 4.16 (1937). 386–405. Building on that insight, Williamson argues that the organizational structure of firms is a consequence of the act of economizing on transaction costs.33Williamson, Oliver. The Economic Institutions of Capitalism. New York: Free Press. 1985. Chapter 4: “Vertical Integration: Theory and Policy.” The desire and ability to decrease transaction costs shapes vertical integration and contracting in a variety of settings, from the production of automobile parts to the decision to build coalfired power plants at coal mine mouths.34See, for example, Klein, Benjamin, Robert G. Crawford, and Armen A. Alchian. “Vertical Integration, Appropriable Rents, and the Competitive Contracting Process.” Journal of Law and Economics 21.2 (1978). 297–326; Joskow, Paul L. “Asset Specificity and the Structure of Vertical Relationships: Empirical Evidence.” Journal of Law, Economics, & Organization 4.1 (1988). 95–117; Bresnahan, Timothy F., and Jonathan D. Levin. Vertical Integration and Market Structure. No. w17889. National Bureau of Economic Research, 2012.

Digital Technologies are Transaction Cost Reducers

Digital technologies reduce the need for vertical integration in electricity due to their distributed and automated monitoring, sensing, and response capabilities. They do so by reducing transaction costs.

When technological change reduces transaction costs, the efficient organizational structures in the industry will also change. When transaction costs rise, a shift to vertical integration enables firms to economize on transaction costs; similarly, when transaction costs fall, the coordination benefits of vertical integration also fall, so the organizational structure should move toward more use of arms-length contracts and markets. In other words, in vertically integrated firms, transactions take place within firms; but when transaction costs fall and lead to less vertical integration, more transactions take place through markets rather than firms. This insight from transaction cost economics has implications for the evolving utility business model.

Falling transaction costs and the ability to automate, arising from digital and DER innovations, suggest two important margins for organizational change: retail markets and distributed production of grid services. The first, retail markets, refers to more local and decentralized markets.35Kiesling, L. Lynne, Michael C. Munger, and Alexander Theisen. “From Airbnb to Solar: Toward A Transaction Cost Model of a Retail Electricity Distribution Platform.” 2019. Available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3229960. Digital technologies around the distribution edge enable consumers, including small consumers and “prosumers,” to participate in market transactions cheaply and conveniently, creating a possibility of increased economic value and reduced environmental emissions.

Recall the use case of Anna, a homeowner with solar and an electric vehicle. While Anna may have invested in these durable assets primarily for their own use, if she has access to a retail market and can participate in it—especially with automation—then she may be able to earn some revenue to help her offset the expense of investing in those assets. Availability of markets creates the opportunity for people like Anna to make more economical investments in technologies that have a smaller environmental footprint.36One significant variable in a consumer’s evaluation of this alternative is the extent to which the price signals they receive reflect accurately the environmental costs associated with different energy choices. This complicated question involves both regulatory policy (e.g., whether or not the energy price reflects a carbon tax or another form of greenhouse gas regulation) and the extent to which consumers choose to act on their environmental preferences even in the absence of such policies. Such markets interconnect owners of distributed resources and enable them to transact with each other, using prices to coordinate their consumption and production decisions and to inform their investment decisions.

Markets for Grid Services

A second and more sophisticated way that the distribution grid can enable DERs to create value for their owners, for others, and for the system itself, is for distributed resources to provide grid services, as discussed previously. Aspects of grid services include frequency regulation, fast frequency response, voltage regulation, and other services that contribute to a balanced, reliable, resilient grid.

The regulated monopoly model supported vertically integrated provision of delivery and grid services at a time when the entire supply chain had the cost subadditivity of a natural monopoly.37Cost subadditivity is the technical requirement for a market to be a natural monopoly. Subadditivity requires both economies of scale (declining long-run average cost over the relevant range of demand) and economies of scope (using a set of assets to produce two products reduces costs compared to stand-alone production, or C(x+y) < C(x) + C(y)). Innovation has reduced that natural monopoly footprint to the transmission and distribution wires portion of the supply chain. However, regulation-embedded vertical integration limits the ability to take advantage of transaction cost reductions.

Distributed resources to provide grid services also create an opportunity for decentralized markets to coordinate those resources. In the example above, suppose the local area of the grid in Anna’s neighborhood is congested and close to imbalance. If Anna (and her neighbors) who own DERs participate in a decentralized local energy market, the energy from her solar PV or her EV battery could provide voltage regulation, frequency regulation, or other grid services to coordinate flow and eliminate the imbalance. If the market is in a transactive system she can program in the price she is willing to accept to sell energy into her home energy management system, and if the market price exceeds her trigger price, her sale of energy is automated and the grid is coordinated within the market period.

Having decentralized markets with prices that reflect local conditions (such as congestion) impart valuable information to owners of grid services and owners of distributed resources, but only if markets exist that enable those prices to form and be communicated in the first place. Thus, transaction cost reducing digital technologies make decentralized markets for grid services possible.38As discussed earlier, such decentralized markets will be feasible in the future, and transactive energy systems will enable the distribution system to evolve into such decentralized markets. Because TE enables locational dynamic pricing to evolve independently at the bulk power level and the distribution system level (and at different levels within the distribution system), TE provides an incremental process for developing decentralized energy markets.

Business Model: A Grid Services Coordinating Platform

My comments here lay out a conceptual framework for thinking about these questions rather than a specific, detailed institutional design. This conceptual framework is also complicated by the variety of regulatory models in the different states and their implications for utility business models. 15 states and the District of Columbia have restructured their regulatory institutions to unbundle generation from the regulated utility and to allow retail competition, and the utility business model in those states differs significantly from the conventional vertically integrated monopoly. Evolving toward a platform model and decentralized markets is more compatible with such restructured business models.

Grid modernization and DERs create the opportunity for a platform business model. A platform firm acts as an intermediary connecting two or more agents for mutual benefit.39Parker, Geoffrey G., Marshall W. Van Alstyne, and Sangeet Paul Choudary. Platform Revolution: How Networked Markets Are Transforming the Economy and How to Make Them Work for You. W.W. Norton & Company. 2016. See also Evans, David, and Richard Schmalensee. Matchmakers: The New Economics of Multisided Platforms. Harvard Business Review Press. 2016. Consider the analogy to financial market exchanges, such as stock exchanges or futures exchanges, which provide trading platforms. By being attentive to the interests of both buyers and sellers, they define standard products and rules by which exchanges will occur, and provide timely information and a way for buyers to bid and sellers to offer, opening or closing new markets as the interests of buyers and sellers wax and wane.

Importantly, this value proposition is precisely the same as that seen in other platform companies. Ride sharing platforms (like Uber, Lyft, and Sidecar) give vehicle owners an opportunity to monetize an underutilized asset they own—seat space in their cars—while giving others an opportunity to get rides. Ride sharing platforms change the vehicle purchase calculus, at the margin affecting the decision of when to buy a new car, how nice a new car to buy, and how many hours to spend on the platform and available to give rides. Similarly, by connecting people with rooms to rent to people who want rooms, Airbnb provides a platform that enables property owners to profit from renting out the excess capacity in their homes.

A core function of a distribution platform will continue to be providing and operating the distribution wires network. How that function will evolve, the specific functions that different entities will perform, and the regulatory treatment of those functions are all topics of current debate.

These essential operational functions that would be performed by the distribution system operator (DSO) include

- System planning over multiple timeframes to inform distribution grid investment decisions;

- Timely and transparent interconnection of consumers, producers, and DER owners on the distribution grid;

- Real-time operation of the distribution grid;

- and Coordination with distributed market platforms for energy and grid services.40Kristov, Lorenzo. “Regulatory and Market Architecture for the Integrated Decentralized Electric Grid.” Presentation, Transactive Energy Systems Conference. 2019.

By performing those functions as a DSO and coordinating the need for and provision of grid services, the new utility business model would be a grid services coordinating platform.

The distribution platform firm has the operational and regulatory requirement to deliver electricity services to end users. Accompanying that role are a reliability requirement, with some administrative definition of what constitutes reliability, and the physical real-time network balancing function. The distribution platform is the orchestrator of grid needs, i.e., reliability, frequency regulation, voltage regulation, and capacity. The distribution platform earns a normal rate of return and the revenue to maintain and modernize infrastructure through a wires charge to retail customers. For these DSO functions and grid services provision and coordination, the distribution platform would earn a service fee.

This definition of the primary roles of a DSO-grid services coordinating platform may appear straightforward, but the scope of distribution platform that would enable it to fulfill these roles is likely to involve the distribution platform itself as a market participant in roles that could have anticompetitive effects. For example, given the load serving entity requirement, should the distribution platform engage in energy market transactions for backup energy generation to enable it to fulfill that role in the cases where decentralized contracts do not give it confidence, or in other extenuating circumstances? To maintain system balance in the presence of diverse and intermittent energy sources like wind and solar, should the distribution platform own and control “behind the meter” residential solar? In both of these cases the presence of a large, regulated incumbent buyer or seller with market power could lead to anticompetitive vertical foreclosure.41Kiesling, L. Lynne. “Incumbent Vertical Market Power, Experimentation, and Institutional Design in the Deregulating Electricity Industry.” Independent Review 19.2 (2014). 239–264. Similarly, having the incumbent regulated monopoly provide a curated “marketplace” for customer devices could exert anticompetitive market power in a function that could be competitive.

Unlike a traditional wires-only business model, a platform model emphasizes the role of the firm as an intermediary facilitating the interactions of agents in the network. A platform model does imply some technological differences in the distribution network compared to the traditional distribution grid architecture. The existing architecture of the distribution grid is designed for one-way current flow, from generator to end user. In a technological context with few large-scale generators and many users, one-way flow was a cost-effective architecture choice. Smart grid and distributed resource technologies have the potential to enable smaller-scale generation and distribution throughout the network, and to enable small-scale transactions between distributed agents, which would require a network capable of two-way current flow.

One example of a design for a DSO-grid services coordinating platform is the layered architecture proposed by Lorenzo Kristov—a wires-only open-access DSO, providing system planning, interconnection, real-time operation, and markets.42Kristov, Lorenzo. “Regulatory and Market Architecture for the Integrated Decentralized Electric Grid.” Presentation, Transactive Energy Systems Conference. 2019. Kristov’s proposal includes the following features of such a platform:

- Open, participatory distribution planning process that includes 3rd parties with DER-based nonwires services

- Defined grid services that DER owners and aggregators can provide and be paid for; procure services through transparent market mechanisms

- Streamlined interconnection for local microgrids and community energy projects

- Transparent procedures to coordinate transmission-distribution interface and curtail DER when needed for real-time reliability

- DSO collaboration with local governments on decarbonization and resilience projects

- Data access framework that protects privacy and security while enabling all of the above

- Limited DSO roles and assets based on “natural monopoly” (poles and wires, system operation); fenced-off competitive activities (retail kWh, DER ownership); privatized technology risks

Regulatory Frameworks for a Decentralized, Digital Energy Future

Economic regulation has shaped the electricity industry for over a century. In the US both federal (for transmission and wholesale market operations) and state (for distribution systems) agencies regulate the actions of industry participants. Such regulation takes the form of rate-of-return (ROR) regulation, allowing the vertically integrated monopoly to earn a market-benchmarked rate of return on its capital assets. Regulators must approve the allowed rate of return and which capital assets can earn that return, known as the rate base. In return for these regulatory limitations on their revenue model, utilities receive a legal entry barrier that grants them a monopoly on all of the firm’s activities in a specific territory.43Viscusi, Kip, Joseph Harrington, and David Sappington. Economics of Regulation and Antitrust. MIT Press. 1983. Chapters 11, 12.

Such regulation has tradeoffs. ROR regulation gives regulated utilities incentives to invest in more capital than otherwise necessary, and asymmetric information between regulators and the regulated firm can lead to above-normal profits for utilities.44Laffont, Jean-Jacques, and Jean Tirole. A Theory of Incentives in Procurement and Regulation. MIT Press. 1993. See also Viscusi, Kip, Joseph Harrington, and David Sappington. Economics of Regulation and Antitrust. MIT Press. 1983. Chapter 13. The emphasis on cost recovery for providing a specific standard set of services also prevents value creation through diversity and product differentiation. But with a relatively stable set of technologies through the 1960s, this regulatory model fulfilled the 20th century’s policy objectives of safe, reliable, and affordable standard electric service.45Hirsh, Richard. Power Loss: The Origins of Deregulation and Restructuring in the American Electric Utility System. MIT Press. 1999.

The changing technology landscape creates pressure for this traditional regulatory model in much the same way that it strains the utility business model by reducing the economic justification for vertical integration. Regulations designed in the early 20th century and codified mid-century,46Bonbright, James C., Albert L. Danielsen, and David R. Kamerschen. Principles of Public Utility Rates. Columbia University Press. 1961. with large electro-mechanical technologies and the vertically integrated regulated monopoly business model, are increasingly outdated. Add to that the increasing emphasis on environmental policy objectives—air quality regulations since 1970 and more recent regulations focused on greenhouse gas emissions—and the mismatch between traditional regulation and potential values in the 21st century becomes even more apparent.

Regulatory Frameworks for a Decentralized, Digital Energy Future

Increasingly over the past 40 years state and federal governments have implemented environmental regulations that affect electric utility operations and investment decisions. Most existing regulatory policies have been introduced by state and federal governments with the goal of reducing carbon emissions and subsidizing the growth of select renewable technologies, such as solar. However, there is sometimes a conflict between pursuing the most cost-efficient carbon reductions and encouraging the growth of particular technologies. If, for example, the government subsidizes solar power through tax credits, it encourages the development of solar technology perhaps at the expense of other renewable or energy efficiency technologies.

On the federal level, there is a solar investment tax credit (ITC), which is currently a 26% tax credit for installation of residential solar, that will be phased out in 2022. On the state level, the most powerful renewable energy policies are renewable portfolio standards (RPS), which have been adopted by 29 states. Renewable portfolio standards most often have specific percentage targets for renewable electricity generation by utilities, but it is becoming increasingly common to have “carve-outs” for specific technologies, including distributed generation. For example, Colorado has a target of 30% renewables by 2020 for its investor-owned utilities, 3% of which must come from distributed generation.47DSIRE database, North Carolina Clean Energy Technology Center. Available at https://programs.dsireusa.org/system/program/detail/133.

Although the integration of specific incentives for distributed generation is one aspect of a possible regulatory framework, the true advantage of a market-based distributed electricity system is just that: its reliance on the market. If it is cost-effective for consumers to adopt rooftop solar once the grid enables them to sell and buy electricity from it, adoption will increase. Production or investment subsidies, as well as mandates such as those that exist in current RPS policies, distort market signals by subsidizing certain technologies.48To the extent that such subsidies are substitutes for more transparent carbon pricing, they do communicate information about the environmental costs of different energy technologies, but they are an indirect and opaque policy choice that is prone to political manipulation. Moving away from such subsidies and technology mandates and adopting more transparent carbon pricing policies would amplify the benefits of transactive systems and decentralized energy markets.

Existing regulations stifle some changes and subsidize others, leading to cross-subsidization and a landscape that is not technology neutral for entrepreneurs to develop and commercialize clean energy technologies.49L. Lynne Kiesling. “Alternatives to Net Metering: A Pathway to Decentralized Electricity Markets.” R Street Institute Policy Study 52. 2016. 4. Cross subsidies obscure transparent price signals when utilities charge lower prices to customers that are more expensive to serve and higher prices to others. One example of technology-specific regulations that embed such cross-subsidization is net energy metering (NEM). NEM regulations allow residential customers with DERs to sell excess energy back to the utility.50Smith, Josh, Grant Patty, and Katie Colton. “Net Metering in the States: A Primer on Reforms to Avoid Regressive Effects and Encourage Competition.” Center for Growth and Opportunity Policy Paper 2018.001. August 2018. 6; L. Lynne Kiesling. “Alternatives to Net Metering: A Pathway to Decentralized Electricity Markets.” R Street Institute Policy Study 52. 2016. 2. In several states the customer is paid a price at or above the regulated retail rate, which means that NEM customers are using the distribution system without paying to use it.51Smith, Josh, Grant Patty, and Katie Colton. “Net Metering in the States: A Primer on Reforms to Avoid Regressive Effects and Encourage Competition.” Center for Growth and Opportunity Policy Paper 2018.001. August 2018. 7; L. Lynne Kiesling. “Alternatives to Net Metering: A Pathway to Decentralized Electricity Markets.” R Street Institute Policy Study 52. 2016. 7; MIT Energy Initiative. Utility of the Future. 2015. 15; Eid, Cherrelle, Javier Reneses, Pablo Frías Marín, and Rudi Hakvoort. “The Economic Effect of Electricity Net-Metering with Solar PV: Consequences for Network Cost Recovery, Cross Subsidies and Policy Objectives.” Energy Policy 75 (2014). 244–254; Picciariello, Angela, Claudio Vergara, Javier Reneses, Pablo Frías, and Lennart Söder. “Electricity Distribution Tariffs and Distributed Generation: Quantifying Cross-Subsidies from Consumers to Prosumers.” Utilities Policy 37 (2015). 23–33; Brown, David P., and David E.M. Sappington. “Designing Compensation for Distributed Solar Generation: Is Net Metering Ever Optimal?” Energy Journal 38.3 (2017); Sergici, Sanem, Yingxia Yang, Maria Castaner, and Ahmad Faruqui. “Quantifying Net Energy Metering Subsidies.” Electricity Journal 32.8 (2019). 106632. This pricing structure, a relic of a time when analog meters would spin backward to account for excess generation, incorporates regressive cross-subsidies into electricity pricing.52Smith, Josh, Grant Patty, and Katie Colton. “Net Metering in the States: A Primer on Reforms to Avoid Regressive Effects and Encourage Competition.” Center for Growth and Opportunity Policy Paper 2018.001. August 2018. 8. As DER shares increase, these obsolete NEM regulations introduce costly and inefficient tensions in the distribution system, and should be replaced by digital, decentralized markets that use automation to connect DER owners with ease and convenience.

Renewable portfolio standards (RPSs) also affect DERs. An RPS either suggests or mandates that some percentage of the electricity that utilities sell is generated using renewable sources by a specified target date.53Smith, Josh, and Vidalia Cornwall. “What is the Relationship Between Renewable Portfolio Standards and Electricity Prices?” Center for Growth and Opportunity Research in Focus 2019.001. February 2019. 1. RPS policies focus on specific qualifying renewable technologies (typically wind and solar) rather than technologies that yield the specific policy outcome—reduced greenhouse gas emissions. By excluding hydroelectric, nuclear, and other low-carbon sources, RPS regulations are not technology neutral and have led to higher electricity prices in states with RPS mandates.54Smith, Josh, and Vidalia Cornwall. “What is the Relationship Between Renewable Portfolio Standards and Electricity Prices?” Center for Growth and Opportunity Research in Focus 2019.001. February 2019. 1. Some states are changing their RPS regulations to clean energy standards to enable those low-carbon technologies to compete equivalently with wind and solar under these regulations.

Regulation to Enable DER Interconnection and Platform Business Models

Traditional regulation’s focus on cost-based rate setting complemented and reinforced the more homogeneous technologies of the 20th century. Its focus also complemented and reinforced the homogeneous and distinct roles of generators as producers and customers as consumers. Today’s distribution grid and the people in the network are more technologically and economically diverse, and are increasingly more heterogeneous in scale and location. Taking advantage of this diversity to enable economic and environmental benefit will require not only changes to the utility business model, but also in regulatory frameworks. The transaction cost economics analysis above suggests four regulatory changes to facilitate DERs and evolution toward platform business models for utilities:

- A regulatory mission of consumer protection that de-emphasizes cost-based rate-setting

- Matching the regulatory jurisdiction over the utility to the parts of the supply chain that still possess natural monopoly cost structures

- Distributed markets to enable DER owners to profit from their resources as an alternative to net energy metering

- Outcome-focused performance-based regulation

The shift toward DER integration and interconnection suggest that the regulatory mission should evolve to consumer protection and away from cost-based rate setting. This regulatory approach is customer-centered, focusing on ease of use and the value to consumers of being able to consume and produce energy and grid services to meet their other life goals. The tools of a consumer-protection-focused regulatory approach include the following:

- Information provision as inputs to consumer choices

- Transparency and disclosure requirements for market participants

- Network open access interconnection and interoperability requirements

- Market participation

Consumer protection using these mechanisms mirrors the regulatory approach of the Federal Trade Commission, which can provide useful lessons and parallels.55https://www.ftc.gov/policy.

From a structural perspective, a change in the regulatory footprint to quarantine the monopoly is the best feasible approach for enabling the benefits of DER interconnection and digital innovation to emerge. Confining the regulated monopoly footprint to natural monopoly functions, such as interconnection, system operations, transmission and distribution wires, and delivery, would reduce entry barriers in competitive or potentially competitive markets such as behind-the-meter solar and EV charging.

This “quarantine the monopoly” concept arises from the work of William Baxter, who in his position as Assistant Attorney General in the US Department of Justice in the 1980s was the primary architect of the settlement of the US vs. AT&T case that led to AT&T’s divestiture in 1982. One of Baxter’s principal concerns regarding the welfare effects of the AT&T monopoly was what came to be known as Baxter’s Law, or the Bell Doctrine: “regulated monopolies have the incentive and opportunity to monopolize related markets in which their monopolized service is an input.”56Joskow, Paul, and Roger Noll. “The Bell Doctrine: Applications in Telecommunications, Electricity, and Other Network Industries.” Stanford Law Review 51 (1998). 1249.

If there is sufficient rivalry or potential rivalry in a related market, then allowing monopolist participation in that market could reduce or stifle competition, enabling the monopolist to extend its monopoly into the related market. One result of extending that vertical monopoly into a related market would be reduced output, higher prices, and deadweight loss arising in that related market. Baxter’s argument was that the best feasible approach to such a situation, in which a regulated monopolist sits in the middle of a vertical supply chain with competitive or potentially competitive markets on either or both sides, is to quarantine the monopoly by restricting its market participation to its regulated functions. The best way to do this is to separate the ownership and control of the regulated functions from the other vertically related functions.57Kiesling, L. Lynne. “Incumbent Vertical Market Power, Experimentation, and Institutional Design in the Deregulating Electricity Industry.” Independent Review 19.2 (2014). 239–264. See also Kiesling, L. Lynne. “A Prosperous and Cleaner Future: Markets, Innovation, and Electricity Distribution in the 21st Century.” Conservation Leadership Council. (2015).

However, this approach involves regulatory restructuring, which may not be likely in states that retain the vertically integrated utility structure and traditional regulatory model. In those states, the next best alternative is to match the utility’s revenue to its degree of performance on specific outcomes. For example, such performance-based regulation would provide additional return on equity basis points if the length of time it takes to interconnect DERs is below a certain threshold. Sadly, this limited vision would still fall far short of enabling the value potential that digital and DER technologies create.

A third policy for sustainable DER interconnection and growth is to move away from administrative regulations like NEM that subsidize DER adoption and toward distributed transactive markets to enable DER owners to earn revenue from the excess capacity in their DER assets (which would itself induce increased investment in DER assets), streamlined interconnection contracts, etc.58Kiesling, L. Lynne, Michael C. Munger, and Alexander Theisen. “From Airbnb to Solar: Toward A Transaction Cost Model of a Retail Electricity Distribution Platform.” 2019. Available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3229960. The decentralized markets described above take advantage of the reduced transaction costs arising from digital technologies, and can create a transactive system in which DER owners can participate easily and conveniently using automation to enable their DERs to respond to price signals. Markets and a transactive energy system would also make DERs more effective by encouraging economic value creation rather than encouraging total production, as NEM does.

A final policy recommendation is the move away from cost-based rate-setting and toward performance-based rates (PBR) for the remaining monopoly functions, not as technology-focused or program-focused inducements, but tied to actual, substantive, desirable outcomes.59Lazar, Jim, and Wilson Gonzalez. Smart Rate Design for a Smart Future. Regulatory Assistance Project. July 2015. Lazar and Gonzalez discuss rate design within a vertically integrated framework, though, while the analysis in this paper focuses on a future scenario with decentralized local energy markets and grid services markets. In that scenario the regulatory footprint to which rate design is relevant would be delivery, grid services provision, and grid services coordination functions of a DSO. The example above of DER interconnection time performance illustrates outcome-based PBR. In a DSO-grid services coordinating platform context, their revenue can be a consequence of their performance on the DSO functions and how well they deliver on the other dimensions of the institutional design. This PBR structure can form the process of determining the time-varying, volumetric service fee for the DSO and grid service coordination functions.

These four recommendations combine to form a regulatory framework conducive to innovation in clean energy technologies and increased DER participation in the energy system. It also prioritizes consumer values, choice, and control by enabling those who want to become prosumers to do so through decentralized markets that align individual incentives with system benefits.

Conclusion

Technological change is transforming our daily lives, and its transformation of the electricity industry and the distribution grid is in progress. Digital and DER technologies create new and diverse ways to generate economic and environmental value, and do so in large part by reducing transaction costs. The features of digital and distributed energy technologies described above indicate the extent to which these technologies are transaction cost reducers, in the electricity industry as well as throughout the entire economy. The powerful transaction-cost-reducing features of digital technologies reduce the impetus for vertical integration of distribution and retail as the economically appropriate organization of the electricity industry.

Technological change is transforming our daily lives, and its transformation of the electricity industry and the distribution grid is in progress. Digital and DER technologies create new and diverse ways to generate economic and environmental value, and do so in large part by reducing transaction costs. The features of digital and distributed energy technologies described above indicate the extent to which these technologies are transaction cost reducers, in the electricity industry as well as throughout the entire economy. The powerful transaction-cost-reducing features of digital technologies reduce the impetus for vertical integration of distribution and retail as the economically appropriate organization of the electricity industry.

Falling transaction costs make coordination through markets rather than within firms more beneficial than before, and DERs will mean that more people have more and different valuable resource capabilities that they can exchange. Decentralized economic coordination through markets informs the process of decentralized physical coordination by providing a way for people to communicate their preferences to each other. Digital automation reduces the costs of such communication and coordination.

Distributed resources can disrupt the grid’s balance and make centralized control more difficult. They can also, though, provide some of these grid services for rebalancing in a more localized setting. In a more distributed grid architecture, disturbances and imbalances can be counteracted using flexible resources located closer to the disturbance. Thus, distributed resources can become valuable suppliers of grid services to counteract some of the imbalances the DERs can introduce.