Introduction

In December of 2019, New Jersey joined thirteen other states and the District of Columbia in offering driver’s licenses to unauthorized immigrants (NYT 2019a). Proponents of Unauthorized Immigrant License Policies (UILPs), such as the administrator of New Jersey’s Motor Vehicle Commission, argue that unauthorized immigrants are already driving and that their inability to acquire a license prohibits them from purchasing car insurance (NYT 2019b; UTO 2019). In contrast, opponents argue that UILPs will increase the number of uninsured drivers on the road. While arguing against Oregon’s failed UILP, then state Representative Kim Thatcher stated that she was “concerned the new driver’s cards [would] not positively impact the number of insured drivers on the road” (Protect Oregon DL 2014).

Despite receiving considerable media attention (NYT 2016; Washington Post 2019; NBC 2019), little is known about the relationship between UILPs, auto insurance coverage, and traffic outcomes. To the best of our knowledge, there are only two other papers on the subject. In the first, Lueders, Hainmueller, and Lawrence (2017) show that California’s UILP (AB 60) was not associated with increases in the number of traffic accidents. They do however uncover a change in accident composition; more intensely-treated counties experienced a reduction in the number of hit-and-run accidents. Meanwhile Cáceres and Jameson (2015) document a positive association between policies restricting unauthorized immigrants’ access to driver’s licenses and auto insurance costs, though the relationship is weaker in areas with more unauthorized immigrants.

While both of these studies are well-executed, we make several notable contributions. As the first paper to examine how UILPs affect insurance outcomes in a multi-state setting, we leverage substantially more policy variation than was available to previous authors. In addition, we examine a rich set of insurance-related outcomes, including auto insurance coverage, claims, and the severity of these claims for multiple types of auto insurance (liability-bodily injury, liability-property damage, collision, comprehensive, and uninsured/underinsured motorist). We show that UILPs are associated with a 1 percent increase in auto insurance coverage, suggesting that newly-licensed unauthorized immigrants do opt to purchase insurance. However, we also document increases in insurance claims, which are most pronounced in No Fault insurance states where it is easier to file a claim. Similarly, we provide evidence that California’s UILP was associated with an increase in the number of collisions, but we do not identify any relationship between UILPs and the severity of insurance claims or fatalities.

Legislative Background and Existing Literature

The United States is one of the most car-dependent countries in the world (World Bank 2013), and obtaining a driver’s license is linked to both economic and personal freedom (Raphael and Rice 2002). Yet despite comprising nearly 5 percent of the US labor force, the majority of the nation’s 11 million unauthorized immigrants cannot legally drive (Passel and Cohn 2018). We begin by discussing major pieces of legislation over the last decade which have expanded unauthorized immigrants’ access to driver’s licenses. We then summarize existing work on these policy changes.

Legislative Background

Driver’s licenses are issued by state department of motor vehicles. While a driver’s license grants the holder driving privileges throughout the country, each state is free to set its own requirements. Because these licenses often also serve as identification (Egelman and Cranor 2005)—including for boarding commercial aircraft—Congress established minimum federal identification standards in response to the Septem- ber 11th terrorist attacks (Lopez 2004; Kanstroom 2006; Lin 2009).

The REAL ID Act of 2005 requires states to obtain and verify driver’s license applicants’ birthdates, photos, and Social Security numbers (Public Law 109-13 Title II Sec 201 (3)).1The Intelligence Reform Act of 2004 also established a set of standards. It was superseded by the REAL ID Act, which granted more expansive powers to the federal government. However, states retain the ability to issue clearly distinguishable “not for federal ID” driver’s licenses to unauthorized immigrants (Amuedo-Dorantes, Arenas-Arroyo, and Sevilla 2018). Nearly a decade after the passage of the REAL ID Act, a flurry of legislative activity expanded driving privileges to nearly half of all unauthorized immigrants. Between 2013 and 2015, ten states and the District of Columbia passed laws permitting these individuals to obtain licenses.

Unauthorized Immigrants and Traffic Outcomes

In studying how UILPs affect traffic outcomes, our study is most comparable to Lueders, Hainmueller, and Lawrence (2017). These authors examined the relationship between California’s UILP (AB 60) and the number of traffic accidents within the state between 2006 and 2015 (AB 60’s implementation year), exploiting the fact that treatment was felt more intensely in counties issuing the most AB 60 licenses as a share of the total number of licenses in the county. Though California does not report the number of AB 60 licenses issued at the county level, the authors approximate this value as the difference between the number of licenses actually issued and the number of licenses predicted to be issued after fitting county-specific linear time trends to the 2011–2014 license data. Lueders, Hainmueller, and Lawrence (2017) did not identify a change in the total number of accidents, though they do identify a change in accident composition. Specifically, the authors found a negative association between AB 60 exposure and the number of hit-and-run accidents, which they attributed to AB 60 reducing unauthorized immigrants’ risk of citation, arrest, and possible deportation when interacting with law enforcement.

The Institute for Social Research (2018) also exploited the fact that AB 60 was likely felt more intensely in counties with the most unauthorized immigrants. In contrast to Lueders, Hainmueller, and Lawrence (2017), the Institute for Social Research (2018) did not find any relationship between AB 60 licenses and hit-and-run collisions when they measured exposure using the share of the county comprised of unauthorized immigrants. The authors speculated that while gaining a license may have initially increased unauthorized immigrants’ willingness to interact with law enforcement officials, this effect was offset by the 2016 presidential election and the Trump administration’s immigration priorities. Finally, the Institute for Social Research (2018) suggested that AB 60 may have helped slow the growth in California’s rate of uninsured drivers.

Our paper also complements work by Cáceres and Jameson (2015) who examined the relationship between policies restricting unauthorized immigrants’ access to driver’s licenses and the cost of car insurance. Examining a subset of 41 states over a 14-year period, the authors found that restrictions on driving privileges increased the cost of car insurance, though this increase was smaller in areas with more unauthorized immigrants. The authors suggested that this pattern could be explained by auto insurance inducing unauthorized immigrants to drive less carefully. It is worth noting that the effect of increasing access to driver’s licenses may not be symmetric to these restrictive policies. After the implementation of a restrictive law, the only unauthorized immigrants on the road will be those willing to accept the risk of being unlicensed and uninsured. While UILPs will make it easier for these individuals to obtain auto insurance, they may also change the composition of drivers by inducing more unauthorized immigrants onto the road.

Driver’s Licenses and Unauthorized Immigrants

This paper contributes to an emerging understanding of the consequences of UILPs, which thus far has primarily focused on labor market outcomes. Amuedo-Dorantes, Arenas-Arroyo, and Sevilla (2020) examined the relationship between UILPs and employment for a sample of likely-unauthorized immigrants While they did not identify any change in the probability that a likely-unauthorized immigrant is employed, they did document adjustments at the intensive margin for subsets of likely-unauthorized workers. Specifically, the authors found a 1.6 percent increase in weekly hours worked for likely-unauthorized men. Amuedo-Dorantes, Arenas-Arroyo, and Sevilla (2020) also found evidence that UILPs increase average commuting times for men who reported driving to work, though they did not identify changes in the probability that likely-unauthorized immigrants report driving to work. In contrast, a working paper by Cho (2019) documented a positive relationship between the implementation of a UILP and the probability that a likely-unauthorized immigrant has access to a car and reports taking a private vehicle to work. Cho also identified a 1 percentage point increase in the probability that a likely-unauthorized is employed, an effect which was most pronounced in low-accessibility areas and for those employed in car-dependent occupations.

Insurance and Moral Hazard

Our research also contributes to a well-established economics literature on moral hazard and insurance, though we do not purport to summarize this extensive body of work. Economists have long recognized that insurance may alter behavior (Arrow 1963; Pauly 1968), though it has been difficult to disentangle this phenomenon from the possibility that higher risk individuals may be more likely to select into insurance.

Chiappori and Salanie (2000) did not find evidence of moral hazard in a cross-section of data on French drivers, while Dionne, Michaud, and Dahchour (2013) did find evidence when using panel data, although the effect is limited to those with less than 15 years of experience. Weisburd (2015) estimated moral hazard by examining accidents for employees of a large Israeli company where those covered by a collective bargaining agreement received free auto insurance. She found that a $100 discount in accident costs increased the likelihood of being in an accident by approximately 10 percent.

Schneider (2010) also found evidence of moral hazard for drivers when he compared the outcomes of New York City taxicab drivers who are long-term lessees and owner-operators. To address the possibility that riskier drivers selected into leasing, he first controlled for a rich set of driver and vehicle characteristics. He also instrumented for leasing status with community norms about taxi ownership and examined the outcomes for a subset of drivers who switched from leasing to owning. Overall, he estimated that 16 percent of all lessees’ accident could be attributed to moral hazard.

Finally, auto insurance can also influence the decision to file an insurance claim (and the amount of the claim). On one hand, large deductibles discourage the insured from reporting small accidents (Chiappori and Salanie 2014), and policies reducing the costs of filing are likely to increase the number of claims.

For instance, states with No Fault auto insurance—whereby the insurer pays the policy holders’ medical bills regardless of who was at fault—has been liked to greater insurance costs (Landes 1982; Cummins, Phillips, and Weiss 2001; Cohen and Dehejia 2004; RAND 2010). At the same time, auto insurance may generate ex post moral hazard, whereby claimants are able to file false claims or exaggerate the value of legitimate claims. Looking at auto insurance, Cummins and Tennyson (1996) found a positive relationship between permissive attitudes toward dishonest and fraudulent behavior and bodily injury liability claims.

Data, Measures, and Methods

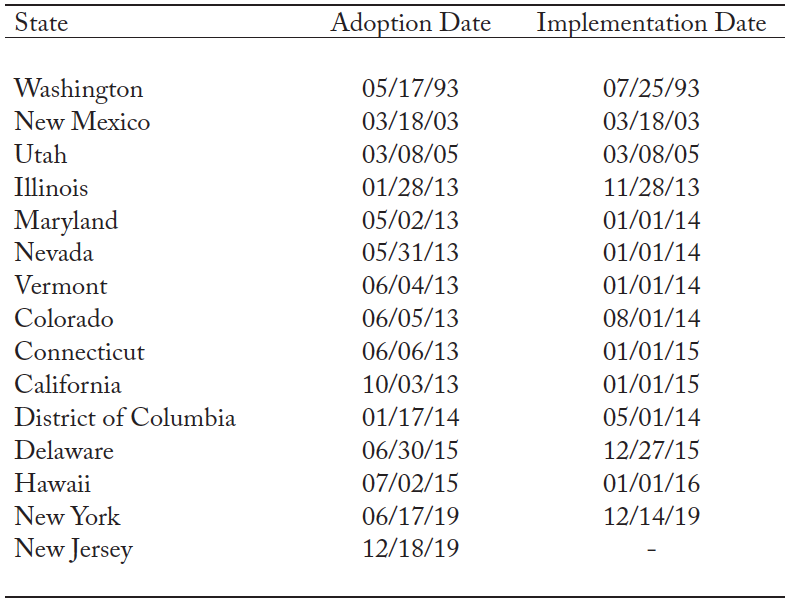

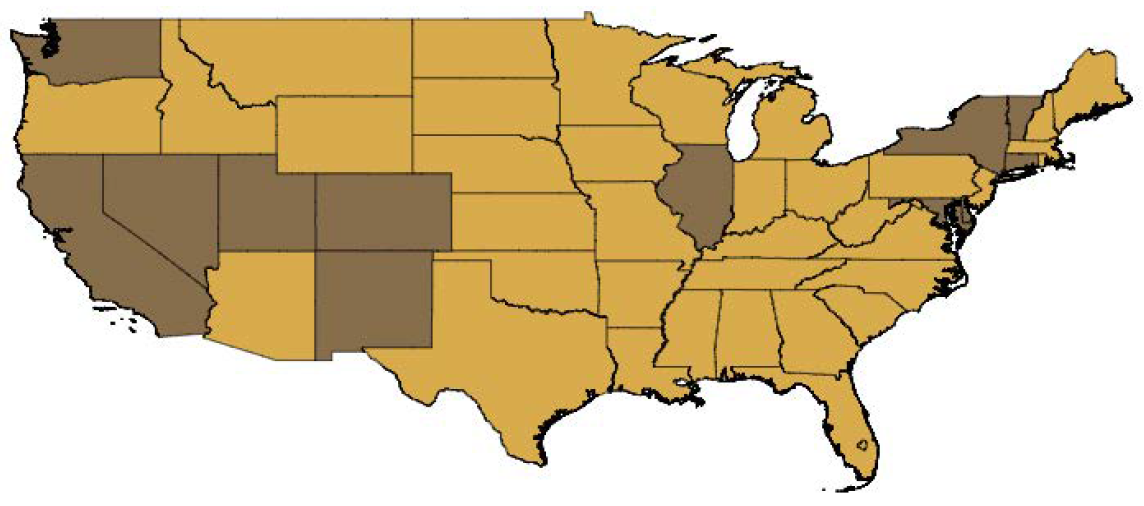

We obtain information on state laws offering driving privileges to unauthorized immigrants from the National Conference of State Legislatures (NCSL 2019), while adoption and implementation dates are obtained from each piece of legislation. Figure 1 depicts the states having passed a UILP as of 2019, and the exact dates are listed in Table 1.2Though not depicted, Hawaii also allows unauthorized immigrants access to a driver’s license. Oregon SB 833, passed in 2013, sought to permit unauthorized immigrants to obtain a license, but was ultimately overturned by Ballot Measure 88. Since this paper utilizes implementation dates, Oregon is never a treatment state. While New Jersey passed its UILP in 2019, it does not yet have an implementation date. These states vary considerably in terms of the size of their likely-un- authorized immigrant populations. For instance, they include both the state with the largest number of likely-unauthorized immigrants (California) and the state with the smallest number (Vermont). Both of those states offer driver’s licenses to unauthorized individuals. Of the 10 states with the most likely-unauthorized immigrants, 3 have adopted a UILP.3Using the American Community Survey, the top 10 states are California, Texas, New York, Florida, Illinois, New Jersey, Georgia, North Carolina, Washington, and Virginia.

Travel Behaviors: Highway Statistics and American Community Survey

We first use the 2008–2017 Federal Highway Administration’s Highway Statistics series to explore whether the implementation of a UILP increases the number of licensed drivers with the following event- study framework:

(1)

where  is an indicator for being

is an indicator for being  periods away from the implementation of a

periods away from the implementation of a  ,

,  and

and  are indicators capturing observations outside the balanced event-study window,

are indicators capturing observations outside the balanced event-study window,  is a vector of time-invariant state fixed effects,

is a vector of time-invariant state fixed effects,  is a vector of state-invariant year fixed effects, and standard errors are clustered at the state level (Bertrand et al. 2004).4 Because the first switch from untreated to treated occurs in 2013, our balanced event-study window can have at most 6 pre-periods. Similarly, the final switch occurs in 2016, so we can have at most 1 post-period. We are unable to estimate pre-implementation coefficients for WA, NM, and UT, so we exclude them from the analysis in order to assure that our results are not driven by a change in the sample composition at j=0. However, our results are robust to including these states. We also opt not to include state-specific linear time trends in this specification because the estimates do not indicate a noticeable pre-trend.

is a vector of state-invariant year fixed effects, and standard errors are clustered at the state level (Bertrand et al. 2004).4 Because the first switch from untreated to treated occurs in 2013, our balanced event-study window can have at most 6 pre-periods. Similarly, the final switch occurs in 2016, so we can have at most 1 post-period. We are unable to estimate pre-implementation coefficients for WA, NM, and UT, so we exclude them from the analysis in order to assure that our results are not driven by a change in the sample composition at j=0. However, our results are robust to including these states. We also opt not to include state-specific linear time trends in this specification because the estimates do not indicate a noticeable pre-trend.

We next use the 2008–2017 American Community Survey (ACS) to test whether UILPs induce more unauthorized immigrants onto the road as opposed to enabling those who were already driving to obtain licenses (Ruggles et al. 2019). Because the ACS does not directly ask about authorization status, we use a residual imputation method proposed by Borjas and Cassidy (2019). Specifically, we use characteristics indicative of legal status to identify likely-authorized immigrants; all remaining foreign-born individuals are considered likely-unauthorized.5A foreign-born person is classified as likely-authorized if that person (a) arrived before 1980; (b) is a citizen; (c) receives Social Security benefits, SSI, Medicaid, Medicare, or Military Insurance; (d) is a veteran or is currently in the Armed Forces; (e) works in the government sector; (f ) resides in public housing, receives rental subsidies, or is the spouse of someone who resides in public housing or receives rental subsidies; (g) was born in Cuba; (h) has an occupation requiring some form of licensing; or (i) has a legal immigrant or citizen spouse. All remaining foreign-born persons are classified as likely-unauthorized. The code for this imputation, as well as the imputation for the ACS, is graciously provided by Borjas (2017) and Borjas and Cassidy (2019) on Borjas’s personal website (https://sites.hks.harvard.edu/fs/gborjas/#section3). We restrict attention to 18–54-year-old individuals in order to match the group examined by Cho (2019). Using this scheme, we examine (i) the share of likely-unauthorized immigrants who report taking a private vehicle to work, (ii) the share who report carpooling to work conditional on taking a private vehicle, (iii) the share who report taking a single occupied vehicle to work, and (iv) the average one-way commute time.6A private vehicle includes an automobile, truck, or van. Taxicabs are considered public transportation.

First, we employ a difference-in-differences specification which controls for state and year fixed effects, as well as business cycle characteristics, driving policies, and demographic composition which may be correlated with both the decision to implement a UILP and the travel behavior of likely-unauthorized immigrants. Following Amuedo-Dorantes, Arenas-Arroyo, and Sevilla (2018), we then augment our model with state-specific linear time trends, in order to account for potential time-varying heterogeneity which may be correlated with travel behaviors and the implementation of a UILP. We construct these linear time trends by interacting each state fixed effect with a variable TREND that takes on the value 1 in 2008, 2 in 2009, up through 10 in 2017. This specification is given by equation (2):

(2)

Because only employed individuals are asked the transportation questions, we control for state-level business cycle characteristics. The vector  , includes the natural log of real state product per capita, the natural log of the real value of residential building permits, and the natural log of the number of initial unemployment claims. We also control for whether the state implemented a public or universal E-Verify mandate—policies shown to adversely affect the labor market prospects of likely-unauthorized immigrants (Amuedo-Dorantes and Bansak 2014; Orrenius and Zavodny 2015). Similarly, the vector

, includes the natural log of real state product per capita, the natural log of the real value of residential building permits, and the natural log of the number of initial unemployment claims. We also control for whether the state implemented a public or universal E-Verify mandate—policies shown to adversely affect the labor market prospects of likely-unauthorized immigrants (Amuedo-Dorantes and Bansak 2014; Orrenius and Zavodny 2015). Similarly, the vector  includes the fractions of the likely-unauthorized population which are male, Hispanic, white, black, and married. We also control for the shares which have less than a high school degree or a high school degree, the average number of children, and the average age.

includes the fractions of the likely-unauthorized population which are male, Hispanic, white, black, and married. We also control for the shares which have less than a high school degree or a high school degree, the average number of children, and the average age.

The coefficient of interest,  , measures how residing in a state implementing a is related to travel behavior for likely-unauthorized individuals. In the presence of the control variables, fixed effects, and trends, the identifying assumption is that the outcomes of interest for treated states would have evolved identically to those for the control states had the not been implemented.

, measures how residing in a state implementing a is related to travel behavior for likely-unauthorized individuals. In the presence of the control variables, fixed effects, and trends, the identifying assumption is that the outcomes of interest for treated states would have evolved identically to those for the control states had the not been implemented.

Insurance Outcomes: NAIC Auto Insurance Database Reports

We use the National Association of Insurance Commissioners’ Auto Insurance Database Reports (NAIC 2010, 2013, 2017, 2018) to test whether UILPs are associated with changes in auto insurance outcomes. These data are sourced from various statistical agencies and are assembled by the NAIC Causality Actuarial and Statistical (C) Task Force in order to help regulators and policymakers assess state insurance markets. The reports contain information on premiums, losses, exposures, and claims for both the voluntary and residual insurance market. We estimate the relationship between these data and the implementation of a UILP using equation (3):

(3)

where INSURANCE is our variable of interest. This equation is similar to equation (2) with a few notable exceptions. For one, the vector includes the natural log of the likely-unauthorized population and the natural log of the state population. Additionally, equation (3) controls for state driving policies which may be related to insurance outcomes, given by the vector  . These include whether the state had a graduated driver’s license program (Dee 1999; Ulmer et al. 2000; Eisenberg 2003; Dee, Grabowski, and Morrisey 2005; Karaca-Mandic and Ridgeway 2010; Argys, Mroz, and Pitts 2019), primary enforcement of a seat- belt law (Carpenter and Stehr 2008), or a texting ban (Kolko 2009; McCartt, Kidd, and Teoh 2014).

. These include whether the state had a graduated driver’s license program (Dee 1999; Ulmer et al. 2000; Eisenberg 2003; Dee, Grabowski, and Morrisey 2005; Karaca-Mandic and Ridgeway 2010; Argys, Mroz, and Pitts 2019), primary enforcement of a seat- belt law (Carpenter and Stehr 2008), or a texting ban (Kolko 2009; McCartt, Kidd, and Teoh 2014).

By allowing unauthorized immigrants to obtain driver’s licenses, UILPs increase the ease with which they can purchase auto insurance. As such, we first examine whether UILPs are associated with changes in auto insurance coverage as measured by the number of earned exposures. If unauthorized immigrants opt to purchase coverage, will be positive. In the event that unauthorized immigrants do not respond by purchasing auto insurance, the point estimate should remain small and insignificant. As such, we anticipate a non-negative coefficient, regardless of whether unauthorized immigrants purchase auto insurance.

Next, we test whether UILPs are related to auto insurance claims. If UILPs induce unauthorized immigrants who were previously not driving to get behind the wheel, we would expect the number of claims to increase by virtue of there being more drivers on the road. Moreover, if these new drivers purchase auto insurance, claims may rise if they use this coverage. However, it is also possible that UILPs do not increase the number of drivers on the road, and instead grant legality to those unauthorized immigrants who were already driving. However, we would still expect to see an increase in insurance claims in this scenario. For one, these newly-licensed drivers may purchase auto insurance, enabling them to file claims when they are involved in accidents. Additionally, possessing a license and insurance coverage will lower the cost of interacting with law enforcement officials or being involved in an accident. As such, newly-licensed and insured unauthorized immigrants may drive less carefully after the implementation of a UILP. In order to adjust for increases in auto insurance claims attributable to changes in insurance coverage, we also examine how UILPs affect the frequency of insurance claims. This latter measure is defined as 100*(incurred claims/earned exposures).

We also examine the severity of these claims, defined as the real value of incurred losses per claim.7The following example, adapted from NAIC (2018), is useful for clarifying the various measures considered: (4) (5)

An auto policy insuring one car for six months is issued on 9/28/2008, effective 10/1/2008. The cost of the policy is $300. The written exposure for this policy is 1 car × ½ year = 0.5 car-years and is included in calendar year 2008 exposures because the policy was issued in 2008. The written premium is $300 (cost of the policy) and is included in calendar year 2008 premiums. The policy is in force for three months in 2008. For calendar year 2008, the earned exposure is 1 cars × 1/4 year = 1/4 car-year, and the earned premium is: $300 × 1/2 policy length = $150.

The number of incurred claims in a given year is defined in the same report as the “total number of claims associated with insured events/ situations occurring during a given time period.”7 These data are available for the years 2008–2015. If UILPs induce more unauthorized immigrants onto the road, the relationship between UILPs and the severity of accidents will depend on both their relative propensity to be involved in a car accident and the value of their vehicles. If unauthorized immigrants are on average safer drivers than existing drivers, the severity of the average accident may fall. Moreover, this decrease will be exacerbated if these new drivers have less expensive cars. However, if unauthorized immigrants are riskier drivers and/or have more expensive vehicles, the severity of the average accident may increase. In the event that UILPs do not increase the number of drivers on the road, accident severity may increase if newly-insured unauthorized immigrants are riskier drivers. However, average accident severity may fall if these newly-insured drivers are filing claims for less expensive vehicles. As such, the relationship between UILPs and accident claims, frequency, and severity is an empirical question.

Within these broad outcome groups, we separately consider four types of insurance: (i) liability insurance—both bodily injury and property damage, (ii) collision insurance, (iii) comprehensive insurance, and (iv) uninsured/underinsured motorist insurance. It is worth noting that almost every state requires drivers to purchase liability insurance which covers damage done to other individuals. In contrast, collision insurance covers damages to the policyholder’s property, such as the cost of repairs or replacement. Comprehensive insurance covers theft or damage unrelated to a collision (such as a tree falling on the car). Finally, uninsured motorist insurance covers the costs associated with being hit by an uninsured driver.

As a falsification check, we also examine the relationship between UILPs and homeowners’ insurance using the NAIC’s Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Reports (2010–2019) for the years 2008 to 2017. Specifically, we consider the written number of homeowners’ owner-occupied insurance policies, as well as the number of these policies at different values (<$100,000; $100,000-$200,000; and >$200,000).

Traffic Outcomes: California SWITRS and National FARS

In order to more directly examine the relationship between UILPs and traffic outcomes, we utilize the 2008–2017 California’s Statewide Integrated Traffic Records System (SWITRS). These data are well-suit- ed for this analysis because they contain records of every collision occurring in California—not only those resulting in a fatality. Moreover, California’s UILP is the largest in the country; since AB 60 was imple- mented in 2015, over 1,000,000 unauthorized immigrants have obtained California driver’s licenses. As a result, over half of all unauthorized immigrants residing in UILP states live in California.

We follow Lueders, Hainmueller, and Lawrence’s (2017) methodology and use county-level data on the number of licenses issued between 2011 and 2014 to predict the number of licenses issued in 2015 using the following equation:

where our dependent variable,  , is the number of licenses issued by county,

, is the number of licenses issued by county,  , in year,

, in year,  . Our independent variables are time-invariant county fixed effects,

. Our independent variables are time-invariant county fixed effects,  , county-invariant year fixed effects,

, county-invariant year fixed effects,  , and county-specific linear time trends,

, and county-specific linear time trends,  . We then extend their methodology by using the predicted number of licenses for 2015 in place of the actual data and repeating this process to obtain the predicted number of licenses in 2016. With these data, we again repeat the process to obtain the predicted number of licenses in 2017.

. We then extend their methodology by using the predicted number of licenses for 2015 in place of the actual data and repeating this process to obtain the predicted number of licenses in 2016. With these data, we again repeat the process to obtain the predicted number of licenses in 2017.

California does not release county-level data on the number of AB 60 licenses issued. As such, we follow Lueders, Hainmueller, and Lawrence (2017) and attribute to the AB 60 program the difference between the number of licenses actually issued and the predicted number of licenses issued. Using these predictions, we estimate the following specification:

where our variable of interest,  , is the predicted number of AB 60 licenses as a fraction of the total number of licenses issued in the county. Our dependent variables of interest are the number of accidents per 1,000 people in the county, the number of fatalities per 1,000, and the number of fatalities per accident.88 These are the dependent variables considered by Lueders, Hainmueller, and Lawrence (2017). While these authors did not include county-specific linear time trends when estimating the relationship between AB 60 intensity and their outcomes of interest, we include them here in order to remain consistent with our prior estimation schemes. However, our appendices show that our estimates are robust to excluding these trends.

, is the predicted number of AB 60 licenses as a fraction of the total number of licenses issued in the county. Our dependent variables of interest are the number of accidents per 1,000 people in the county, the number of fatalities per 1,000, and the number of fatalities per accident.88 These are the dependent variables considered by Lueders, Hainmueller, and Lawrence (2017). While these authors did not include county-specific linear time trends when estimating the relationship between AB 60 intensity and their outcomes of interest, we include them here in order to remain consistent with our prior estimation schemes. However, our appendices show that our estimates are robust to excluding these trends.

In order to closely match Lueders, Hainmueller, and Lawrence (2017), we construct a time-invariant variable,  , by summing the number of AB 60 licenses issued in each county and dividing this total by the number of licenses issued in 2017. We then use this value to estimate equation (6):

, by summing the number of AB 60 licenses issued in each county and dividing this total by the number of licenses issued in 2017. We then use this value to estimate equation (6):

(6)

where  is an indicator for whether the law has been implemented.

is an indicator for whether the law has been implemented.

Finally, we also use the national 2008–2018 Fatality Analysis Reporting System (FARS) to test whether UILPs are associated with the number of vehicle related fatalities in a state. The FARS data contain a near-universe of fatal crashes in the US, including information on the number of injuries in each accident, the date of the accident, and demographic information about each fatality. Using these data, we estimate equation (3) where our dependent variable is the natural log of the number of fatalities in a state during the year.

Results

Travel Behaviors

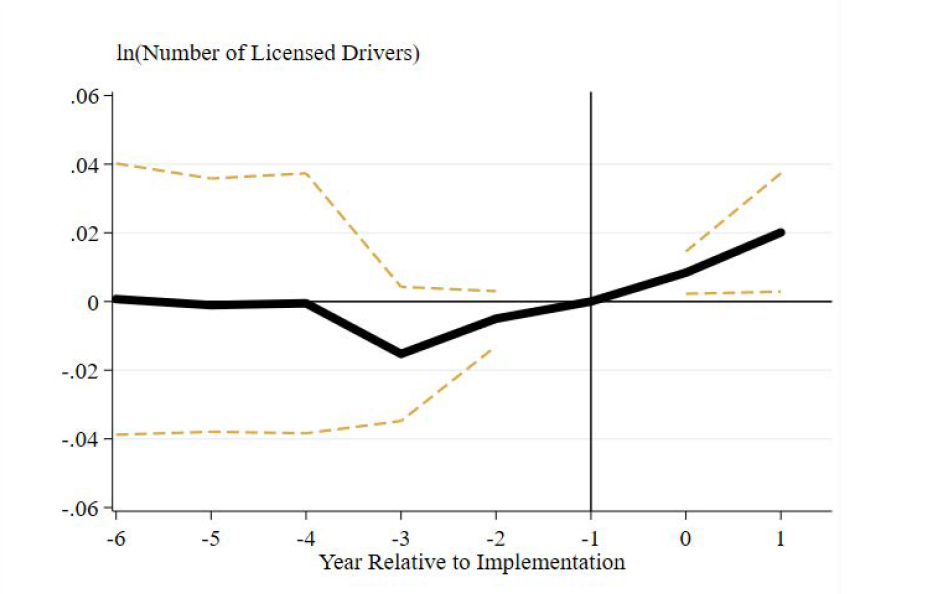

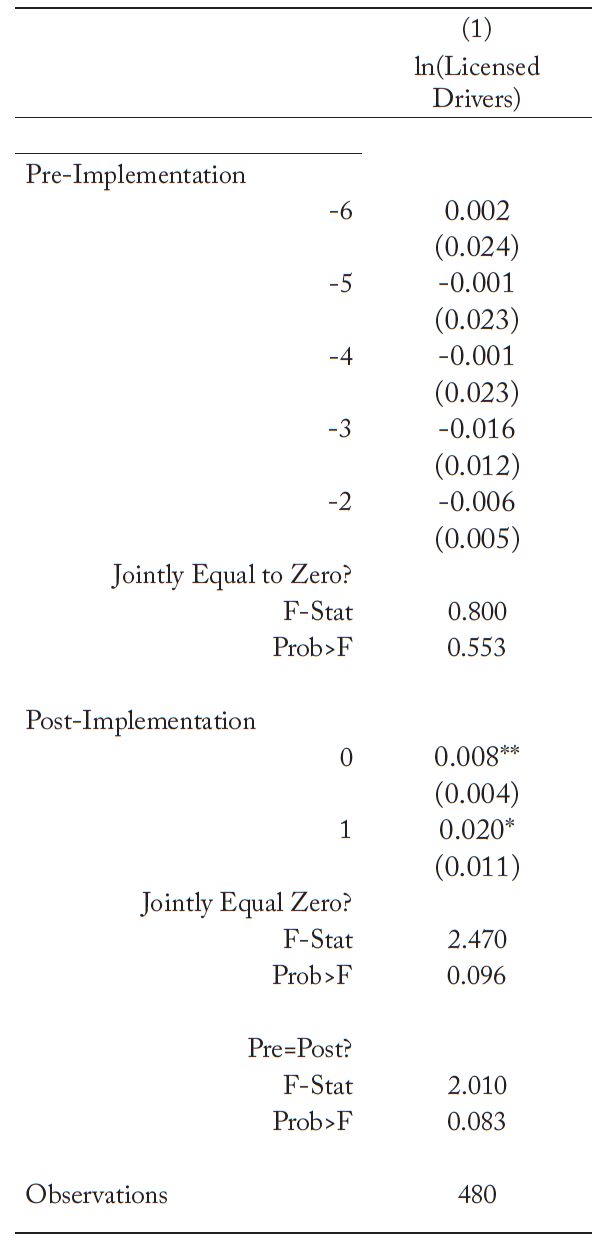

The flat pre-trend in Figure 2 indicates that changes in the number of licensed drivers in the years before UILP implementation were unrelated to the eventual implementation of a UILP.9 Exact coefficients and tests of joint significance are reported in Table A1. However, the number of licensed drivers increased by 1 percent at implementation and an additional 2 percent in the subsequent period. Indeed, we can reject the null hypothesis that the post-implementation coefficients are jointly equal to zero. As such, the event-study results alleviate concerns that states implementing UILPs were already experiencing increases in the number of licensed drivers, and support a causal interpretation of our estimates. The difference-in-differences estimate indicates a 1.3 percent increase in the number of licensed drivers for an average increase of nearly 55,000 licensed drivers.

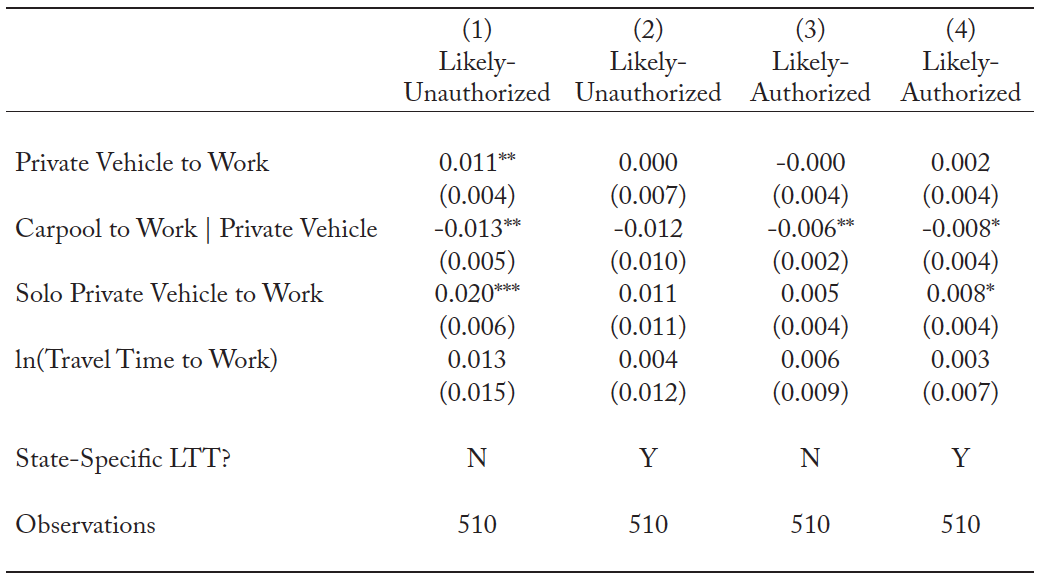

We next test whether UILPs are associated with changes in how likely-unauthorized immigrants report getting to work. In our baseline specification in Table 2, we see that UILPs are associated with a 1.1 percentage point increase in the share of likely-unauthorized immigrants who report taking a private vehicle to work (column 1 row 1), though this estimate is sensitive to the inclusion of state-specific linear time trends (column 2 row 1). We do not observe any corresponding change for likely-authorized immigrants (columns 3 and 4 row 1).

We also document a 1 percentage point reduction in the fraction of likely-unauthorized immigrants which reports carpooling conditional on taking a private vehicle (column 1 row 2), and this point estimate remains largely unchanged after the inclusion of linear time trends (column 2 row 2). Interestingly, UILPs are also negatively associated with the share of likely-authorized immigrants who report carpooling to work (columns 3 and 4 row 2). One explanation for this result is that these individuals were previously driving their unauthorized friends and family members to work. After the passage of a UILP, this service is no longer necessary.

Thus far, the evidence indicates that UILPs are associated with both an increase in the share of likely-un- authorized immigrants who report driving to work and a reduction in the share who report carpooling conditional on taking a private vehicle. In order to fully capture the change in the number of likely-unauthorized immigrants behind the wheel, our dependent variable in row (3) is the share which reports driving alone to work. We find that UILPs are associated with a 2 percentage point increase in the share of likely-unauthorized immigrants who report driving a single-occupied vehicle to work (columns 1 row 3), though this estimate falls to a 1 percentage point increase after the inclusion of state-specific linear time trends (column 2 row 3). Finally, we do not observe a change in commute time for either group (row 4).

Before proceeding, it is worth discussing how our estimates fit with the existing literature on UILPs. Using a difference-in-differences strategy which includes state-specific linear time trends, Amuedo-Dor- antes, Arenas-Arroyo, and Sevilla (2020) found that UILPs are associated with a statistically insignificant 0.8 percentage point increase in the probability that likely-unauthorized men report taking a private vehicle to work. They also found a statistically insignificant 0.1 percentage point reduction in the probability that these men report carpooling. Meanwhile, Cho (2019) used a difference-in-differences specification without linear time trends and found a 2.5 percentage point increase in the probability that a likely-un- authorized immigrant reports commuting by car. As such, our estimated effects are largely consistent with other work and provide support for the claim that UILPs increase the number of unauthorized immigrant drivers, though we show that this estimate is sensitive to the inclusion of state-specific linear time trends.

Insurance Outcomes

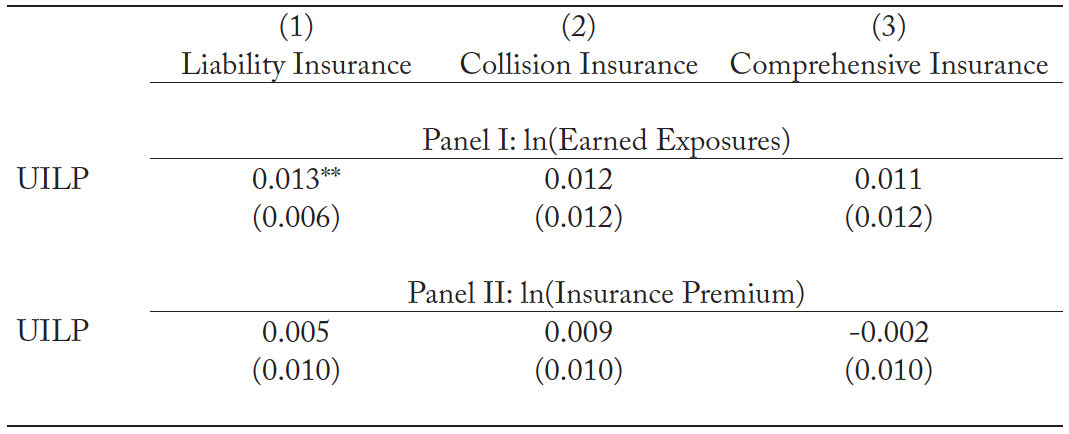

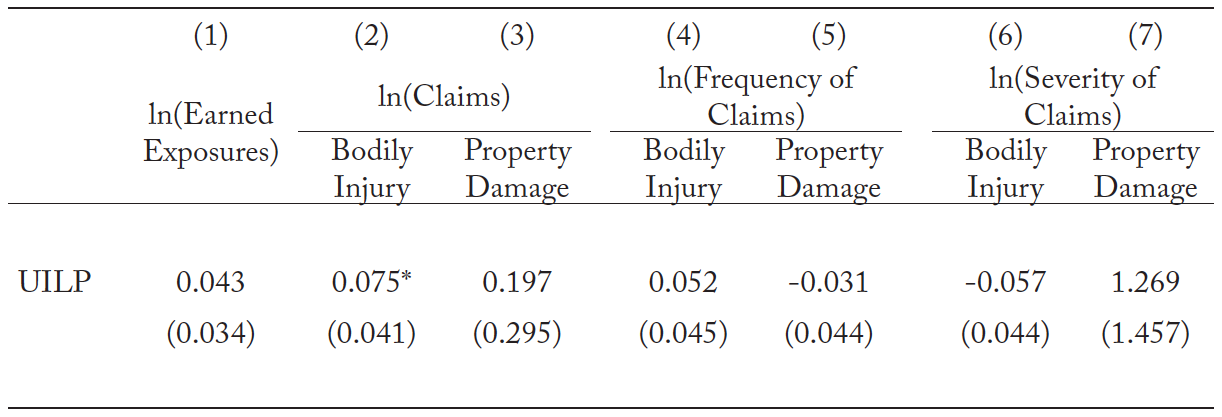

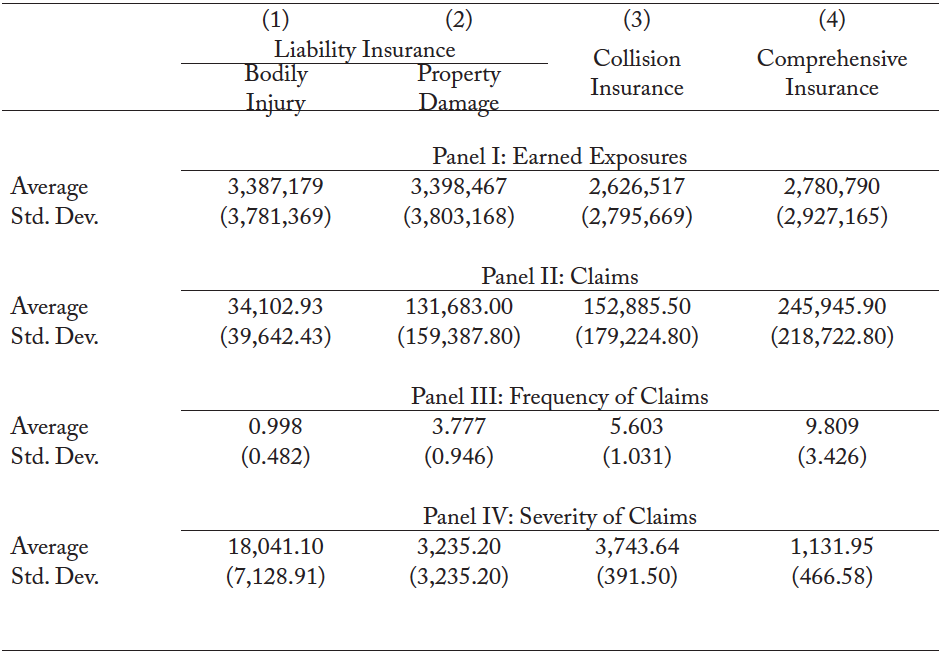

We next test whether UILPs are associated with greater auto insurance coverage as measured by the number of earned exposures. In Table 3, we show that UILPs are associated with a 1.3 percentage point increase in liability exposures (Panel I column 1).10The data separately reports the number of earned exposures for the bodily injury and property damage components of liability insurance, though the premium data are only reported for liability insurance as a broad category. The coefficients and standard errors are identical regardless of whether we examine the bodily injury or property damage components. Because the data are only available through 2015, we do not perform an event study analysis because we cannot estimate a meaningful post-period with a balanced panel. Using the summary statistics presented in Table A2, this is equivalent to over 44,000 liability insurance exposures. Similarly, we estimate a 1 percentage point increase in the number of collision and comprehensive insurance exposures (Panel I columns 2 and 3), though the results are statistically insignificant.11We show in Table A3 that the results are robust to using written exposures instead of earned exposures (see footnote 8 for a discussion of the difference). It is perhaps not surprising that we only detect an increase in liability insurance coverage, because almost every state mandates that licensed drivers purchase liability insurance but not necessarily other types of auto insurance. We do not detect any change in insurance premiums (Panel II).

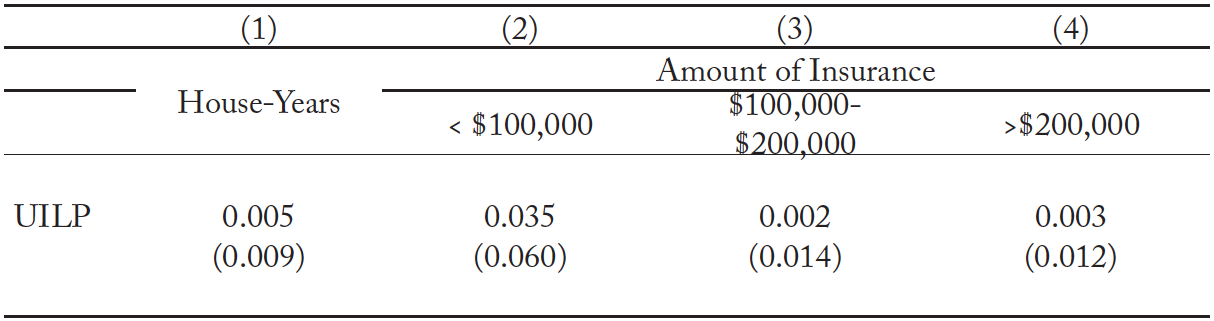

While the nature of our data prevents us from definitively attributing these increases to unauthorized immigrants, we show in Table 4 that they are not due to broader insurance trends. Specifically, we show that UILPs are unrelated to the number of homeowners’ insurance exposures (column 1). Nor do we identify any relationship between UILPs and the value of these policies (columns 2–4), suggesting that our estimates from Table 3 are identifying a relationship unique to auto insurance.

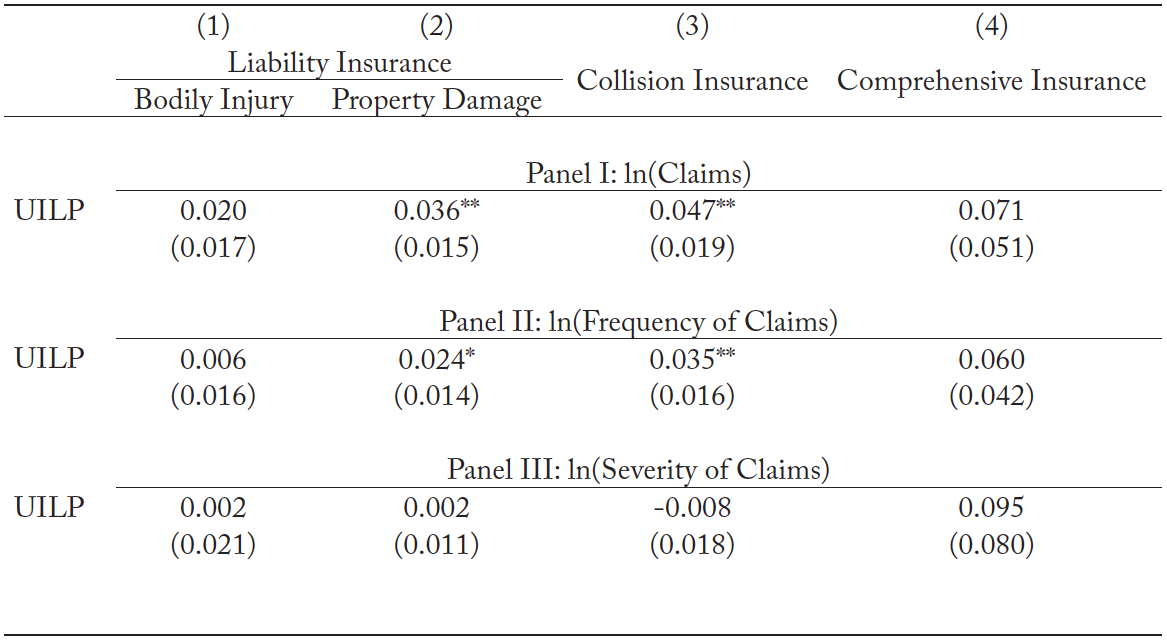

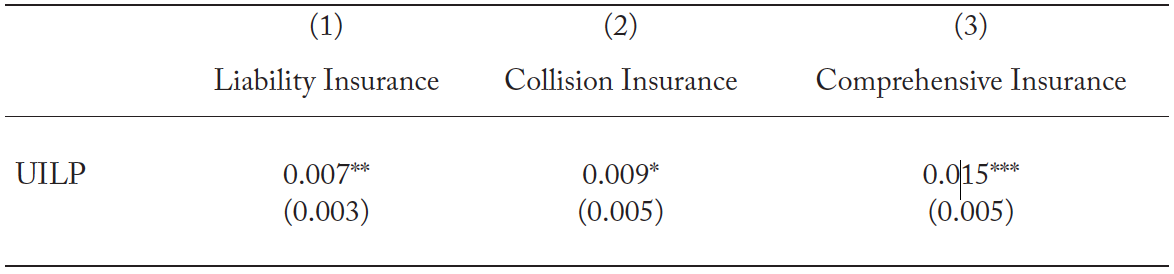

We next examine the relationship between UILPs and use of auto insurance. In Table 5, we show that UILPs are associated with a 3.6 percent increase in property damage claims (Panel I column 2), as well as a nearly 5 percent increase in collision claims (Panel I column 3). These increases persist even after accounting for changes in insurance coverage (Panel II column 2 and 3). We do not, however, find a relationship between UILPs and the severity of these claims (Panel III). As a whole, Table 5 suggests that UILPs are associated with more frequent—but no more expensive—insurance claims.

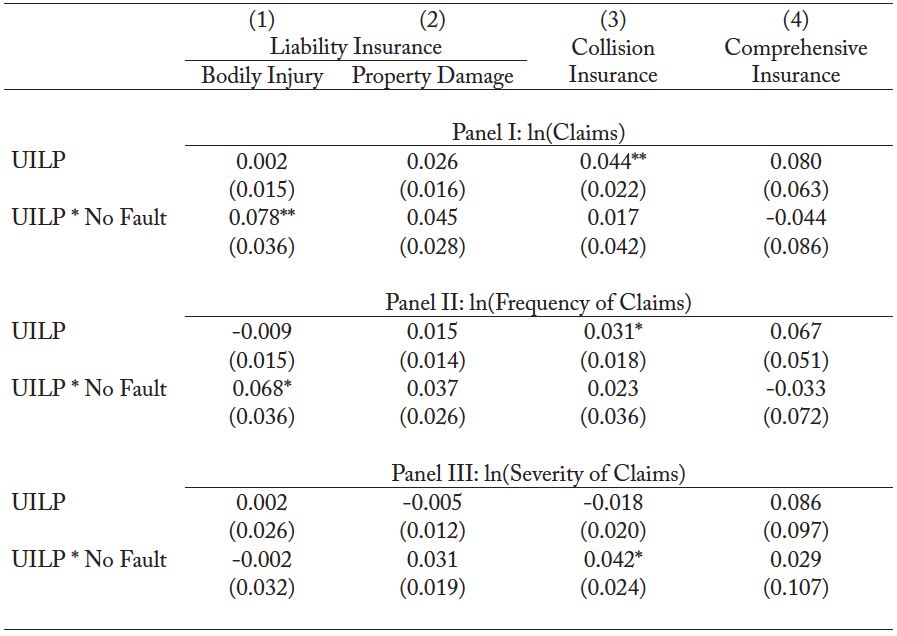

In Table 6, we test whether the relationship between UILPs and insurance claims differs by tort type. While UILPs are not related to bodily injury claims in traditional tort states, they are associated with an 8 percent increase in bodily injury claims in No Fault insurance states (Panel I column 1).12Five states (Delaware, Hawaii, Maryland, Utah, and Washington) as well as the District of Columbia have both No Fault insurance laws and a UILP. This is perhaps unsurprising; it is easier to file claims in No Fault insurance states. The point estimates also indicate that UILPs are associated with more property damage (Panel I column 2) and collision insurance claims (Panel I column 3) in No Fault insurance states, though the estimates are statistically insignificant.13 The p-value for property damage claims is 0.106 for the UILP coefficient and 0.118 for the interaction term. Because comprehensive insurance claims do not include another party, it is unsurprising that the interaction coefficient is negative and statistically insignificant (Panel I column 4). Again, these results persist after adjust- ing for changes in insurance coverage (Panel II).

In contrast to our estimates for the number of claims, we do not find any evidence that UILPs differentially affect the severity of bodily injury claims in No Fault insurance states (Panel III column 1). However, we identify a 2 percent increase in the severity of property damage (Panel III column 2) and collision insurance claims (Panel III column 3), though with a p-value of 0.105 the former estimate is statistically insignificant. In Table 7, we find little evidence of a relationship between UILPs and uninsured/under-insured motorist insurance claims. The only exception is an 8 percent increase in bodily injury claims (column 2), though this estimate does not persist after adjusting for changes in exposures (column 4). So, while the prior estimates suggest that UILPs are associated with more claims, the estimates in Table 7 suggest that these drivers are no less likely to be insured.

Traffic Accidents

While we have documented a positive relationship between UILPs and auto insurance claims, this result does not necessarily imply an increase in traffic accidents. It is instead possible that these claims arise from accidents that would have otherwise occurred but not been reported, because unauthorized immi- grants were unable to purchase auto insurance. That is to say, the results in the prior tables may be due to unauthorized immigrants more intensely utilizing auto insurance after holding the number of accidents constant.

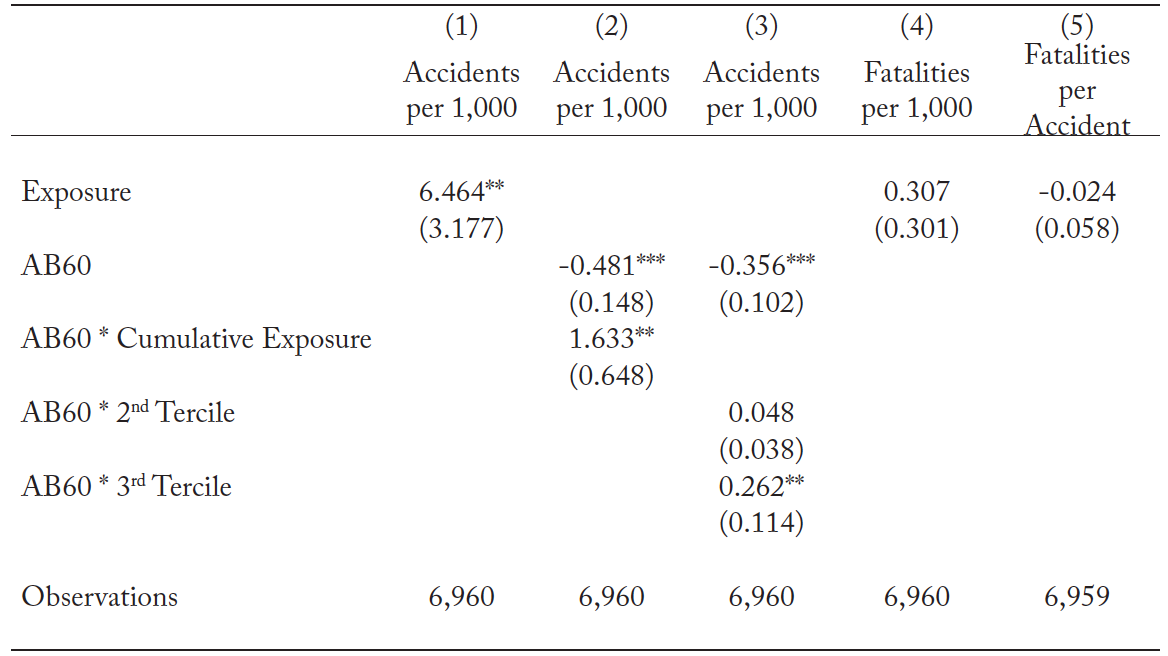

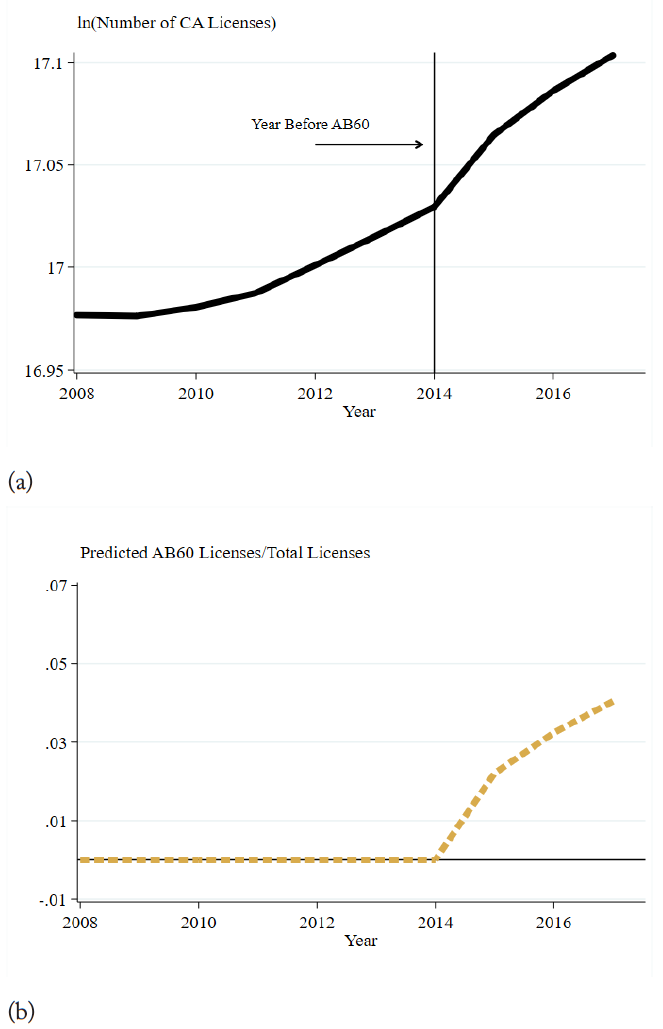

We test this possibility using California’s SWITRS data for 2008–2017 and extending the methodology proposed by Lueders, Hainmueller, and Lawrence (2017). As we show in Figure 3, California experienced an increase in the number of licenses issued after the implementation of AB 60 (Panel A), and our estimated county level share of AB 60 licenses (Panel B) aligns closely with administrative descriptive statistics. We predict that there were 606,226 AB 60 licenses issued in 2015, while the released number was 605,000 (CA DMV 2016). Similarly, we predict 983,853 AB 60 licenses in 2017, and the number of AB 60 licenses issued reached 1,000,000 by April of 2018 (CA DMV 2018).

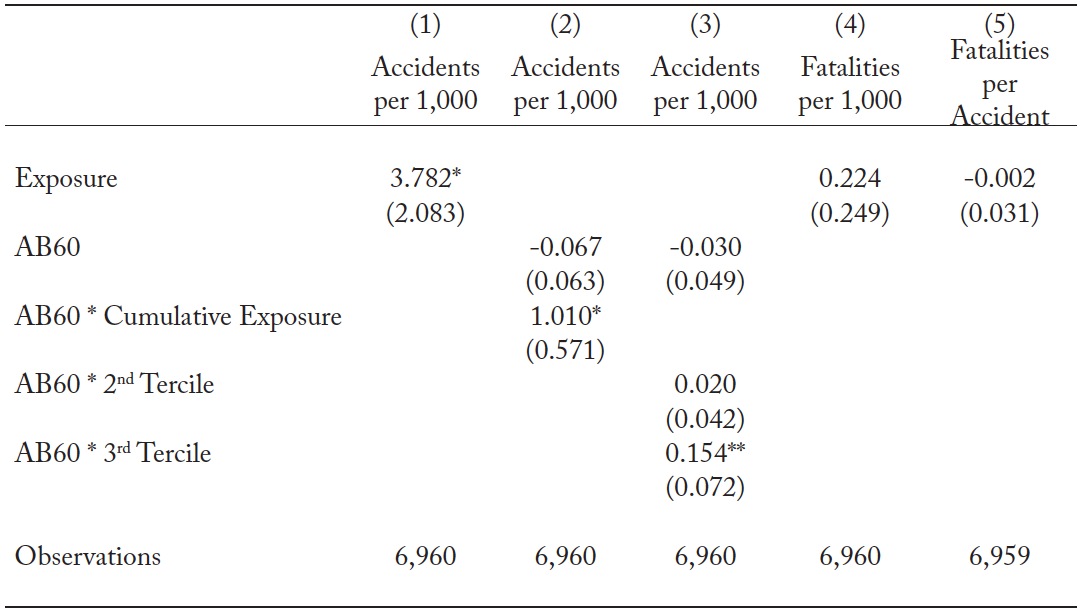

Using these estimates, we show in Table 8 that counties most intensely issuing AB 60 licenses saw increases in the number of collisions (column 1). Because the average value of exposure is 0.009 and the average number of accidents is 1.32 per 1,000, the coefficient is equivalent to a 4.4 percent increase in the average number of collisions per 1,000 people. This relationship is robust to interacting a time invariant measure of exposure  with an indicator taking on the value of 1 from 2015 onward (column 2). Moreover, the relationship is driven by the counties in the highest tercile of intensity in issuing AB 60 licenses (column 3). However, we do not find evidence that AB 60 exposure is differentially related to the number of fatalities in a county (column 4) or the number of fatalities per collision (column 5).14We picked the tercile cutoffs in order to match Lueders, Hainmueller, and Lawrence (2017), and the results are robust to alternative cutoffs. As a whole, Table 8 is consistent with our prior results indicating that while UILPs may be associated with more claims, they are not associated with more severe accidents.

with an indicator taking on the value of 1 from 2015 onward (column 2). Moreover, the relationship is driven by the counties in the highest tercile of intensity in issuing AB 60 licenses (column 3). However, we do not find evidence that AB 60 exposure is differentially related to the number of fatalities in a county (column 4) or the number of fatalities per collision (column 5).14We picked the tercile cutoffs in order to match Lueders, Hainmueller, and Lawrence (2017), and the results are robust to alternative cutoffs. As a whole, Table 8 is consistent with our prior results indicating that while UILPs may be associated with more claims, they are not associated with more severe accidents.

This pattern of results is new and stands in contrast to Lueders, Hainmueller, and Lawrence (2017) who did not find any change in the number of accidents. Our studies differ in two meaningful ways. For one, Lueders, Hainmueller, and Lawrence (2017) did not include county-specific linear time trends, and we show in Table A4 that our results are not driven by our inclusion of these trends. Instead, we show in Table A5 that our estimates are due to having additional years of data. Lueders, Hainmueller, and Lawrence’s (2017) sample period ended the year AB 60 was introduced, and we show in Table A5 that the relationship between AB 60 exposure and the number of accidents has increased over time.

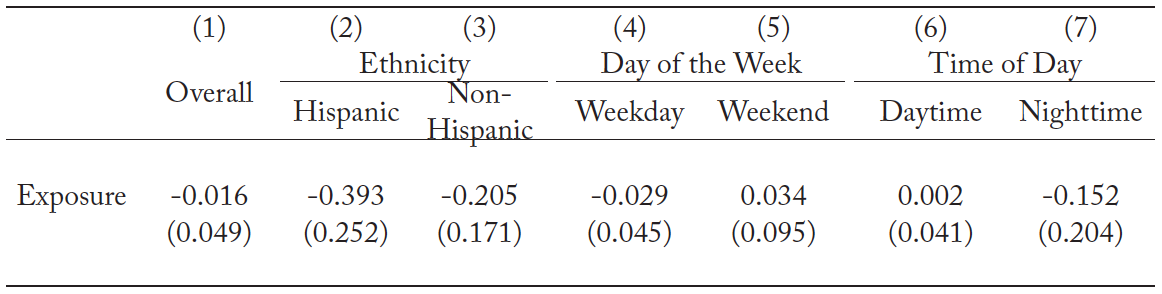

In Table 9, we use the FARS data and the difference-in-differences method of equation (3) to test whether there is a relationship between UILP implementation and fatal accidents throughout the country. Consistent with our evidence from California, we do not detect a change in the number of fatalities nationwide (column 1). Indeed, the coefficient is negative and statistically insignificant. Nor is there any change in fatalities by ethnicity (columns 2 and 3), the day of the week (columns 4 and 5), or the time of day (columns 6 and 7).

Conclusion

Proponents of UILPs argue that they enable unauthorized immigrants to purchase auto insurance. On the other hand, opponents worry that they induce more uninsured drivers onto the road and lead to more insurance claims. With 14 states and the District of Columbia allowing unauthorized immigrants to obtain driver’s licenses, and others debating similar initiatives, it is important to assess the veracity of these claims.

Our paper is the first to examine how UILPs affect the number of licensed drivers in a state as well as a comprehensive set of insurance outcomes. We show that UILPs increase the number of licensed drivers in a state and we find evidence that they are associated with a higher fraction of likely-unauthorized immigrants reporting that they drive themselves to work. We also document an increase in auto insurance coverage which is in line with our estimated increase in the number of licensed drivers. Therefore, it appears that unauthorized immigrants do respond by purchasing auto insurance. While we uncover some evidence that insurance claims rise, we do not uncover any relationship between UILPs and the severity of these claims. These estimates are consistent with accident data from California. While counties that issued the most driver’s licenses to unauthorized immigrants experienced increases in the number of collisions, these crashes were no more likely to result in a fatality.

Overall, our estimates suggest that many of the claims regarding UILPs are overstated, indicating that the decision to implement a UILP should largely be based on equity and legal considerations. It is worth noting, however, that we are unable to measure an important potential benefit of UILPs. For white natives, interactions with law enforcement through routine traffic stops often occur without incident. However, even a minor traffic stop can lead to deportation for an unlicensed unauthorized immigrant (NYT 2006; Washington Post 2019). By enabling these individuals to more safely interact with law enforcement officers, UILPs likely provide considerable psychological benefits to unauthorized immigrants, and attempting to quantify these benefits remains an important area for future work.

Appendix

Table 1. Policy passage and implementation

Source: National Conference of State Legislatures (2019)

Note: New Jersey has not set a date for when it will begin issuing driver’s licenses to unauthorized immigrants.

Table 2. UILPs are positively related to the share of likely-unauthorized immigrants driving to work

Source: American Community Survey, 2008–2017.

Note: The dependent variable in row (1) is the share of the group taking a private vehicle to work, in row (2) the share of the group carpooling conditional on taking a private vehicle, in row (3) the share of the group driving a vehicle to work without any passengers, and in row (4) the natural log of the one-way commute time in minutes. Columns (1) and (2) examine likely-unauthorized immigrants as identified by the Borjas and Cassidy (2019) residual imputation method. Column (3) and (4) consider the remaining immigrants. Columns (1) and (3) include only state and year fixed effects, business cycle controls (the natural log of state product per capita, the natural log of initial unemployment claims, the natural log of the real value of residential building permits, and indicators for whether the state had implemented a public or universal E-Verify mandate), demographic controls (the fraction of the respective group that is male, Hispanic, white, black, or married, as well as the average age, the average number of children, the fraction with less than a high school degree, and the fraction with a high school degree), and driving controls (an indicator for having a graduated driver’s license program, an indicator for having a texting ban, and an indicator for having primary enforcement of a seatbelt law). Columns (2) and (4) include state-specific linear time trends. Robust standard errors, shown in parentheses, are clustered at the state level. State-year averages are prepared using the sample weights, and estimates are weighted by the sum of the state-year weights. *** p<0.01, ** p<0.05, * p<0.10

Table 3. UILPs are associated with increases in auto insurance coverage

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2010, 2013, 2017, 2018.

Note: The dependent variable in Panel I is the natural log of the number of earned insurance exposures, while the dependent variable in Panel II is the natural log of the real value of the average insurance premium. Column (1) considers liability insurance, column (2) collision insurance, and column (3) comprehensive insurance. The independent variable of interest is an indicator for whether the state had implemented an Unauthorized Immigrant License Policy for at least half the year. Each column includes the natural log of the state population, the natural log of the likely-unauthorized population, business cycle controls (real state product per capita, the natural log of initial unemployment claims, the natural log of the real value of residential building permits, and indicators for whether the state had implemented a universal or public E-Verify mandate), driving controls (indicators for having primary enforcement of seatbelts, a texting ban, and a graduated driver’s license program), state fixed effects, year fixed effects, and state-specific linear time trends. The sample period is 2008–2015. Standard errors, shown in parentheses, are clustered at the state level. *** p<0.01, ** p<0.05, * p<0.10

Table 4. There is no relationship between the implementation of a UILP and the number or composition of written homeowners’ insurance exposures

Source: National Association of Insurance Commissioners, Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/ Cooperative Unit Owner’s Insurance 2010–2019.

Note: The dependent variable in column (1) is the natural log of the number of written homeowners’ owner-occupied exposures. Columns (2)–(4) consider the number of exposures by the value of the insurance (<$100,000, between $100,000 and $200,000, and greater than $200,000). Each column includes the full set of controls from Table 3. Standard errors, shown in parentheses, are clustered at the state level. The data are for years 2008–2017. *** p<0.01, ** p<0.05, * p<0.10

Table 5. UILPs are associated with more property damage and collision claims

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2010, 2013, 2017, 2018.

Note: The dependent variable in Panel I is the natural log of the number of insurance claims, in Panel II the natural log of the frequency of claims (total number of claims divided by exposures), and in Panel III the natural log of the real value of the severity of these claims. Column (1) examines the bodily injury component of liability insurance, column (2) the property damage component of liability insurance, column (3) collision insurance, and column (4) comprehensive insurance. Each column includes the full set of controls from Table 3. The sample period is 2008–2015. Standard errors, shown in parentheses, are clustered at the state level. *** p<0.01, ** p<0.05, * p<0.10

Table 6. The relationship between UILPs and changes in the number of auto insurance claims is more pronounced in No Fault insurance states

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2010, 2013, 2017, 2018. Note: The dependent variable in Panel I is the natural log of the number of insurance claims, in Panel II the natural log of the frequency of claims (total number of claims divided by exposures), and in Panel III the natural log of the real value of the severity of these claims. Column (1) examines the bodily injury component of liability insurance, column (2) the property damage component of liability insurance, column (3) collision insurance, and column (4) comprehensive insurance. Each column includes the full set of controls from Table 3. The sample period is 2008–2015. Standard errors, shown in parentheses, are clustered at the state level. *** p<0.01, ** p<0.05, * p<0.10

Table 7. UILPs are positively associated with uninsured/underinsured motorist insurance claims

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2010, 2013, 2017, 2018.

Note: The dependent variable in column (1) is the natural log of the number of earned exposures, in columns (2) and (3) the natural log of the number of claims, in columns (4) and (5) the natural log of the frequency of claims (total number of claims divided by exposures), and in columns (6) and (7) the natural log of the real value of the severity of claims. Each column includes the full set of controls from Table 3. The sample period is 2008–2015. Standard errors, shown in parentheses, are clustered at the state level. *** p<0.01, ** p<0.05, * p<0.10

Table 8. California counties issuing AB 60 licenses most intensely saw increases in collisions

Source: California Statewide Integrated Traffic Records System 2008–2017 Note: The dependent variable in columns (1)–(3) is the number of traffic collisions per 1,000 people in the county in a given month. The dependent variable in column (4) is the number of fatalities per 1,000 people, and in column (5) the dependent variable is the number of fatalities per accident. Each column includes county fixed effects, year fixed effects, month fixed effects, and county-specific linear time trends. The independent variable in columns (1), (4), and (5) is the number of predicted AB 60 licenses divided by the number of total licenses in the county. In column (3) the independent variables of interest are an indicator for the AB 60 law being implemented and its interaction with a time-invariant measure of exposure to AB 60. This latter measure is constructed by summing the number of AB 60 licenses issued between 2015 and 2017 and dividing it by the number of licenses in the county in 2017. The independent variables in column (4) are again the AB 60 indicator, as well as indicators for being above the 2nd and 3rd tercile in the cumulative exposure distribution. The sample size is one smaller in column (5) because there is one county-month-year observation without any accidents. Robust standard errors, shown in parentheses, are clustered at the county level. *** p<0.01, ** p<0.05, * p<0.10

Table 9. UILPs are unrelated to the number of vehicle related fatalities

Source: Fatality Analysis Reporting System 2008–2017

Note: The dependent variable in column (1) is the natural log of the number of fatalities. The next two columns examine the natural log of the number of fatalities by ethnicity, the subsequent two by the day of the week, and the final two by the time of the day. Each column includes the full set of controls from Table 3. Robust standard errors, shown in parentheses, are clustered at the county level. *** p<0.01, ** p<0.05, * p<0.10

Figure 1. States allowing unauthorized immigrants to obtain driver’s licenses

Source: National Conference of State Legislatures (2019).

Note: Lighter colored states do not allow unauthorized immigrants to obtain a driver’s license, while the darker states do. Though not pictured, Hawaii also offers licenses to unauthorized immigrants.

Figure 2. UILPs are associated with increases in the number of licensed drivers

Source: Federal Highway Administration’s Highway Statistics (2017) Note: The sample period is 2008–2017. The dependent variable is the natural log of the number of driver’s licenses in a state, while the independent variables are state fixed effects, year fixed effects, and two indicators for all of the periods outside the balanced window (-6 to 1). In order to ensure a balanced panel, the sample does not include Washington, New Mexico, or Utah. The exact coefficients are reported in Table A1. The dashed lines indicate 90 percent confidence intervals.

Figure 3. AB 60 increased the number of licensed drivers in California

Source: Institute for Social Research (2018); California Open Data Portal (2019)

Source: Institute for Social Research (2018); California Open Data Portal (2019)

Note: Panel (a) shows the natural log of the number of licenses issued in California over time. Panel (b) presents the estimated share of licenses held by unauthorized immigrants using an extension of the estimation scheme of Lueders, Hainmueller, and Lawrence (2017).

Table A1. UILPs are associated with increases in the number of licensed drivers

Source: Federal Highway Administration’s Highway Statistics (2017)

Note: The sample period is 2008–2017. The dependent variable is the natural log of the number of driver’s licenses in a state, while the independent variables are state fixed effects, year fixed effects, and two indicators for all of the periods outside the balanced window (-6 to 1). In order to ensure a balanced panel, the sample does not include Washington, New Mexico, or Utah. The coefficients are depicted in Figure 2. *** p<0.01, ** p<0.05, * p<0.10

Table A2. Summary statistics for insurance outcomes

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2010, 2013, 2017, 2018.

Table A3. UILPs are associated with increases in auto insurance coverage as measured by written exposures

Source: National Association of Insurance Commissioners Auto Insurance Database Reports 2013, 2017, 2018.

Note: The dependent variable is the natural log of the number of written insurance exposures. Column (1) considers liability insurance, column (2) collision insurance, and column (3) comprehensive insurance. The independent variable of interest is an indicator for whether the state had implemented an Unauthorized Immigrant License policy for at least half the year. Each column includes for the natural log of the state population, the natural log of the likely-unauthorized population, business cycle controls (real state product per capita, the natural log of initial unemployment claims, the natural log of the real value of residential building permits, and indicators for whether the state had implemented a universal or public E-Verify mandate), driving controls (indicators for having primary enforcement of seatbelts, a texting ban, and a graduated driver’s license program), state fixed effects, year fixed effects, and state-specific linear time trends. The sample period is 2008–2016. Standard errors, shown in parentheses, are clustered at the state level. *** p<0.01, ** p<0.05, * p<0.1

Table A4. The relationship between AB 60 exposure and collisions is robust to excluding county-specific linear time trends

Source: California Statewide Integrated Traffic Records System 2008–2017

Note: The dependent variable in columns (1)–(3) is the number of traffic collisions per 1,000 people in the county in a given month. The dependent variable in column (4) is the number of fatalities per 1,000 people, and in column (5) the dependent variable is the number of fatalities per accident. Each column includes county fixed effects, year fixed effects, and month fixed effects. The independent variable in columns (1), (4), and (5) is the number of predicted AB 60 licenses divided by the number of total licenses in the county. In column (3) the independent variables of interest are an indicator for the AB 60 law being implemented and its interaction with a time-invariant measure of exposure to AB 60. This latter measure is constructed by totaling the number of AB 60 licenses issued between 2015 and 2017 and dividing it by the number of licenses in the county in 2017. The independent variables in column (4) are again the AB 60 indicator, as well as indicators for being above the 2nd and 3rd tercile in the cumulative exposure distribution. The sample size is one smaller in column (5) because there is one county-month-year observation without any accidents. Robust standard errors, shown in parentheses, are clustered at the county level. *** p<0.01, ** p<0.05, * p<0.10

Table A5. The relationship between AB 60 exposure and collisions has gotten stronger over time

Source: California Statewide Integrated Traffic Records System 2008–2017 Note: The dependent variable is the number of accidents per 1,000 people in a county during a particular month. Columns (1)–(3) present estimates from a bivariate regression of the dependent variable on the Exposure variable and a constant. Columns (4)–(6) include county fixed effects, year fixed effects, month fixed effects, and county-specific linear time trends. Column (1) only includes observations from 2015, column (2) 2016, and column (3) 2017. Column (4) considers data from 2008–2015, column (5) 2008–2016, and column (6) 2008–2017. Robust standard errors, shown in parentheses, are clustered at the county level. *** p<0.01, ** p<0.05, * p<0.10

References

Amuedo-Dorantes, C., & Bansak, C. (2014). Employment verification mandates and the labor market outcomes of likely unauthorized and native workers. Contemporary Economic Policy, 32(3), 671–680.

Amuedo-Dorantes, C., Arenas-Arroyo, E., & Sevilla, A. (2020). Labor market impacts of states issuing driving licenses to undocumented immigrants. Labour Economics 63.

Argys, L. M., Mroz, T. A., & Pitts, M. M. (2019). Driven from work: Graduated driver license programs and teen labor market outcomes. Federal Reserve Bank of Atlanta Working Paper Series 2019–16.

Arrow, K. J. (1963). Uncertainty and the welfare economics of medical care. American Economic Review, 5, 141–149.

Bertrand, M., Duflo, E., & Mullainathen, S. (2004). How much should we trust differences-in-differences estimates? Quarterly Journal of Economics, 119(1), 249–275.

Borjas, G. J. (2017). The labor supply of undocumented immigrants. Labour Economics, 46, 1–13. Borjas, G. J., & Cassidy, H. (2019). The wage penalty of undocumented immigration. Labour Economics, 61.

Cáceres, M., & Jameson, K. P. (2015). The effects on insurance costs of restricting undocumented immigrants’ access to driver licenses. Southern Economic Journal, 81(4), 907–927.

Carpenter, C. S., & Stehr, M. (2008). The effects of mandatory seatbelt laws on seatbelt use, motor vehicle fatalities, and crash-related injuries among youths. Journal of Health Economics, 27(3), 642–662.

Chiappori, P.-A., & Salanie, B. (2000). Testing for asymmetric information in insurance markets. Journal of Political Economy, 108, 56–78.

Chiappori, P.-A., & Salanie, B. (2014). Asymmetric information in insurance markets: Predictions and tests. Handbook of Insurance.

Cho, H. (2019). Driver’s license reforms and job accessibility among undocumented immigrants. Working Paper.

Cohen, A., & Dehejia, R. (2004). The effect of automobile insurance and accident liability laws on traffic fatalities. Journal of Law and Economics, 47, 357–393.

Cummins, J. D., Phillips, R. D., & Weiss, M. A. (2001). The incentive effects of no-fault automobile insurance. Journal of Law and Economics, 44(2), 427–464.

Cummins, J., & Tennyson, S. (1996). Moral hazard in insurance claiming: Evidence from automobile insurance. Journal of Risk and Uncertainty, 12(1), 29–50.

Dee, T. S. (1999). State alcohol policies, teen drinking and traffic fatalities. Journal of Public Economics, 72(2), 289–315.

Dee, T. S., Grabowski, D. C., & Morrisey, M. A. (2005). Graduated driver licensing and teen traffic fatalities. Journal of Health Economics, 24(3), 571–589.

Dioenne, G. J. (2011). Incentive mechanisms for safe driving: A comparative analysis with dynamic data. Review of Economics and Statistics, 93, 218–227.

Dionne, G., Michaud, P.-C., & Dahchour, M. (2013). Separating moral hazard from adverse selection and learning in automobile insurance: Longitudinal evidence from France. Journal of the European Economic Association, 11(4), 897–917.

Egelman, S., & Cranor, L. F. (2005). The Real ID Act: Fixing Identity Documents with Duct Tape. I/S: A Journal of Law and Policy, 2(1), 149–183.

Eisenberg, D. (2003). Evaluating the effectiveness of policies related to drunk driving. Journal of Policy Analysis and Management, 22(2), 249–274.

Institute for Social Research. (2018). Assessing the Impacts of AB 60: California’s Low Cost Auto Insurance Program and Uninsured Motorists.

Kanstroom, D. (2006). The better part of valor: The REAL ID Act, discretion, and the rule of immigration law. New York Law School Law Review, 51, 61–206.

Karaca-Mandic, P., & Ridgeway, G. (2010). Behavioral impact of graduated driver licensing on teenage driving risk and exposure. Journal of Health Economics, 29(1), 48–61.

Kolko, J. (2009). The effects of mobile phones and hands-free laws on traffic fatalities. B.E. Journal of Eco- nomic Analysis and Policy (Contributions), 9, 1–26.

Landes, E. M. (1982). Insurance, liability, and accidents: A theroetical and empirical invesitgation of the effect of no-fault accidents. Journal of Law and Economics, 25(1), 49–65.

Lin, S. (2009). States of resistance: The REAL ID Act and constitutional limits upon federal deputization of state agencies in the regulation of non-citizens. New York City Law Review, 12, 329–354.

Lopez, M. P. (2004). More than a license to drive: State restrictions on the use of driver’s licenses by non- citizens. Southern Illinois University Law Journal.

Lueders, H., Hainmueller, J., & Lawrence, D. (2017). Providing driver’s licenses to unauthorized immi- grants in California improves traffic safety. Proceedings of the National Academy of Sciences, 114(16), 4111–4116.

McCartt, A. T., Kidd, D. G., & Teoh, E. R. (2014). Driver cellphone and texting bans in the United States: Evidence and effectiveness. Annals of Advances in Automotive Medicine, 58, 99–114.

National Association of Insurance Commissioners. (2010). Auto Insurance Database Report 2007/2008. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2010). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2008. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2011). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2009. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2012). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2010. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2013). Auto Insurance Database Report 2010/2011. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2013). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2011. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2014). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2012. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2015). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2013. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2016). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2014. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2017). Auto Insurance Database Report 2013/2014. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2017). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2015. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2018). Auto Insurance Database Report 2015/2016. National Association of Insurance Commissioners.

National Association of Insurance Commissioners. (2018). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2016.

National Association of Insurance Commissioners. (2019). Dwelling Fire, Homeowners Owner-Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report: Data for 2017.

National Conference of State Legislatures. (2019). States Offering Driver’s Licenses to Immigrants. Retrieved from http://www.ncsl.org/research/immigration/states-offering-driver-s-licenses-to-immigrants.aspx

National Highway Traffic Safety Administration. (2019). Fatality Analysis Reporting System Data 2008–2017.

NBC. (2019, April). States consider driver’s licenses for undocumented immigrants amid ramped up immigration enforcement. Retrieved from NBC Chicago: https://www.nbcchicago.com/news/politics/States-Drivers-Licenses-Undocumented-Immigrants-Immigration-Enforcement-508824221.html

New York Times. (2006, April 14). Path to deportation can start with a traffic stop. Retrieved from New York Times: https://www.nytimes.com/2006/04/14/nyregion/path-to-deportation-can-start-with-a-traffic-stop.html?mtrref=www.google.com&assetType=REGIWALL

New York Times. (2016, March 09). In Democratic debate, Hillary Clinton and Bernie Sanders clash on immigration. Retrieved from New York Times: https://www.nytimes.com/2016/03/10/us/politics/democratic-debate.html

New York Times. (2019, June 17). Driver’s licenses for undocumented are approved in win for progressives. Re- trieved from New York Times: https://www.nytimes.com/2019/06/17/nyregion/undocumented-immigrants-drivers-licenses-ny.html

New York Times. (2019, December 16). Long lines as undocumented immigrants in N.Y. rush to get licenses. Retrieved from New York Times: https://www.nytimes.com/2019/12/16/nyregion/undocumented-immigrant-drivers-license-ny-nj.html

Orrenius, P. M., & Zavodny, M. (2015). The impact of E-Verify mandates on labor market outcomes. Southern Economic Journal, 81(4), 947–959.

Passel, J. S., & Cohn, D. (2018). U.S. Unauthorized Immigrant Total Dips to Lowest Level in a Decade. Pew Research Center.

Pauly, M. V. (1968). The economics of moral hazard: A comment. American Economic Review, 58(3), 531–537.

Protect Oregon Driver Licenses. (2014). Representative Kim Thatcher – endorser. Retrieved from Protect Oregon Driver Licenses: https://www.protectoregondl.org/endorsers/representative-kim-thatcher-endorser-0

RAND. (2010). The U.S. experience with No-Fault automobile insurance: A retrospective.

Raphael, S., & Rice, L. (2002). Car ownership, employment, and earnings. Journal of Urban Economics, 52, 109–130.

Ruggles, S., Flood, S., Goeken, R., Grover, J., Meyer, E., Pacas, . . . Sobek, M. (2019). IPUMS USA: Version 9.0 [dataset]. Minneapolis: IPUMS.

Schneider, H. S. (2010). Moral hazard in leasing contracts: Evidence from the New York City taxi indus- try. Journal of Law and Economics, 53, 783–805.

State of California Department of Motor Vehicles. (2015, April 3). Nearly 500,000 Apply for Licenses Under AB 60. Retrieved from California DMV: https://www.dmv.ca.gov/portal/dmv/detail/pubs/newsrel/newsrel15/2015_27

Statewide Integrated Traffic Records System. (2020). California Highway Patrol. Accessed at: http://is-witrs.chp.ca.gov/

U.S. Department of Transportation Federal Highway Administration. (2018). Summary of Travel Trends: 2017 National Household Travel Survey. Washington D.C.: Federal Highway Administration.

Ulmer, R. G., Preusser, D. F., Williams, A. F., Ferguson, S. A., & Farmer, C. M. (2000). Effects of Florida’s graduated licensing program on the crash rate of teenage drivers. Accident Analysis and Prevention, 32, 527–532.

UTO Insurance. (2019, August). Can illegal immigrants get car insurance? Retrieved from UTO Insurance: https://www.autoinsurance.org/can-illegal-immigrants-get-auto-insurance/

Washington Post. (2019, June). New York will give licenses to undocumented drivers. Some county clerks refuse to comply. Retrieved from https://www.washingtonpost.com/transportation/2019/06/19/new-york-will-give-licenses-undocumented-drivers-some-county-clerks-refuse-comply/?noredirect=on

Washington Post. (2019, June 26). Sanctuary or not? After immigrants were wrongly targeted in Md. suburb, officials strengthen protections. Retrieved from Washington Post: https://www.washingtonpost.com/local/md-politics/sanctuary-or-not-after-immigrants-wrongly-targeted-in-md-suburb-officials-strengthen-protections/2019/06/26/d5ac277c-7c09-11e9-a5b3-34f3edf1351e_story.html?nore-direct=on

Weisburd, S. (2015). Identifying moral hazard in car insurance contracts. Review of Economics and Statistics, 97(2), 301–313.

World Bank. (2013, February). Motor Vehicles per 1,000 People. Retrieved from World Bank: https://data-catalog.worldbank.org/motor-vehicles-1000-people